The practical answer

- Short answer

- Prevent a 15% valuation holdback with this employee agreement audit checklist. Cover IP assignments, non-competes, and change of control clauses before buyers look.

- Best fit

- Industry: Technology & Professional Services. Function: Human Resources & Legal

- Operating path

- Process Documentation → Operational Excellence → Transaction Execution Services

- Key metric

- 15% Typical valuation holdback required by buyers when IP assignment chains are incomplete or unverifiable.

The "Chain of Title" Trap: Why IP Assignments Kill Deals

In the hierarchy of deal killers, missing Intellectual Property (IP) Assignment agreements sit at the very top. Private Equity buyers do not purchase your code, your brand, or your customer list; they purchase the legal certainty that you own them. If a key developer from three years ago never signed a Proprietary Information and Inventions Assignment (PIIA) agreement, you do not own that module of your platform. You merely have an implied license to use it—a license that does not transfer to a buyer.

We consistently see founders treat HR documentation as a compliance checkbox rather than an asset protection strategy. This is a mistake that costs millions. In technology due diligence, buyers will conduct a "Chain of Title" audit. They will map every line of code to a human being, and then check for a signed PIIA for that human. If the chain is broken, the deal stops.

The Remediation Cost Is Extortionate

Fixing this post-LOI is the most expensive legal work you will ever pay for. To remediate a missing signature from a former employee, you often have to pay them a "signing bonus" to execute the document retroactively. We have seen former engineers demand $50,000 or more just to sign a standard IP assignment they should have signed on Day 1. If they refuse, the buyer will demand a 15-20% valuation holdback in escrow to cover the risk of future litigation.

Your Pre-Exit Audit Checklist:

- Audit Every Contributor: Map every current and former employee, contractor, and intern who touched your IP to a signed PIIA.

- Check the "Prior Inventions" Exhibit: A common trap is when a developer lists their side project in the "Excluded Inventions" exhibit, but that side project later becomes a core feature of your product. If it's excluded, you don't own it.

- Verify Consideration: For an agreement to be enforceable, there must be "consideration" (exchange of value). If you had existing employees sign new restrictive covenants without a raise or bonus attached, those agreements may be void in many jurisdictions.

Private Equity buyers do not purchase your code, your brand, or your customer list; they purchase the legal certainty that you own them.

The Non-Compete Reality in 2026: Pivot to Non-Solicits

The regulatory landscape for restrictive covenants has shifted over the last 24 months. As of 2026, the federal non-compete rule is not in effect after court vacatur and the FTC's decision to accede to that vacatur. The practical diligence question has moved to state law, role scope, and whether each covenant is narrowly drafted enough to survive review. Relying on a generic, 50-state non-compete template is now a liability, not a protection.

Buyers are no longer impressed by aggressive non-competes. They want enforceable confidentiality, invention assignment, customer non-solicitation, employee non-solicitation, and retention terms that counsel can defend. An over-broad non-compete can create diligence friction and may be unenforceable in important jurisdictions.

The "Blue Pencil" Risk

In many jurisdictions, including California, Minnesota, and Oklahoma, employee non-competes are broadly restricted or void against public policy. In others, courts may or may not reform overbroad provisions. Smart acquirers in 2026 prioritize non-solicitation and confidentiality agreements over broad non-competes. A tight, enforceable restriction on soliciting customers and colleagues is more useful than a broad ban on working in the industry.

Strategic Pivot: Review your agreements for over-breadth with counsel. If you ban a junior salesperson from working for "any competitor globally," you have created diligence risk. Narrow the scope to customer relationships, confidential information, and solicitation activity that the company can reasonably protect.

The "Change of Control" Landmines

As you prepare for exit, you must audit your executive agreements for "Change of Control" provisions that can distort your deal economics. Founders often grant early hires generous acceleration clauses—agreements that their unvested stock options will immediately vest upon an acquisition. While this sounds fair in the startup phase, it creates a massive retention problem for the buyer.

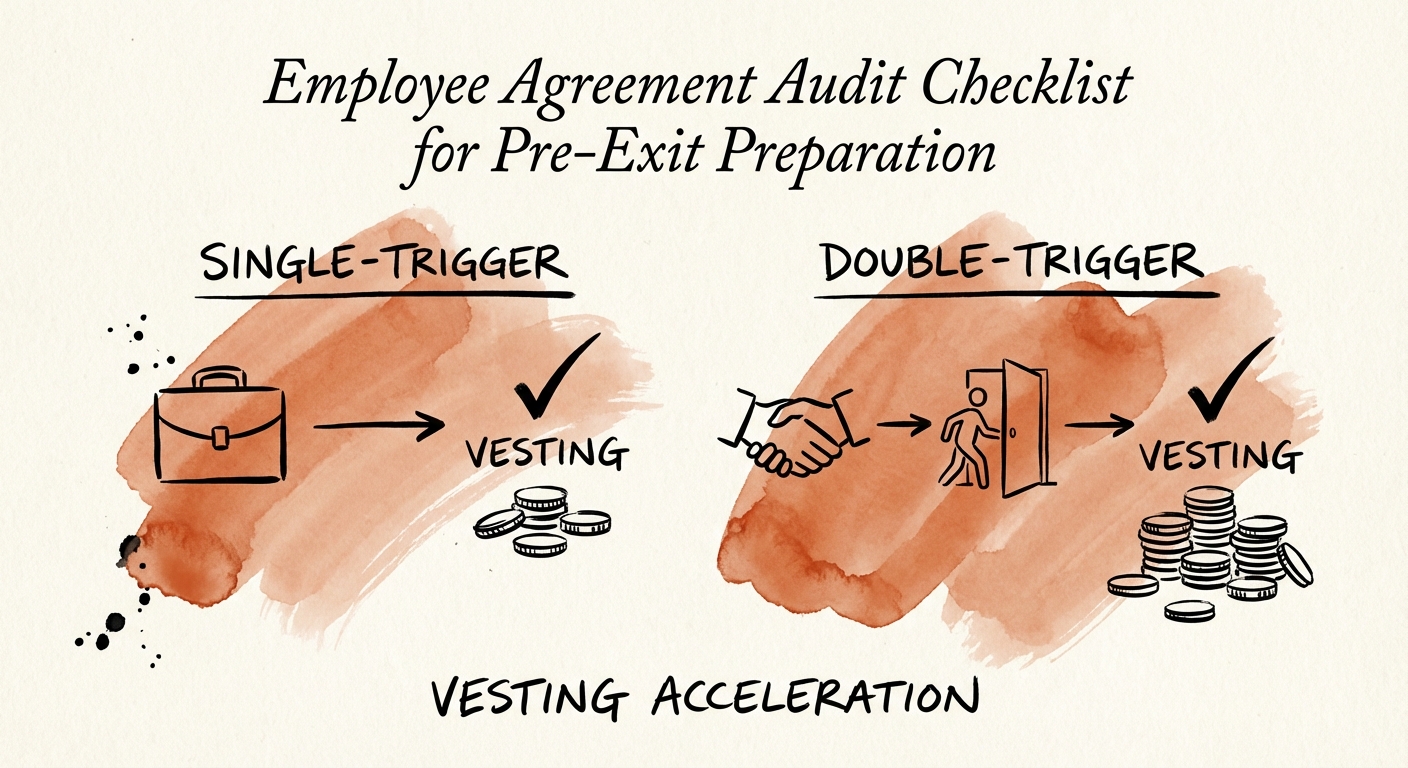

Single-Trigger vs. Double-Trigger

A "Single-Trigger" clause means the employee gets fully vested the moment the deal closes. They can take their check and walk out the door the next day. Buyers hate this. They will often lower the purchase price to create a new retention pool to re-incentivize these people.

You want "Double-Trigger" acceleration: vesting only accelerates if the company is sold AND the employee is terminated (or demoted) within 12 months. This protects the employee from being fired post-merger but ensures they stay if they are wanted. Converting single-trigger to double-trigger agreements is a critical founder extraction step that should happen 12-18 months before you hire an investment banker.