The practical answer

- Short answer

- Founders often treat disclosure schedules as administrative paperwork, but they are your primary defense against post-closing clawbacks. Here is the 2026 guide to negotiating exceptions in tech M&A.

- Best fit

- Industry: Technology. Function: Legal & Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

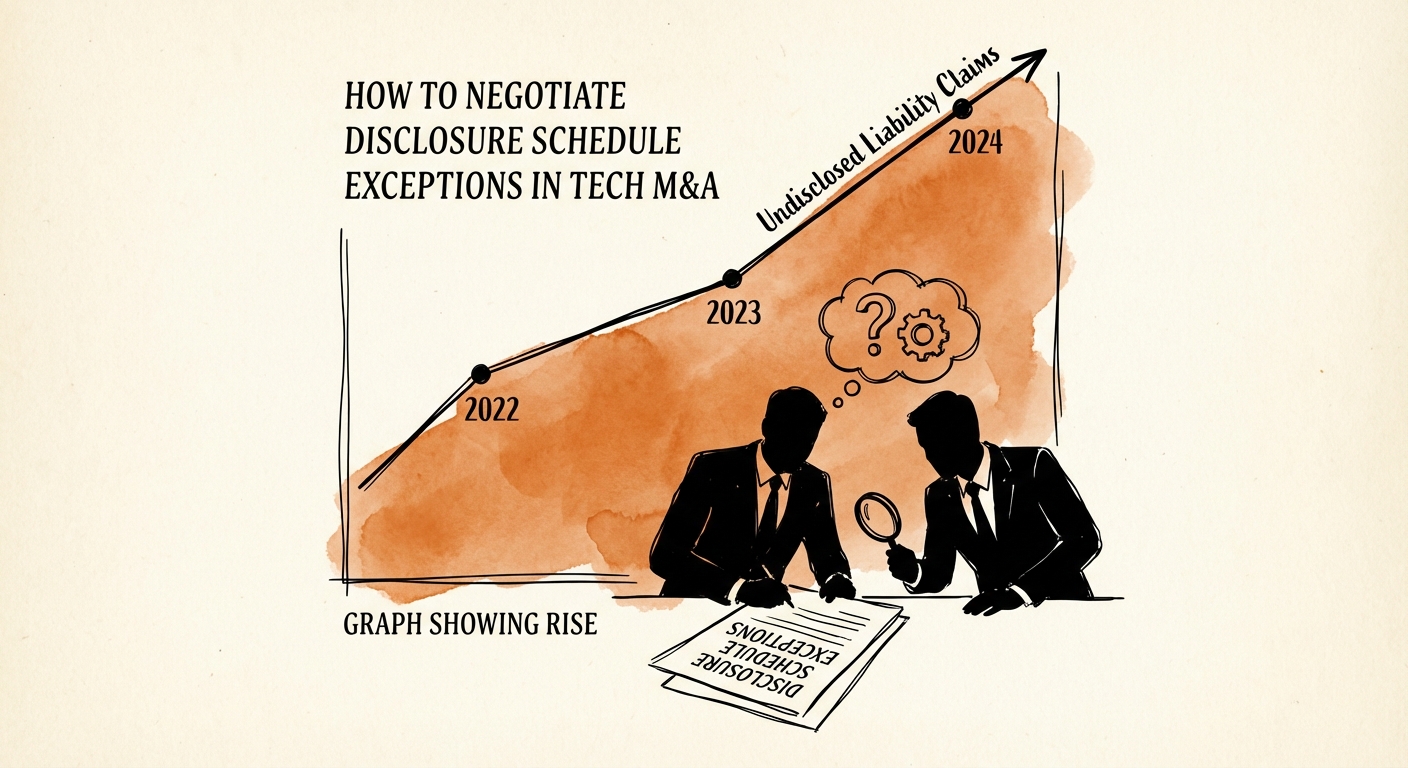

- Key metric

- 24% The percentage of M&A indemnification claims stemming from 'Undisclosed Liabilities' in 2024, doubling since 2022.

The Administrative Trap That Costs Founders Millions

In the final weeks of a deal, when adrenaline is high and sleep is scarce, the "Disclosure Schedule" often lands on a founder's desk as a 50-page Excel file labeled "Administrative." Your counsel asks you to populate it with every contract, employee, open source license, and potential lawsuit. The temptation is to delegate this to a junior finance manager or treat it as a check-the-box exercise. That is a multi-million-dollar mistake.

The Disclosure Schedule is not just a list; it is your primary shield against indemnification claims. In M&A law, the Representations and Warranties (R&W) describe the "perfect" version of your company. The Disclosure Schedule lists the exceptions to that perfection. If you disclose a fact properly, the buyer generally cannot sue you for breach of representation regarding that fact. Conversely, if you fail to disclose a material liability, you are handing the buyer an open checkbook to claw back proceeds from your escrow.

Recent data from SRS Acquiom reveals that 24% of all indemnification claims in 2024 were for "Undisclosed Liabilities," a figure that has doubled since 2022. In a market where buyers are increasingly litigious, the gap between what you know and what you write down is where deal value evaporates. For founders negotiating indemnity caps, the disclosure schedule is the functional mechanism that makes those caps irrelevant—because fraud and intentional misrepresentation (often argued from willful non-disclosure) typically uncap liability entirely.

If you don't list the skeleton in the closet, you are essentially paying the buyer to find it later. The Disclosure Schedule is the only place in the deal where you can unilaterally rewrite the risk allocation.

The RWI Paradox: Disclose Facts, Not Conclusions

The rise of Representations and Warranties Insurance (RWI) has fundamentally changed how disclosures function. In a traditional deal, you wanted to disclose everything to prevent the buyer from suing you. In an RWI deal, the dynamic is more complex.

RWI policies invariably exclude "known issues." If you disclose a specific liability on the schedule, the insurer will write a specific exclusion into the policy, meaning the insurance will not cover it. The buyer, now exposed, will turn back to you and demand a "Special Indemnity"—a dollar-for-dollar holdback from your exit proceeds to cover that specific risk.

This creates a paradox: You must disclose enough to avoid a fraud claim, but if you over-disclose or frame risks poorly, you guarantee a price reduction. The winning strategy is to disclose facts, not legal conclusions.

The Art of the 'Fact Pattern' Disclosure

Consider a scenario where your engineering team used a library with a questionable open source license.

- The Amateur Disclosure: "We are likely in violation of the AGPL v3 license in our core backend."

Result: The insurer excludes it. The buyer demands a $2M holdback for code remediation. - The Pro Disclosure: "The Company utilizes the 'XYZ' library, which is licensed under AGPL v3, in its backend architecture as described in the technical diligence folder 4.2."

Result: You have disclosed the fact. You have not admitted a violation. The insurer may still exclude it, but you have room to argue with the buyer that the risk is theoretical, not actual, potentially avoiding a special indemnity.

This nuance is critical when dealing with technical due diligence red flags. Your goal is to provide the buyer with enough information to be "on notice" without drafting their legal claims for them.

Three Tech Disclosures That Save Exits

Beyond the strategy, there are three specific line items in tech M&A that cause the most disproportionate damage when omitted.

1. The 'Pied Piper' Gap (IP Assignments)

It is common for early-stage startups to use contractors who never signed proper Proprietary Information and Inventions Assignment (PIIA) agreements. If you discover this during diligence, disclose it specifically: "PIIA agreements are missing for contractors A, B, and C." Do not hide it under a general "we use contractors" disclosure. If a buyer discovers this post-close and that contractor claims ownership of your IP, the "Failure to Disclose" claim will bypass your indemnity basket.

2. Change of Control Triggers in Revenue Contracts

Many founders assume their customer contracts are standard. However, enterprise procurement teams often slip in "termination for convenience" or "consent required for assignment" clauses triggered by an acquisition. Failing to disclose these on the "Material Contracts" schedule is a breach of the "No Conflict" representation. Referencing documented customer relationships is insufficient; you must explicitly list contracts that require consent.

3. Open Source 'Copyleft' Exposure

General disclosures like "The company uses open source software" are worthless in 2026. The ABA's deal points study indicates that "Sandbagging" (where a buyer sues for a breach they knew about) is legally permissible in many jurisdictions if the contract is silent. If you use Copyleft code (GPL, AGPL) linked to proprietary software, you must disclose the specific libraries. Buyers are increasingly using automated code scans (like Black Duck or Synopsys) post-close. If their scan finds what your schedule omitted, the remediation costs come directly out of your escrow.