The practical answer

- Short answer

- UiPath partners stuck in 'bot building' trade at 6x EBITDA. Those with Intelligent Automation CoEs command 12x. Here is the diagnostic to pivot your model.

- Best fit

- Industry: IT Services & Consulting. Function: Operations

- Operating path

- GTM Execution → Commercial Performance → Performance Improvement

- Key metric

- 70% Failure rate of digital transformation projects without centralized governance.

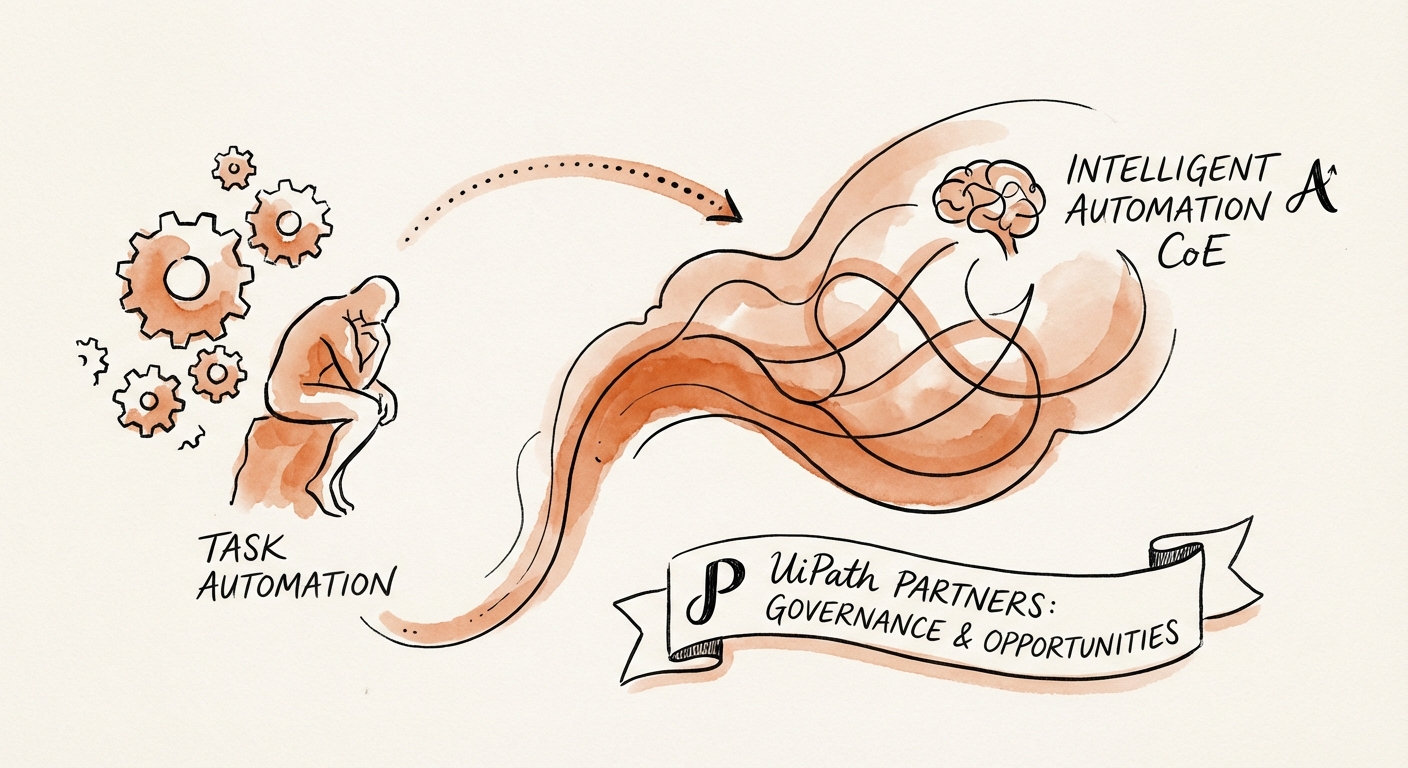

The 'Bot Factory' Commodity Trap

For the last five years, the UiPath partner ecosystem has been fueled by a simple arbitrage: the gap between the promise of Robotic Process Automation (RPA) and the scarcity of developers. Partners built businesses on the "Bot Factory" model—charging project fees to script processes, one after another.

But in 2026, that arbitrage is dead. The commoditization of basic RPA development, combined with the rise of Generative AI code generation, has compressed project margins. What was once a $175/hour billable role is now a $65/hour commodity. More importantly, the "project-based" revenue quality is high-risk to your valuation.

Private Equity buyers penalize pure-play "Bot Builders" because the revenue is non-recurring and fragile. Without a governance layer, individual bots break when underlying applications change, leading to client frustration and churn. Data shows that 70% of digital transformation initiatives fail to meet their objectives, often due to this fragmented, task-based approach. If your firm is merely building the bots that eventually break, you aren't building an asset; you're building technical debt for your clients and revenue volatility for yourself.

Automation without governance isn't a strategy; it's a legacy system waiting to break. The partners who win in 2026 won't be the ones writing the scripts—they'll be the ones writing the rules.

The Pivot: CoE-as-a-Service (CaaS)

The partners commanding 12x+ EBITDA multiples have shifted their value proposition from "Labor" to "Governance." They don't just build automations; they stand up and manage the client's Intelligent Automation Center of Excellence (CoE).

In the "CoE-as-a-Service" model, the partner takes responsibility for the entire automation lifecycle: discovery, prioritization, governance, infrastructure, and maintenance. Instead of a $50k project fee, they charge a $15k/month subscription to manage the program. This shifts the revenue mix from 80% Project / 20% Support to 40% Project / 60% Recurring.

Why This Drives Valuation

Buyers pay for predictability. A CoE contract embeds your firm into the client's operational nervous system. You aren't just a vendor; you are the gatekeeper of their process efficiency. With the arrival of Agentic Automation—where AI agents perform autonomous tasks—the need for strict governance (guardrails, security, auditability) explodes. Partners who own the governance layer become irreplaceable, reducing churn to near zero and increasing Net Revenue Retention (NRR) above 110%.

The Valuation Arbitrage: 6x vs. 12x

The math of this pivot is stark. Consider two UiPath partners, both generating $2M in EBITDA.

Partner A (The Bot Builder) generates $2M EBITDA primarily through one-off implementation projects. Their revenue resets to zero every January 1st. In due diligence, PE firms view this as high-risk. They apply a standard IT Services multiple of 5x-6x.

Exit Value: $10M - $12M.

Partner B (The CoE Partner) generates $2M EBITDA, but 60% comes from multi-year "Managed CoE" contracts. They have visibility into 18 months of future cash flow. Because they manage the platform and not just the script, they trade closer to MSP or SaaS-lite multiples of 10x-12x.

Exit Value: $20M - $24M.

The strategic move for 2026 is not to hire more developers, but to productize your governance. If you cannot demonstrate a standardized CoE framework that generates recurring revenue, you are leaving 50% of your firm's potential value on the table.