The practical answer

- Short answer

- When PE diligence reaches your customers, sequence and stakes decide your multiple. A founder-CEO guide to staging reference calls without triggering churn or a holdback.

- Best fit

- Industry: B2B Technology & Services. Function: Sales & Customer Success

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 25% Standard valuation holdback applied by PE firms when key customer references fail to validate 'stickiness' or transferability.

The call happened too early, and the buyer heard exactly what they wanted

Here is the scene that wrecks deals. A founder of a 60-person B2B software-and-services company is three bidders deep into a competitive process, feeling good. Each bidder asks for "just a quick chat" with two or three customers. He wants to keep momentum, so he says yes to everyone. Within ten days, his single largest account — call it 30% of recurring revenue — has fielded four separate calls from people they've never met, asking pointed questions about renewal intentions and switching costs.

The customer doesn't churn. They do something worse for the deal: on the fourth call, slightly annoyed and trying to sound balanced, the VP says, "Honestly, we could probably build a lighter version of this internally if we had to." That single hedge — offered by a happy customer who was just tired of the questions — lands in the buyer's commercial diligence deck under "substitution risk." The offer gets re-cut.

This is the part founders miss. In a sell-side process, the reference call is not a character witness. The buyer has already concluded you're good at the work; that's why there's a Letter of Intent on the table. They are now on the phone for one reason — to price the probability that the revenue survives the transaction. Customers are up to three times more likely to churn when an acquisition leaves them feeling neglected or uncertain, and an uncoordinated parade of reference calls manufactures exactly that uncertainty — months before anyone signs. You're not validating your business. You're stress-testing it in public, for free, on behalf of the people negotiating against you.

A reference call isn't a compliment contest. The buyer already decided you're competent — they're on the phone to price the risk that your revenue walks out the door the day you do. Sequence the call wrong and you hand them the discount.

Why this is brutal for a company your size specifically

If you were a 4,000-customer SaaS business, a few sloppy reference calls would wash out in the average. You are not that company. In the lower-middle market, the top quartile of customers often drives roughly 89% of profit — which means your "reference list" and your "concentration risk" are the same five logos. Every name you offer up is, by definition, a name the buyer is already nervous about losing.

So the math runs against you twice. Each call you grant goes to an account whose departure would actually move the model, and the buyer knows it. When validation on those accounts comes back even slightly soft — a champion who's lukewarm, a renewal that "depends on the new owner's roadmap" — the buyer doesn't walk. They reach for the structure that lets them buy your company while transferring the risk back to you: the holdback. A meaningful slice of the purchase price, frequently around 25%, gets parked in escrow for 12 to 24 months and released only if those exact accounts stick. As PE diligence has gotten sharper and more data-driven, this kind of contingent structuring has become the default reflex, not the exception.

Read what that actually does to your outcome. A quarter of your headline number stops being a payment and becomes a bet — a bet on customers who got annoyed by the very process meant to reassure the buyer. The cruel irony: the founder who generously said "yes" to every reference request to seem confident is the one who hands the buyer the evidence to defer his own money.

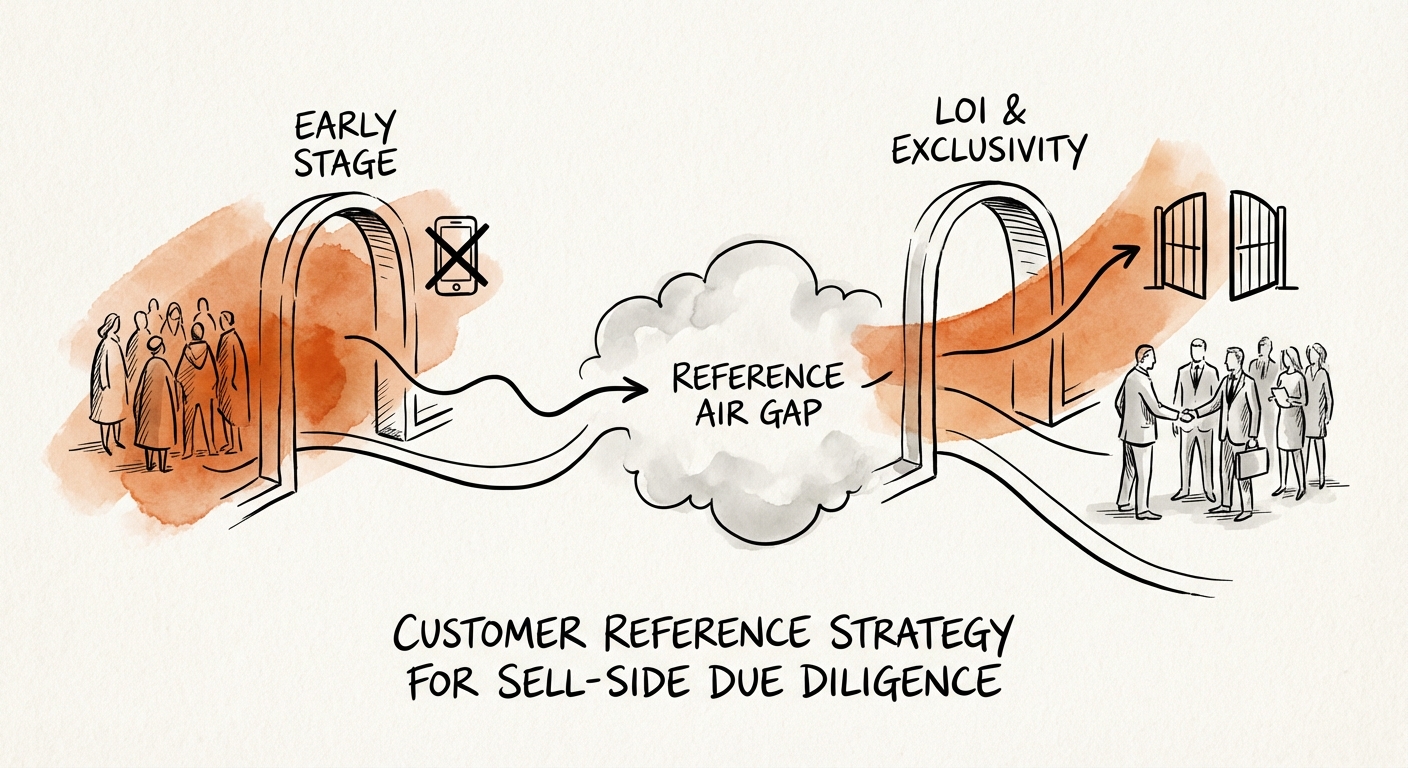

The fix: stage access by deal stage, then engineer the calls you do allow

The discipline is a gate. No live customer access until three things are simultaneously true — and "the buyer asked nicely" is not one of them.

Gate it on these, in order.

- A signed LOI with a real valuation range. If the price isn't agreed in principle, you're spending your customers' goodwill to help someone decide whether to bid.

- Exclusivity. You are no longer running a field of bidders. One party gets access, which caps total calls per account at a manageable number instead of multiplying them across every tire-kicker.

- Commercial diligence ~80% done. The buyer has already seen your retention data — NRR versus GRR, cohort curves, logo retention. The live call is confirmation of a thesis they've mostly built, not a discovery mission you're funding.

For everything before that gate, feed curiosity without exposing relationships. Put a "reference portfolio" in the data room early — recorded customer video, case studies with hard ROI numbers, anonymized verbatims. It blunts the buyer's urge to "just talk to a few people now," and it's your defense against the blind third-party calls a buyer commissions into your category. Because of your concentration profile, an analyst dialing "companies in your space" can de-anonymize you in two questions; documented proof in the room reduces how hard they dig.

When you do open the gate, don't hand over your three happiest friends. Pick three accounts that each prove a line item in the buyer's investment thesis: the expander who started small and grew their spend several times over (proves you land and expand), the switcher who left a named competitor for you (proves the moat is real, not just incumbency), and the survivor who stayed through a price increase or a rough outage (proves the workflow is genuinely sticky, not just cheap). Then make a real call to each champion before the buyer does — not to coach the answers, which destroys credibility, but to frame the why: "We're bringing in a partner to fund the roadmap you've been asking for; they want to hear what you actually need next." Want the questions a buyer will be working from on that call? Pressure-test yourself against the pre-LOI diligence checklist first. Sequence it this way and the reference round stops being the place your deal leaks value — it becomes the place you defend the multiple and keep the full check off the escrow table.