The practical answer

- Short answer

- Messy cap tables kill deals. This diagnostic checklist covers dead equity, missing warrants, and 409A gaps that delay M&A exits by 35%.

- Best fit

- Industry: B2B Technology. Function: Finance & Legal

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 26.7% Average M&A indemnification cap as % of Deal Value (2025), reflecting heightened scrutiny on ownership risks.

The 90% Error Rate: Why Spreadsheets Kill Deals

In the high-velocity environment of a Series B or C scale-up, the capitalization table often lives in a spreadsheet managed by a part-time controller or the founder themselves. While this suffices for day-to-day operations, it is a liability in a transaction. Recent data suggests that 9 out of 10 spreadsheet-based cap tables contain material errors when audited during due diligence. These aren't just rounding errors; they are structural flaws that can pause a deal or, worse, trigger a re-trade.

The cost of this negligence is quantifiable. Legal analysis indicates that "corporate cleanup"—the frantic pre-deal legal work required to fix missing stock certificates, unrecorded option grants, and broken vesting schedules—can double your transaction legal fees, easily escalating from a standard $50,000 to over $100,000. More critically, these errors destroy trust. If a buyer cannot trust your representation of who owns the company, they will question the integrity of your revenue, your IP, and your forecasts.

The "Indemnification" Risk

Buyers are protecting themselves against this uncertainty with aggressive terms. In late 2024 and through 2025, indemnification caps in M&A deals surged to an average of 26.7% of Total Enterprise Value (TEV), a record high driven by heightened scrutiny on compliance and ownership risks. If your cap table isn't airtight, you aren't just risking a delay; you are risking a quarter of your exit proceeds being locked up in escrow to cover potential lawsuits from forgotten warrant holders or former employees.

If a buyer cannot trust your representation of who owns the company, they will question the integrity of your revenue, your IP, and your forecasts.

The Cleanup Checklist: Exorcising "Dead Equity" and Ghost Warrants

A pristine cap table is not just about accurate math; it is about accurate legal documentation. The most common "silent killers" in due diligence are not the active investors, but the ghosts of the past. Use this diagnostic to identify the liabilities hiding in your equity stack.

1. The "Dead Equity" Audit

Review every line item belonging to a former employee or advisor. Do you have a signed termination letter acknowledging the cancellation of unvested options? If not, that former marketing lead from 2022 technically still holds a claim to your equity. Auditing employee agreements is critical here; a missing IP assignment agreement combined with a murky equity grant is a litigation minefield that buyers will refuse to inherit.

2. The Warrant Reconnaissance

Warrants issued to venture debt lenders, landlords, or early advisors often lack the rigorous documentation of a priced equity round. We frequently see warrants that were "assumed" to have expired but lack a formal expiration or exercise notice. In a $100M exit, a "forgotten" 1% warrant is a $1 million liability. Ensure every warrant has a corresponding countersigned agreement and a clear status: exercised, expired, or outstanding.

3. The 409A Valuation Gap

If you issued options while your 409A valuation was expired (older than 12 months) or materially inaccurate, you have created a tax liability for your employees and a withholding obligation for your company. Buyers will demand a "cheap stock" analysis to quantify this risk. If the gap is significant, the buyer may require a special indemnity or a purchase price reduction to cover potential IRS fines.

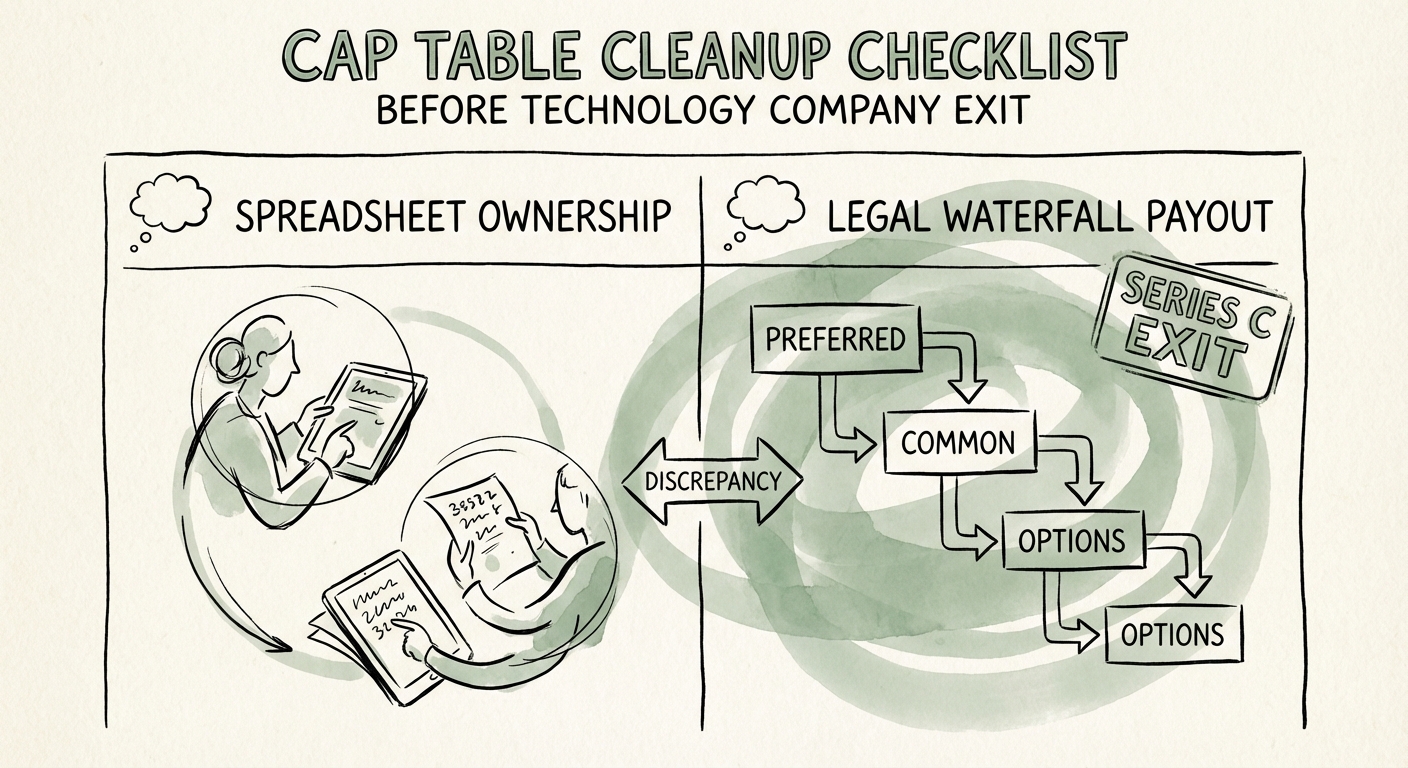

The Waterfall Reality Check: Spreadsheet vs. Legal Reality

The most painful moment in an exit is often the "Waterfall Analysis." This is the calculation that determines exactly how much cash each shareholder receives based on liquidation preferences, participation rights, and transaction fees. Founders often rely on a simple percentage ownership model (e.g., "I own 20%, so I get 20% of the deal"). This is rarely accurate.

Liquidation Preference Overhang

In a downside or flat exit, senior liquidation preferences (often 1x or greater) eat into the common stock payout. If you raised a Series C with a 2x liquidation preference or "participating preferred" status, your spreadsheet model might overstate your payout by millions. You must run a strict legal waterfall analysis that layers the Certificate of Incorporation terms over your cap table. Benchmarking your ownership against real-world dilution scenarios helps recalibrate expectations before the Letter of Intent (LOI) arrives.

The "Promised" Equity Trap

Did you ever promise an advisor 0.5% in an email? Did you tell an early engineer you'd "make them whole" in the next round? In the eyes of a PE buyer, these informal promises are undisclosed liabilities. You must formalize or legally extinguish these "handshake deals" before opening the data room. The Founder's Guide to Surviving Your First PE Partner emphasizes that transparency regarding these liabilities builds credibility; hiding them destroys it.