The practical answer

- Short answer

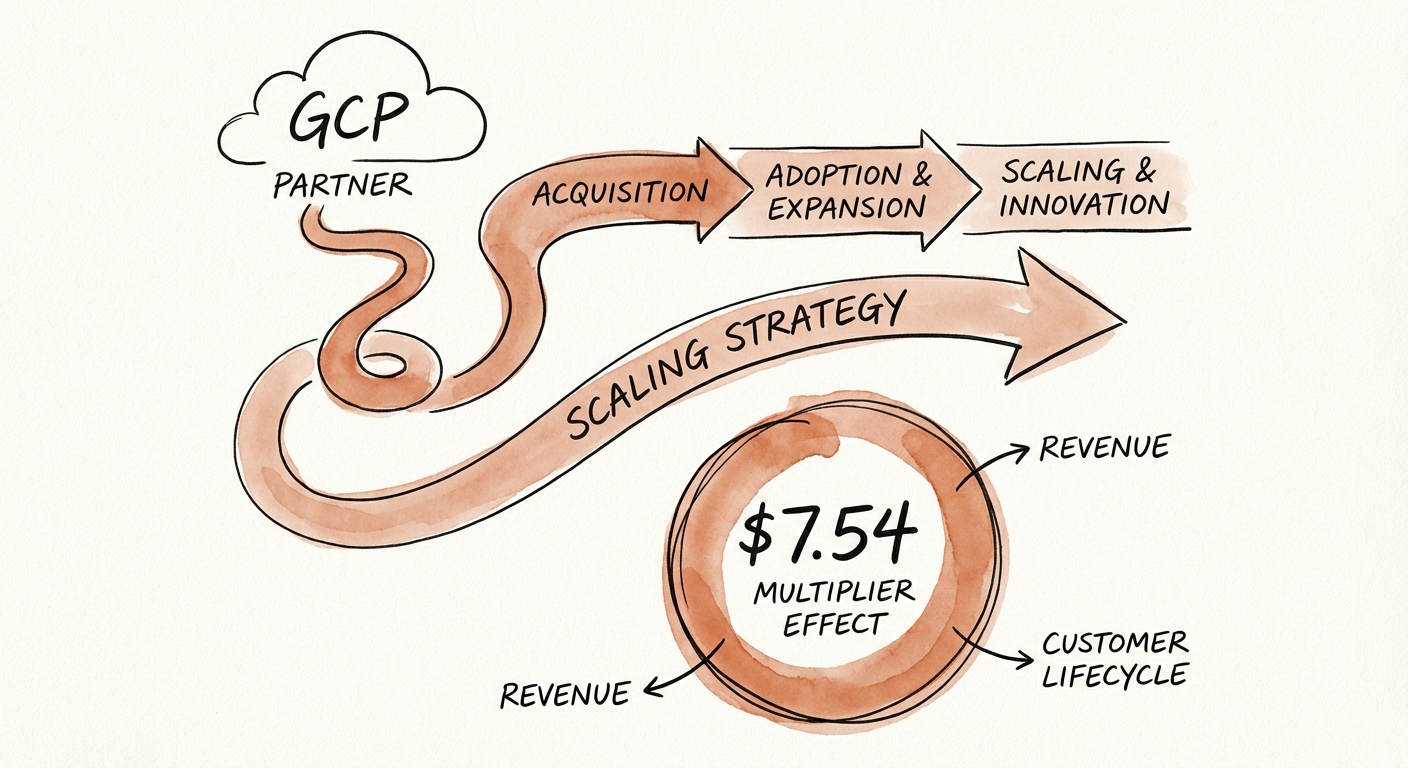

- 2026 growth benchmarks for GCP partners. How to scale from $10M to $50M, unlock the $7.54 multiplier, and escape the 'generalist' valuation trap.

- Best fit

- Industry: Cloud Consulting & Managed Services. Function: Growth Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 1% Of U.S. companies break the $10M revenue ceiling.

The $7.54 Multiplier: Why Resale is the Wrong Revenue Goal

If you are still celebrating resale margin, you are playing a 2020 game. The 2026 Google Cloud Partner ecosystem has shifted largely away from simple resale economics. While Google Cloud is growing at 32% YoY—outpacing AWS and Azure in recent quarters—the real story for partners isn't the cloud consumption itself; it's the services wrapped around it.

New data indicates that for every $1 of Google Cloud consumption sold in 2025, partners are projected to generate $7.54 in their own services, IP, and managed support revenue. This is your new North Star metric. If your firm is generating $2 in services for every $1 of consumption, you are leaving over $5 on the table. You are effectively a low-margin bank for Google, carrying the receivables risk while someone else captures the high-margin transformation budget.

For founders stuck at $15M revenue, this is usually the primary blocker. You built the business on low-friction resale and "lift and shift" migrations. That got you to $10M. It won't get you to $50M. The "Diamond" tier and updated 2026 Partner Network changes are explicitly designed to reward partners who deliver outcomes—meaning complex data estate modernization, GenAI implementation, and sticky managed services—rather than just transaction volume.

You can be a $10M generalist forever, or you can be a $50M specialist. You cannot be both. The market has bifurcated, and the middle ground is a kill zone.

The $10M Trap vs. The $50M Machine

Breaking the $10M ceiling is statistically improbable for most service firms; fewer than 1% of U.S. companies ever achieve it. The reason isn't lack of market demand—GCP demand is white-hot. The reason is the "Hero Founder" operational model.

At $5M to $10M, you (the founder) are the Chief Selling Officer and the Chief Firefighter. You close the big deals, and you save the red accounts. But to scale to $50M, you must transition from "heroics" to "systems." Here is the benchmark data separating the stalled $10M generalist from the scaling $50M specialist:

- Revenue per Employee: Stalled firms hover at $180k. Scaling firms push $250k+ by leveraging IP and automation.

- Gross Margin: Generalists accept 35-40% blended margins. Specialists command 55-60% by selling "outcomes" (e.g., Data Modernization) rather than "hours."

- Utilization: The trap is running at 85% utilization, leaving no room for growth or training. The $50M firm targets 68-72% utilization, intentionally creating slack for innovation and pre-sales engineering.

Without documenting your processes and extracting the founder from the sales cycle, you cannot scale. You will hit the $10M wall, bounce off, and burn out.

Valuation Reality: The Gap Between 4x and 12x

Not all GCP revenue is created equal. When Private Equity looks at your firm, they don't just see "Google Cloud Partner." They see a specific valuation multiple based on what you sell.

The Generalist Discount (4x - 6x EBITDA)

If you are a "Premier Partner" with a generic listing—doing a bit of Workspace, a bit of VM migration, and a bit of resale—you are a commodity. PE firms value these businesses at 4x to 6x EBITDA. The risk is high because you have no moat; a Global Systems Integrator (GSI) can undercut your rates tomorrow.

The Specialist Premium (10x - 14x EBITDA)

The firms trading at double-digit multiples in 2026 have picked a lane. They aren't just "GCP Partners"; they are "The Healthcare Data Security Experts on GCP" or "The GenAI Retail Implementation Leaders." They own Intellectual Property (IP)—accelerators, connectors, or proprietary frameworks—that makes their revenue sticky. They have Net Revenue Retention (NRR) above 115%. They don't just sell hours; they sell speed and certainty.

To get exit-ready, stop chasing every RFP. Specialize rigorously. Build the IP that justifies the $7.54 multiplier. That is how you turn a stalled service shop into a strategic asset.