The practical answer

- Short answer

- A 90-day operational playbook for new PE portfolio CFOs. From the 13-week cash flow to the 5-day close, here is how to survive the first quarter and secure the exit.

- Best fit

- Industry: Private Equity / B2B SaaS. Function: Office of the CFO

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 5.8 Median years private equity firms now hold portfolio companies (2025), demanding sustained operational value creation over 'quick flips.'

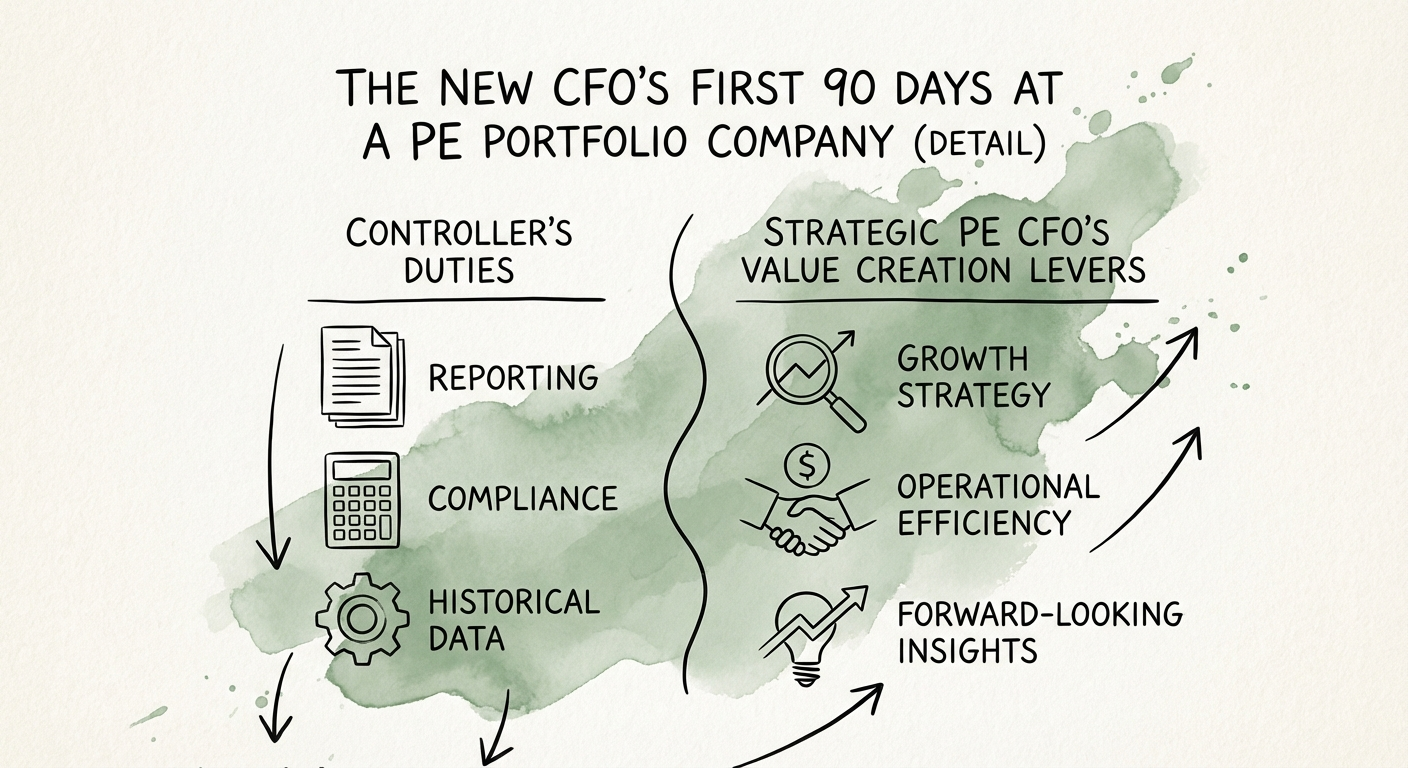

The Era of the "Scorekeeper" CFO Is Dead

If you were hired to simply close the books and manage the audit, you are already redundant. In 2025, the median private equity holding period hit a record 5.8 years. The "quick flip" via multiple arbitrage is gone. Returns are now generated solely through operational execution, and the CFO is no longer just a steward of assets—they are the architect of the exit.

The statistics are brutal: CFO turnover in portfolio companies is at a six-year high, with nearly 1 in 5 finance chiefs leaving their posts annually. Why? because they treat the role like a controller position. They focus on GAAP compliance while the business burns cash. They produce 50-page board decks that look backward while the Operating Partner needs a flashlight to see forward.

Your first 90 days are not about learning the culture or going on a listening tour. They are about establishing financial command. You have three sprints. Execute them, or you will become a turnover statistic.

Days 0–30: The Cash & Truth Audit

Your predecessor didn’t leave because everything was going great. Your first priority is to stop the bleeding you can't see. Most new CFOs inherit a "profitability" narrative that masks a liquidity crisis.

The 13-Week Cash Flow is Your Bible

GAAP P&L is a trailing indicator; cash is the reality. By Day 7, you must implement a direct method, 13-week cash flow forecast. I don’t care if you have to build it in Excel manually. You need to know exactly when the covenants break, not when the model says they might.

The "Dirty Dozen" Data Integrity Check

Trust nothing in the CIM (Confidential Information Memorandum). Launch a forensic audit of the balance sheet immediately. Look for:

- Phantom Inventory: Stock on the books that physically doesn't exist.

- Inactive AR: Receivables over 90 days that are effectively bad debt but haven't been written off to protect EBITDA.

- Accrual Vacuums: Unrecorded liabilities for commissions, bonuses, or warranty claims.

If you find a $2M EBITDA hole in the first 30 days, you are a hero who found "legacy issues." If you find it on Day 91, it’s your miss.

If you find a $2M EBITDA hole in the first 30 days, you are a hero who found 'legacy issues.' If you find it on Day 91, it’s your miss.

Days 31–60: Fixing the Reporting Engine

Once you know the cash position isn't a lie, you must fix the speedometer. In many lower mid-market buyouts, the monthly close takes 20 days. This is unacceptable. A 20-day close means the CEO and Board are lacking operating visibility for two-thirds of the month.

The "Day 5" Mandate

Your goal is a hard close by Business Day 5. This isn't about working harder; it's about eliminating perfectionism in favor of speed. Move to estimates for immaterial accruals. Automate the bank recs. If you are debating a $500 expense classification on Day 12, you are failing the strategic mandate.

The Weekly Flash Report

Do not make the Board wait for the monthly packet. Implement a Weekly Flash Report by Day 45. This simple dashboard should track:

- Cash Balance vs. Forecast (Variance analysis is key)

- Bookings / ARR Movement

- Pipeline Coverage

- Headcount / Open Roles

This builds trust. When the Board sees you tracking the pulse weekly, they stop micromanaging the monthly P&L.

Restructuring the Board Deck

Stop sending 60 slides of GL detail. The Board cares about Value Creation, not accounting minutiae. Your new packet should have five slides that matter:

- Executive Summary: The "So What?" of the month.

- EBITDA Bridge: A waterfall chart explaining the variance from Budget to Actuals (Volume, Rate, Mix, Spend).

- Covenant Monitor: Headroom analysis against bank covenants.

- Sales Efficiency: CAC, LTV, and Magic Number trends.

- Capital Deployment: ROI on recent CAPEX or R&D spend.

Days 61–90: The Strategic Pivot

You have liquidity visibility. You have a reporting engine. Now, you must become the Operating Partner's co-pilot. This is where you transition from "Head of Finance" to "VP of Value Creation."

Forecast Accuracy & The "No Surprises" Rule

The fastest way to lose sponsor confidence in Private Equity is to surprise the sponsor. A missed quarter is forgivable; a surprise missed quarter is fatal. By Day 90, your forecasting accuracy for Revenue and EBITDA should be within +/- 5%.

This requires you to dismantle the "Sales Optimism" typically baked into the CRM. Implement a rigorous pipeline review process where you audit the close dates and probabilities. If the VP of Sales says it's "Committed," you ask to see the procurement email.

Optimizing Working Capital

With hold periods stretching to nearly 6 years, cash efficiency is a valuation lever. Launch a working capital optimization project. Benchmarks show that top-quartile PE portfolios run a Cash Conversion Cycle (CCC) that is 30% shorter than the industry average.

Attack the "Big Three" levers:

- DSO (Days Sales Outstanding): tightening credit terms and automating collections.

- DPO (Days Payable Outstanding): stretching payments to 45 or 60 days where vendor relationships allow.

- DSI (Days Sales of Inventory): Liquidating slow-moving SKUs to free up cash.

The Verdict

The PE CFO role is not for the faint of heart. It is a high-pressure, high-stakes sprint. But for those who can speak fluent EBITDA and fluent Operations, it is the most rewarding seat in the C-Suite. You aren't just reporting history; you're shaping enterprise value.