The practical answer

- Short answer

- Stop relying on gut-feel forecasting. Learn how MEDDPICC, economic-buyer evidence, and multi-threading make enterprise close rates more predictable.

- Best fit

- Industry: B2B Technology. Function: Sales Leadership

- Operating path

- Revenue Architecture → Commercial Performance → Office of the CFO

- Key metric

- Economic buyer High-confidence opportunities need confirmed budget authority and decision process.

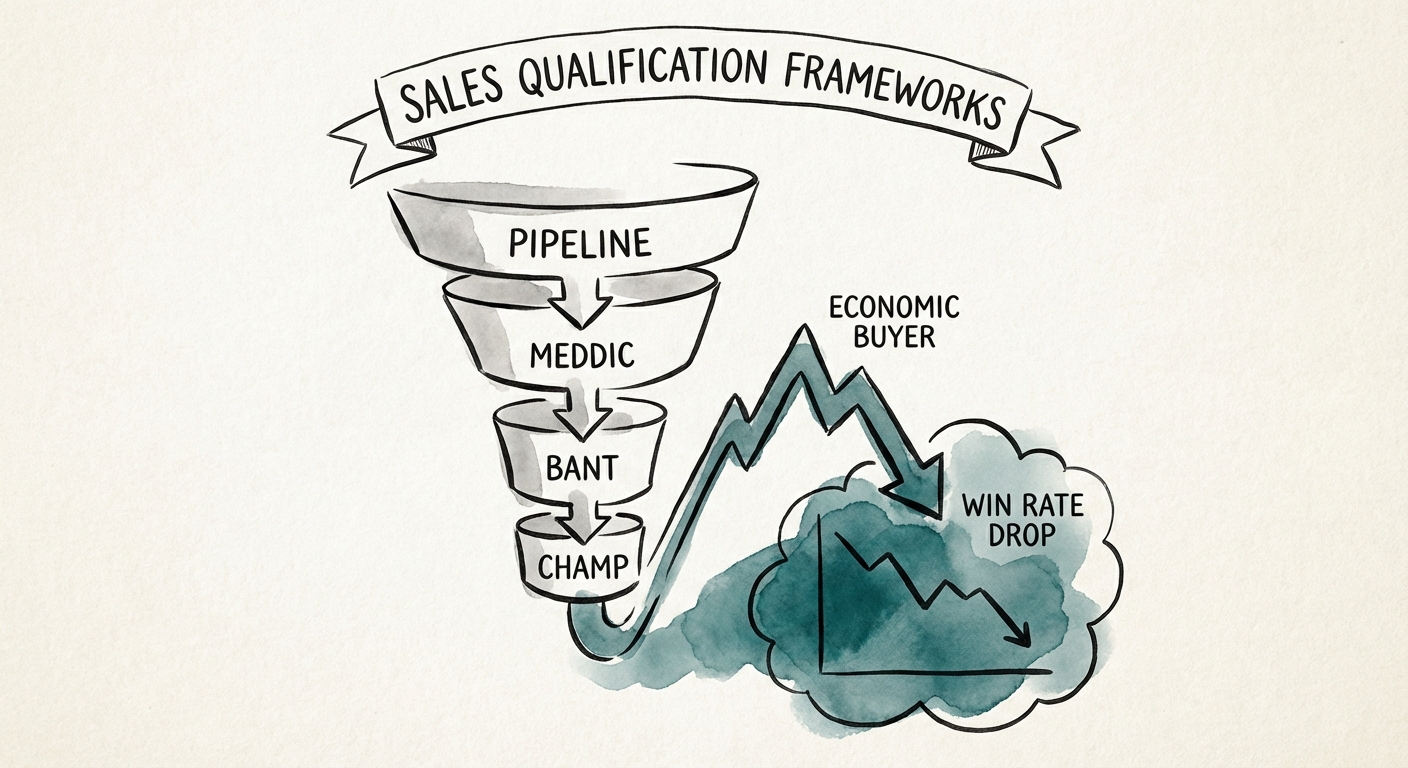

The Weighted Pipeline Problem

For decades, the standard private equity heuristic for pipeline health has been simple: 3x coverage. If the target is $1M, the sales team needs $3M in pipeline. That number is useful as a starting point, but it is not enough to underwrite a quarter.

The problem is qualification quality. A CRM can show "Stage 3: Proposal" with a 40% probability attached, while the rep has not confirmed budget, the economic buyer, paper process, or implementation timing. That is not a forecastable asset. It is an unqualified opportunity wearing a late-stage label.

Probabilistic forecasting also creates false comfort. Ten low-probability deals can aggregate into a neat expected-value number, but enterprise deals close as whole contracts, not fractions. Forecasting needs evidence, not just weighted stage math.

You cannot close 20% of a deal. Forecasting needs buyer evidence, decision process, and commercial next steps, not only weighted stage math.

MEDDPICC as a Predictive Instrument, Not a Checkbox

BANT can work for simple transactions, but enterprise environments usually require consensus buying, security review, procurement, legal process, and executive sponsorship. That is why many teams use MEDDPICC: Metrics, Economic Buyer, Decision Criteria, Decision Process, Paper Process, Implication of Pain, Champion, and Competition.

The acronym only helps if it forces evidence. A rep saying they have access to power is opinion. A calendar invite with the CFO, a mutual action plan, and written decision criteria are evidence. The qualification framework should move the team from sentiment to artifacts.

The Economic Buyer Gate

If the budget holder is not engaged, the deal should not be treated as a high-confidence commit. It may still close, but the risk profile is materially different from a deal where the economic buyer has confirmed the problem, decision process, and commercial urgency.

The Multi-Threading Gate

Single-threaded deals create forecast variance. In larger enterprise opportunities, the champion is only one part of the buying committee. Sales teams need multiple engaged contacts across the business owner, technical evaluator, finance or procurement, and implementation stakeholders.

The PE Operating Partner's Audit Checklist

When evaluating a portfolio company's pipeline, audit for exit criteria, not just entry criteria. Most sales methodologies define what allows a deal to enter the pipeline. Operating partners should focus on what allows a deal to advance.

The Evidence-Based Pipeline Review

Stop asking "How do you feel about this deal?" and start asking for qualification artifacts:

- Stage 2 to 3 Gate: Show the mutual success plan agreed to by the champion.

- Stage 3 to 4 Gate: Show economic-buyer confirmation of decision process and timing.

- Stage 4 to 5 Gate: Show the redlined contract or the specific legal and procurement steps remaining.

Structured qualification does not just improve forecast accuracy. It improves management discipline. A smaller pipeline with evidence-backed opportunities is more valuable than a larger pipeline filled with hope. When qualification aligns with historical win-rate data, leadership can stop debating anecdotes and start managing deal risk.