The Math That Keeps You Awake at Night

You started with 100%. It was a simpler time. You owned the code, the bank account, and the decisions. Then came the Seed round, and you traded a chunk of that freedom for runway. Now, you’re staring at a Series B term sheet, or maybe you just closed one, and you’re looking at your slice of the pie. It’s smaller. Much smaller.

For founders like you who have survived the \"valley of death\" only to enter the \"treadmill of scale\"—the psychological toll of dilution is real. You worry that you’re losing control. You worry that by the time you exit, you’ll be working for a salary in a company you built.

Let me stop you right there. This anxiety is usually based on a lack of context. You are comparing your ownership percentage to an imaginary ideal where you bootstrapped to $100M ARR, rather than the market reality of venture-backed scale.

We have analyzed the latest 2024-2025 datasets from Carta, SaaStr, and Blossom Street Ventures to give you the cold, hard benchmarks. No fluff. Just the numbers that tell you if you are on track for a life-changing exit or if you’ve been over-diluted.

The "Control" Fallacy

Many founders obsessed with maintaining 51% control destroy their companies. They reject capital that could fuel dominance because they fear the math. But as we tell every founder in our Founder to CEO transition labs: 15% of a $500M outcome is $75M. 80% of a $10M outcome is $8M.

You are not optimizing for percentage. You are optimizing for Enterprise Value (EV). But to do that, you need to know what "normal" looks like.

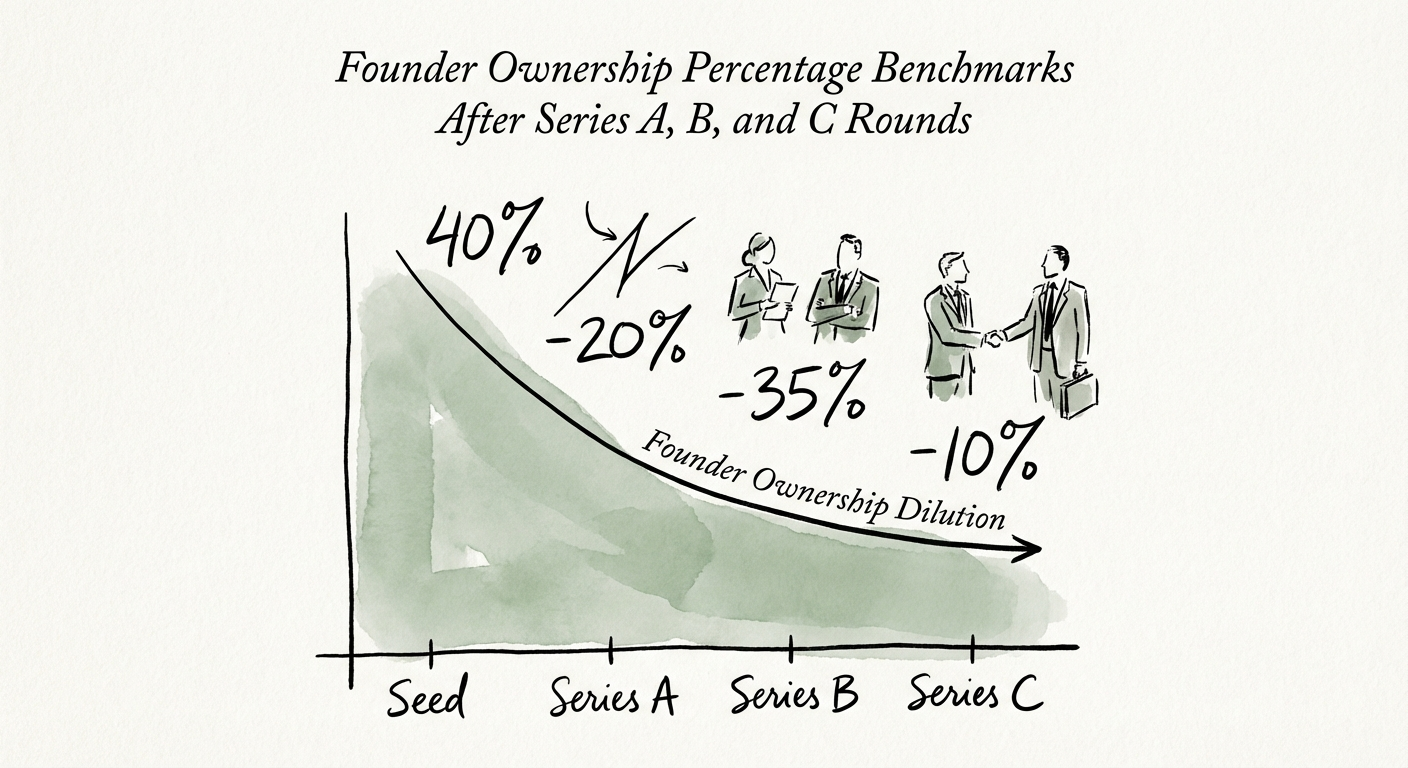

The 2025 Dilution Benchmarks

The market has shifted. In 2021, founders dictated terms. In 2024 and 2025, investors demanded more discipline, and valuations "normalized," meaning dilution is real and unavoidable. Here is the breakdown of median founder ownership (combined among co-founders) by stage.

1. Post-Seed: The "Honeymoon" Phase (56.2%)

According to Carta's 2025 Founder Ownership Report, the median founding team retains 56.2% of the company after the Seed round. This typically follows a dilution event of roughly 20-25%.

If you are below 50% post-seed, you likely raised on weak terms or had a massive pre-seed cap table. This is a warning sign for future rounds, as you have less \"currency\" to spend on talent and investors.

2. Post-Series A: The "Professionalization" Tax (36.1%)

This is the steepest drop. To get from $1M to $10M ARR, you need serious capital. The median founder ownership drops to 36.1%. At the 75th percentile (top performers), founders might retain closer to 48%, but that is increasingly rare in the current high-interest-rate environment.

At this stage, you also encounter the "Option Pool Shuffle." Investors will require you to refresh the employee option pool (typically 10-15%) before the investment, diluting you further. This is standard play, not a personal attack.

3. Post-Series B: The Scale Reality (23%)

By Series B, you are buying growth. You are hiring a VP of Sales, a CFO, and arguably building a middle management layer. The cost? Your ownership drops to a median of 23%. Data from SaaStr and Carta confirms that Series B rounds typically dilute existing shareholders by another 15-18%.

This is the psychological breaking point for many founders. You realize you no longer own a controlling interest. But remember: You trade control for velocity. If you aren't getting velocity (e.g., growing 80%+ YoY), then the dilution wasn't worth it.

4. Post-Series C & Exit: The Wealth Zone (15%)

By the time you reach Series C or an exit, Blossom Street Ventures analyzes that median founder ownership sits at just 15%. For massive successes like Aaron Levie at Box or Patrick Collison at Stripe, ownership can be higher, but for the median IPO or strategic exit, 15% is the magic number.

Is 15% bad? If you exit for $200M (a respectable mid-market exit), that’s $30M in your pocket. That is generational wealth. The danger is when you own 10% of a company that exits for $40M because you raised too much capital at too high a valuation and got crushed by liquidation preferences.

How to Defend Your Equity (Without Killing Growth)

You cannot stop dilution, but you can manage it. The founders who end up with 5% instead of 15% usually make specific, avoidable mistakes.

1. Stop "Buying" Valuation with Bad Terms

We see founders accept a higher valuation (to minimize dilution) in exchange for 2x or 3x liquidation preferences or participating preferred stock. Do not do this. A clean term sheet with 1x non-participating preferred stock at a slightly lower valuation is worth more to you at exit than a vanity valuation with "dirty" terms that put you at the bottom of the waterfall stack.

2. Hire for NRR, Not Just Logos

The most non-dilutive capital you can get is revenue from existing customers. If your Net Revenue Retention (NRR) is below 100%, you are burning equity to replace churned revenue. Fix your NRR, and you reduce your need to raise outside capital to plug the holes in your bucket.

3. The Option Pool Defense

When raising, negotiate the option pool size based on a hiring plan, not a rule of thumb. If an investor asks for a 20% pool, show them your hiring plan for the next 18 months. If the math says you only need 12%, you just saved yourself 8% dilution. Data wins arguments.

4. Prepare for the Secondary Sale

If you are a founder feeling "cash poor" despite a paper net worth of $20M, push for a secondary sale in your Series B or C. Taking $1M-$2M off the table reduces your personal anxiety and makes you a better, more aggressive CEO. It aligns your timeline with the fund's timeline. You stop playing "not to lose" and start playing to win.

Summary: It’s About the Multiple, Not the Percentage

Your 23% ownership at Series B is not a failure; it is the industry standard for high-growth venture assets. The goal now is to ensure that the remaining equity grows in value faster than it dilutes.

Focus on Exit Readiness—building a company that is bought, not sold. Document your processes, clean up your financials, and extract yourself from the day-to-day. That is how you turn your 15% at exit into a number that changes your family's future forever.