The practical answer

- Short answer

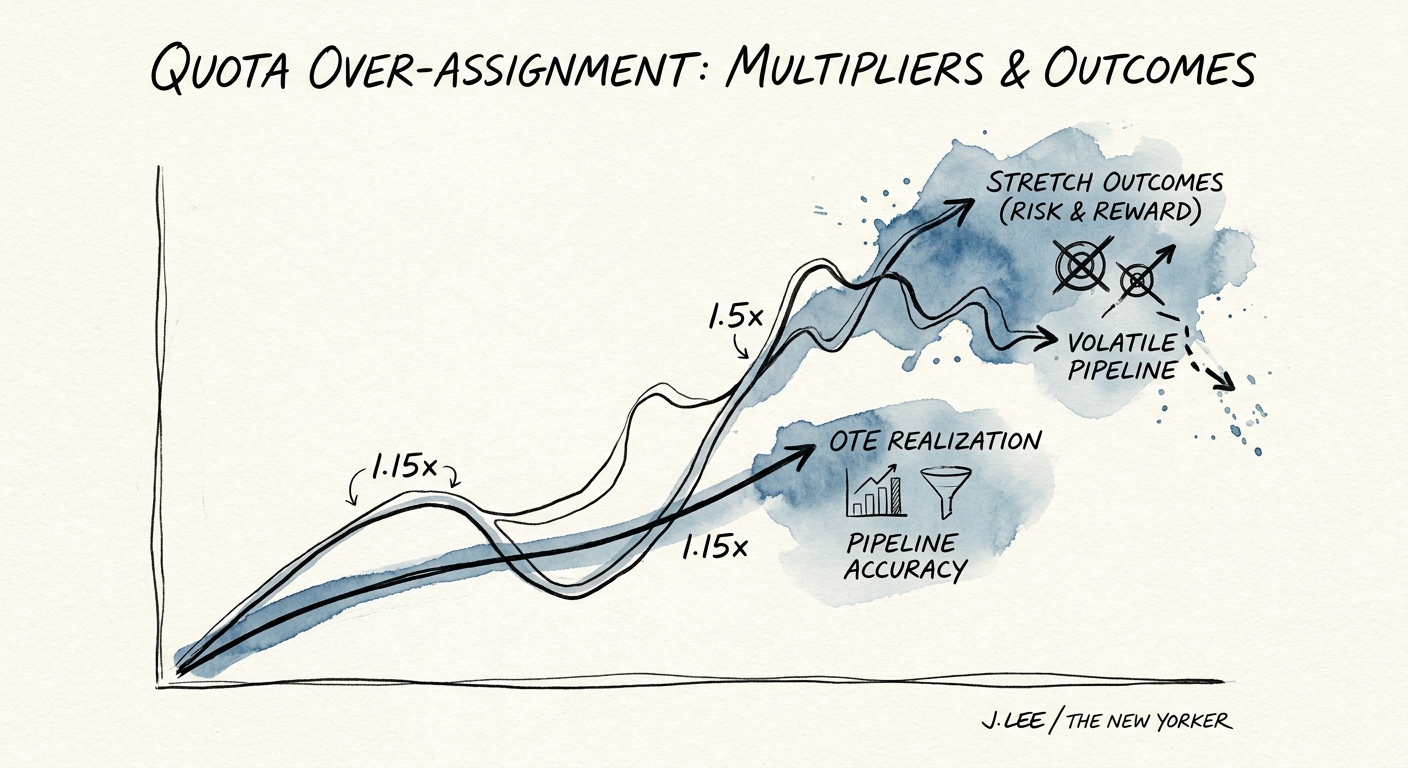

- A 1.5x quota over-assignment multiplier doesn't derisk your board plan. It guarantees ~42% sales attrition. Here's the math, and how to compress to 1.15x.

- Best fit

- Industry: B2B SaaS. Function: Sales Leadership & RevOps

- Operating path

- GTM Execution → Commercial Performance → Performance Improvement

- Key metric

- 42% Guaranteed sales attrition rate when employing a 1.5x quota over-assignment multiplier.

The 1.5x Illusion: A Buffer That Eats the Floor It's Supposed to Protect

Picture the board meeting. The plan calls for $10 million in net new ARR. The CRO pulls up a slide, and the aggregate street quota across the sales floor reads $15 million. "We've over-assigned 1.5x," he says, "so even if only two-thirds of reps make plan, we still hit the number." Heads nod. It feels like prudence. It is, in fact, the moment the company decides to lose roughly four in ten of its sellers before the fiscal year closes.

I've rebuilt this go-to-market motion three separate times across mid-market portfolio companies, and the multiplier always tells the same story. A 1.4x or 1.5x over-assignment is not a hedge against execution risk. It is what leadership reaches for instead of fixing the actual problem: an 18% win rate that should be 30%, or a top-of-funnel that's been starving the floor for two quarters. Inflating the quota doesn't repair either of those. It just spreads the shortfall across people who can't see the spreadsheet and can only feel the number land on their territory.

Here's the part the board slide hides. When you over-assign by 50%, you don't make on-target earnings 50% harder — you make them mathematically unreachable for most of the floor, because attainment was already fragile before you touched it. RepVue's quota attainment tracking shows that across B2B SaaS, only about 43% of account executives hit their number against a normal target. Now stretch that target by another 50% without adding a single lead, and you've quietly handed your mid-tier performers a pay cut they never agreed to. They respond the only way the comp plan lets them: they manufacture pipeline to survive Friday's forecast call. That's how a multiplier becomes a factory for phantom revenue and a pipeline that will never close.

The 1.5x multiplier isn't a strategic buffer. It's a mathematical confession that your revenue operations are broken, signed in your reps' resignation letters.

Run the Arithmetic On One Rep, and the Whole Model Collapses

Take a single enterprise AE. Her territory has produced about $1.2 million in proven annual yield across the last two cycles — that's the empirical ceiling of what the accounts in her patch actually buy. Under a 1.0x plan she'd carry roughly $1.2 million and have a real shot. Under your 1.5x multiplier she's carrying $1.8 million. The gap between what her territory can yield and what her comp plan demands is $600,000 of fiction, and she knows it by the second month. She doesn't escalate. She updates her LinkedIn and takes the recruiter's call. Multiply that decision across the floor and you get what we measure on these engagements: portfolios running a 1.4x to 1.5x over-assignment shed close to 38% of their sellers to voluntary attrition inside twelve months. The buffer you booked on a slide gets paid back as an unbudgeted replacement tax.

The benchmark gap is the tell. Alexander Group's research on sales quotas puts healthy over-assignment in a tight 1.05x to 1.15x band — a real cushion that absorbs ramp and a few misses without breaking the math. The companies bleeding talent are the ones pushing 1.3x to 1.5x while leaving lead flow flat. And replacing that enterprise AE in 2026 isn't a $135,000 line item for recruiting and ramp; that's the visible cost. The hidden one is the roughly half-million in pipeline momentum that evaporates while the seat sits empty and the relationships go cold.

Then the multiplier poisons coaching, which is where it does its quietest damage. When 80% of the floor is pacing at 40% of an inflated number, a sales manager has no signal left. She can't tell the rep who genuinely can't run discovery from the rep whose quota was never solvable — both show the same red dashboard. So the 1-on-1 stops being about win rate and starts being an interrogation of pipeline that everyone privately knows is padded. Gartner's seller burnout research ties this directly to collapsing attainment, with the overwhelming majority of sellers reporting severe burnout when targets are unhooked from territory reality. You can't coach your way out of arithmetic. The first fix is to make the math honest, which starts with a B2B SaaS sales compensation plan where the street target and actual market demand are the same conversation.

Compressing to 1.15x: The Forcing Function CFOs Are Afraid Of

The fix is simple to state and uncomfortable to execute: compress the multiplier to 1.15x, hard ceiling. A $10 million board plan means $11.5 million of aggregate street quota — not $13 million, not $15 million. Every CFO I've walked through this gets the same look, because compression strips away the spreadsheet safety net and forces the company to stand on the true execution capacity of its revenue engine, with nothing to hide behind. That exposure is the entire point.

At 1.15x the fog burns off in a quarter. When a rep misses a rationalized, territory-backed number, the diagnosis is no longer ambiguous — either the sales motion isn't being run or the pipeline generation isn't there, and either way you can act. You manage out the genuine underperformer with a clean conscience instead of carrying them for nine months because you quietly know the quota was never real. Coverage ratios start meaning something again. And you stop tolerating a 15% win rate, because without the fictional buffer to absorb it, that win rate now shows up directly in the gap to plan where the board can see it.

To get there, do the unglamorous work first: rebuild the territory maps and audit historical yield account by account. The standard we enforce across portfolio companies is that every dollar of assigned quota must be backed by roughly three dollars of empirically proven, actionable pipeline capacity. If you can't trace the path by which a rep earns their full OTE, you don't get to hand them that quota. Before you re-cut a single territory, run a sales forecasting accuracy audit — it will show you precisely how much of today's pipeline is defensive fiction generated by people staring down a 1.5x number. Rationalize the multiplier, re-base the quotas on real yield, and the attainment curve and your forecast credibility recover together.