The practical answer

- Short answer

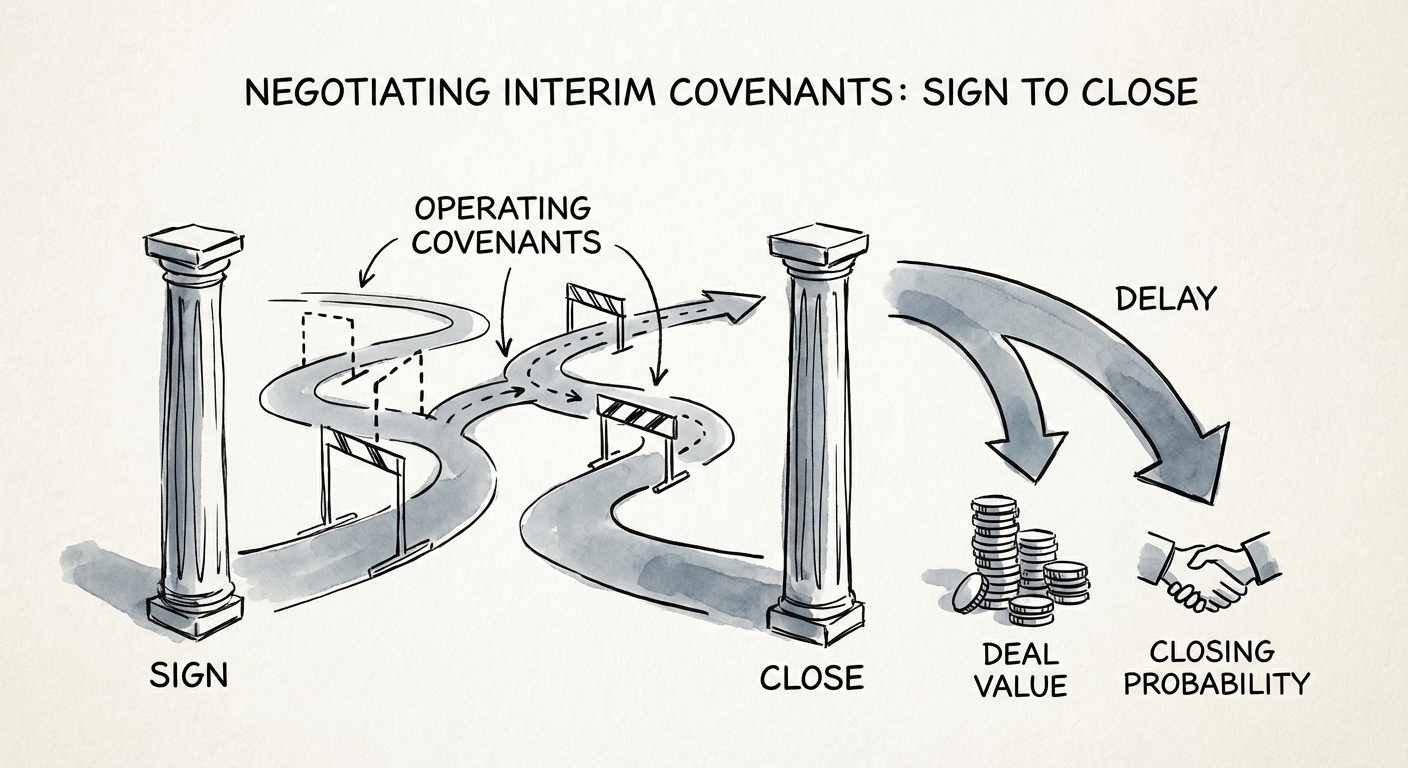

- The period between signing and closing is the most dangerous phase of an exit. Learn how to negotiate interim operating covenants that prevent PE buyers from freezing your business.

- Best fit

- Industry: Technology & Services M&A. Function: Legal & Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 252 Average days from announcement to close in North American M&A, necessitating robust interim operating freedoms.

The 'Ordinary Course' Trap: Why 'Past Practice' Is No Longer Enough

The moment you sign the Sale and Purchase Agreement (SPA) or Merger Agreement, you enter the "Frozen Zone." You are still the legal owner of the business, but the Private Equity buyer now holds a contractual veto over your operational decisions. Their goal is to preserve the asset exactly as it was during due diligence. Your goal is to keep growing it. In 2026, these opposing forces are colliding with more friction than ever.

The standard language in most initial drafts requires the seller to conduct business "in the ordinary course consistent with past practice." Historically, founders viewed this as a throwaway line. It isn't. Recent Delaware Chancery Court rulings, specifically the AB Stable precedent, have used this definition. If your business faces an external shock—a supply chain disruption, a sudden regulatory change, or a competitor's aggressive move—and you take extraordinary measures to survive, you may be in breach of your covenants. If you are in breach, the buyer can walk away without paying a breakup fee, or force a massive price re-trade.

The 2026 Defensive Standard

To protect yourself, you must negotiate three specific modifications to the "Ordinary Course" definition:

- Commercial Reasonableness Override: Do not just agree to "past practice." Insist on language allowing for "commercially reasonable efforts" to respond to emergency situations or changes in the business environment.

- The 'Prudent Operator' Standard: Add a clause permitting actions taken by "prudent operators in similar industries," not just your own operating history. This covers you if the entire market pivots (e.g., adopting new AI compliance standards) and you need to follow suit.

- Deemed Consent Mechanisms: The biggest risk in the interim period is decision latency. If you need to fire a high-risk VP of Sales or sign a $500k contract, you cannot wait two weeks for a PE associate to email you back. Negotiate a "deemed consent" clause: if the buyer does not object within 48 hours (or 2 business days) of a written request, consent is deemed granted.

The interim period is not a waiting room. It is a purgatory where you have all the responsibility of a CEO but only half the authority. Without 'deemed consent' mechanisms, you become a lame duck in your own company.

The 'Veto' List: Negotiating Negative Covenants

Beyond the general "ordinary course" obligation, the buyer will impose a list of "Negative Covenants"—specific actions you are forbidden from taking without their express written consent. In the current market, where 30% of deals face delays extending the interim period to six months or more, these restrictions can strangle your company. You cannot afford to pause your business for half a year.

We are seeing PE firms attempt to lower thresholds aggressively in 2025/2026 drafts. Here is where you must hold the line:

1. The Compensation Straitjacket

The Trap: The buyer forbids any salary increases, bonus payments, or new hires above a low threshold (e.g., $100k) to prevent you from inflating the cost base before they take over.

The Fix: Carve out a "Retention Basket." You need the explicit right to issue retention bonuses or off-cycle raises to key talent who might get jittery during the transition. Negotiate a pre-approved pool (e.g., 3-5% of payroll) that you can allocate at your discretion to prevent a brain drain.

2. The CapEx Freeze

The Trap: A ban on Capital Expenditures over $50k. In a SaaS or tech-enabled services environment, this prevents you from upgrading servers, purchasing necessary software licenses, or initiating implementation projects for new customers.

The Fix: Replace individual project caps with an aggregate "Ordinary Course CapEx Budget." Attach your 12-month budget to the disclosure schedule and state that any spend within that approved budget is permitted, regardless of individual line items.

3. The Commercial Handcuffs

The Trap: A requirement for buyer consent on any new customer contract or renewal with non-standard terms. Since almost every enterprise deal involves some non-standard terms (redlines, payment terms), this effectively inserts the buyer into your sales cycle.

The Fix: Define "Material Contracts" strictly by dollar value (e.g., Top 5 customers only) or duration (contracts >3 years). Do not allow a blanket veto on non-standard terms; instead, specify a "permitted variance" (e.g., discounts up to 15% are pre-approved).

The 'Bring-Down' Condition and MAE Weaponization

The enforcement mechanism for these covenants is the "Bring-Down" condition at closing. The buyer does not have to close if your representations aren't true at the time of closing or if you have breached a covenant. In a volatile 2026 market, buyers are looking for "outs"—reasons to walk away or cut the price if the market turns.

The most dangerous battlefield is the Material Adverse Effect (MAE) clause. Buyers want a broad MAE definition so they can claim that a missed quarter or a lost customer is a "Material Adverse Effect" that kills the deal.

Structuring the 'Burden of Proof'

You must shift the burden. Ensure your MAE definition explicitly excludes:

- General Economic Conditions: A recession or market crash shouldn't kill your specific deal unless it hits you disproportionately hard compared to peers.

- Missed Forecasts: Explicitly state that a failure to meet internal or external financial projections does not, in itself, constitute an MAE (though the underlying cause might).

- The Announcement Effect: Loss of customers or employees caused by the announcement of the deal itself must be carved out. You cannot be penalized because the buyer's reputation scared off a client.

Finally, watch the "Ticking Fee." If the interim period drags on due to regulatory review (HSR, CFIUS) or buyer financing delays, the price should go up, not stay flat. Negotiate a ticker (e.g., 8-10% annualized interest on the equity value) that kicks in if closing is delayed beyond 90 days. This incentivizes the buyer to stop dithering and close the deal.