The practical answer

- Short answer

- Founder's guide to negotiating rollover equity in PE acquisitions. Benchmarks for 2026, Section 721 vs 351 tax traps, and why 'Pari Passu' matters more than percentage.

- Best fit

- Industry: Technology / B2B SaaS. Function: Finance / Legal

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 6.2 Years Average PE holding period in 2025, up from 4.5 years in 2020, making rollover illiquidity a long-term commitment.

The Economics: The "Pari Passu" Battle You Must Win

In the high-stakes theater of Private Equity deal-making, the headline purchase price often distracts founders from the structural reality of their "second bite at the apple." While you may fixate on whether you are rolling 20% or 30% of your proceeds, the far more critical variable is the class of equity you are receiving.

In 2026, with valuation gaps persisting and hold periods lengthening to an average of 6+ years, PE firms are increasingly structuring their equity as Participating Preferred or Senior Preferred, while offering founders Common units. This creates a dangerous misalignment.

The Liquidation Preference Trap

If the PE firm holds Senior Preferred stock with a liquidation preference (often 1x or greater) and a guaranteed dividend (typically 8-10%), and you hold Common stock, your equity is functionally subordinate. In a home-run exit (5x MOIC), this matters less. But in a "sideways" exit—common in today’s vintage where multiple contraction is a real risk—the PE firm gets paid first, and your "20%" stake may be diluted to near zero in economic value.

The Benchmark: Fight for Pari Passu status. This means your rollover equity sits in the exact same security class as the PE firm’s institutional capital. If they get Preferred, you get Preferred. If they get a liquidation preference, you get one too. If they refuse, demanding you take "Junior" or Common equity, you must negotiate a higher upfront valuation to compensate for the significantly higher risk profile of your rollover.

In a sideways exit, the difference between 'Pari Passu' and 'Common' rollover is the difference between a 2x return and a zero.

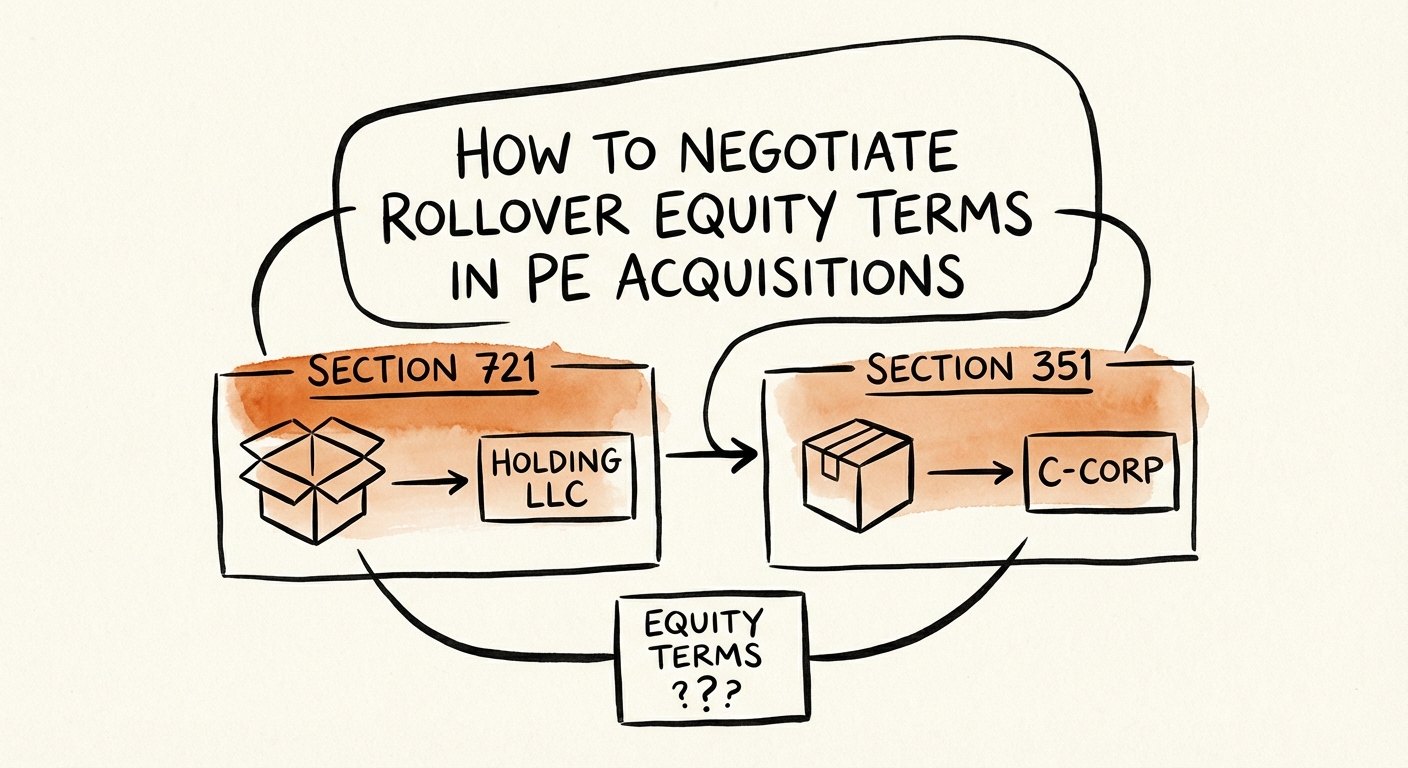

The Tax Trap: Section 721 vs. Section 351

Nothing destroys wealth faster than paying taxes on phantom income. A surprisingly common pitfall for founders in 2026 is failing to structure the rollover as a tax-deferred transaction. If you simply "re-invest" your post-tax proceeds into the NewCo, you are effectively paying capital gains tax on the sale, then buying new illiquid stock with 60-cent dollars. This destroys the compounding power of the rollover.

The "TopCo" Solution

To defer taxes on your rolled equity, the transaction must qualify under specific IRS code sections:

- Section 721 (Partnerships/LLCs): The gold standard for flexibility. It allows you to contribute your existing equity into a new partnership (typically a "TopCo" LLC formed by the PE firm) on a tax-deferred basis. It does not require you to control the new entity.

- Section 351 (C-Corps): Much riskier and harder to qualify for in a typical buyout. Section 351 requires the transferors (you and the PE firm) to fundamentally "control" (own 80%+) of the NewCo immediately after the exchange. If the structure is messy or involves multiple blockers, you could inadvertently trigger a taxable event.

Strategic Advice: Require your M&A tax counsel to validate the "tax-free" status of the rollover in the LOI stage. If the buyer’s structure puts your tax deferral at risk, demand a tax gross-up to cover the liability.

Governance: The Rights of the Minority

Once the deal closes, you are no longer the Captain; you are a passenger. In 2025, we saw a rise in "squeeze-out" mergers where minority shareholders (founders) were forced to sell their rollover at unfavorable terms because they lacked protective provisions.

3 Non-Negotiable Rights

- Tag-Along Rights: If the PE firm sells their stake, you must have the right to sell yours at the same price and terms. Do not get left behind in a partial exit.

- Pre-Emptive Rights (Anti-Dilution): You must have the right (though not the obligation) to participate in future equity issuances to maintain your percentage ownership. Without this, the PE firm can issue new equity to themselves or management pools, diluting you into irrelevance.

- Information Rights: Do not settle for "standard" Delaware statutory rights. Negotiate for monthly financial packages, board materials, and the right to inspect books. If you are rolling 30% of your net worth, you deserve the same visibility as an LP.