The practical answer

- Short answer

- Stop selling seats. Start selling strategy. Discover why Jira Align practices command 12x multiples and how to pivot your Atlassian firm from 'admin' to 'advisor'.

- Best fit

- Industry: Private Equity / IT Services. Function: Strategy / GTM

- Operating path

- GTM Execution → Commercial Performance → Performance Improvement

- Key metric

- 147% Net Retention Rate for Atlassian customers spending >$1M (The 'Stickiness' Premium).

The 'License Flipper' Trap vs. The Strategy Premium

For the last decade, the Atlassian partner ecosystem was a volume game. You sold Jira Software seats, tacked on a 15% margin, and maybe sold a few days of configuration services. It was a good business, but it wasn't a valuable one. In 2026, 'Tooling Shops'—firms that primarily configure workflows and resell licenses—are trading at 4x to 6x EBITDA. They are viewed as commodities, vulnerable to direct sales teams and AI-driven self-configuration.

The market has bifurcated. On the other side of the chasm are 'Transformation Partners.' These firms aren't selling software; they are selling Enterprise Agile Planning (EAP). They use Jira Align not as a ticket tracker, but as a forcing function for organizational change (typically SAFe or Spotify Model implementations). Because they own the strategy—not just the settings—they command 10x to 14x EBITDA multiples.

The math explains the gap. A standard Jira Software implementation might drag along $1.50 in services for every $1.00 in license revenue. A properly executed Jira Align engagement, however, should generate a 3:1 to 5:1 services-to-license ratio. If you are selling Jira Align and your services attach rate is under 3x, you aren't doing transformation. You're just installing expensive shelfware.

You can't install Jira Align. You can only install a culture of alignment, and use the software to enforce it. Partners who understand this trade at 12x. Partners who don't are just reselling shelfware.

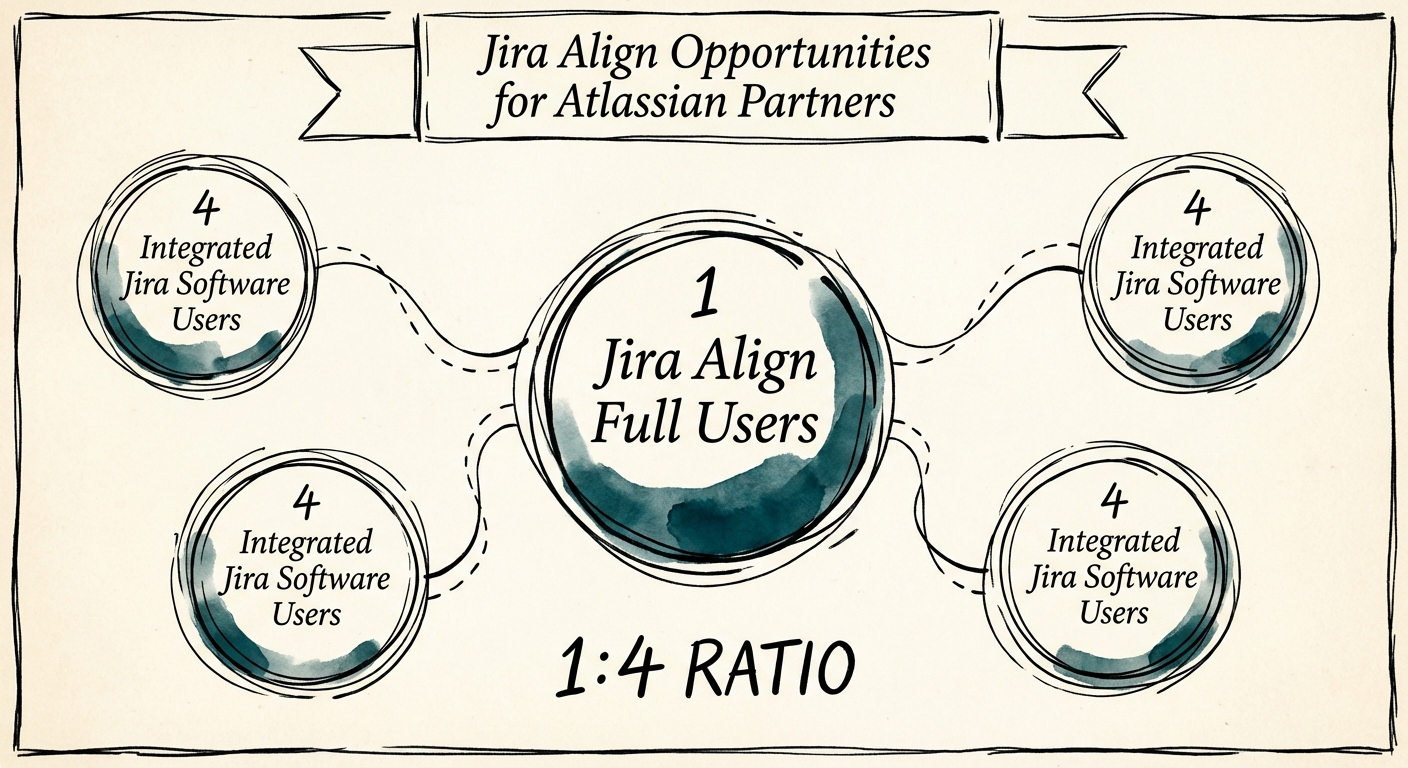

The 1:4 User Ratio: Where Deals Die (Or Scale)

The single biggest mistake Atlassian partners make with Jira Align is treating it like Jira Software. In Jira Software, every developer needs a license. In Jira Align, if you try to license every developer, you will change the deal with price shock before it even reaches the CFO.

Successful partners understand the 1:4 Ratio. Atlassian's architecture assumes that for every 1 'Full' Jira Align user (Portfolio Managers, RTEs, Execs), there are roughly 4 'Integrated' users (Developers) who stay in Jira Software. The value—and the margin—doesn't come from the 4 developers; it comes from the 1 strategist.

The 'Transformation Tax'

When you position the sale around the 'Full' users, you are no longer selling to IT; you are selling to the Office of the CFO or the EPMO. This shifts your bill rate. A Jira Admin bills at $175/hour. An Enterprise Agile Coach bills at $350/hour. By pivoting to Jira Align, you don't just increase your deal size; you fundamentally alter your Revenue Per Employee (RPE), a critical metric for Private Equity buyers. If your RPE is stuck below $220k, you are likely over-indexed on technical configuration and under-indexed on strategic advisory.

The 'Fake Agile' Diagnostic

How do you know if your practice is ready for the Jira Align premium? Private Equity investors look for three specific red flags during due diligence that indicate a 'Fake Agile' shop:

- The 'Plugin' Mentality: If your SOWs focus on 'installing' Jira Align rather than 'mapping value streams,' you are a flight risk. Jira Align fails without process change. If you aren't charging for the process change, the implementation will fail, and you will churn the client.

- The Missing C-Suite: If your primary contact is a Jira Admin, you haven't sold Jira Align; you've sold a headache. True EAP deals require a sponsor at the VP or C-level who cares about Connect Strategy to Execution, not Sprint Velocity.

- The Dependency on Licenses: If more than 40% of your gross profit comes from resale margin, your valuation is capped. With Atlassian's push to direct sales for large enterprise deals, resale is a melting ice cube. Services gross margin is your only defensive moat.

The window to pivot is narrowing. With the Data Center end-of-life looming in 2029 (and sales cutoffs already active), enterprises are forced to rethink their stack. They will either move to Cloud (a commodity move) or move to System of Work (a strategic move). Your multiple depends on which path you guide them down.