The practical answer

- Short answer

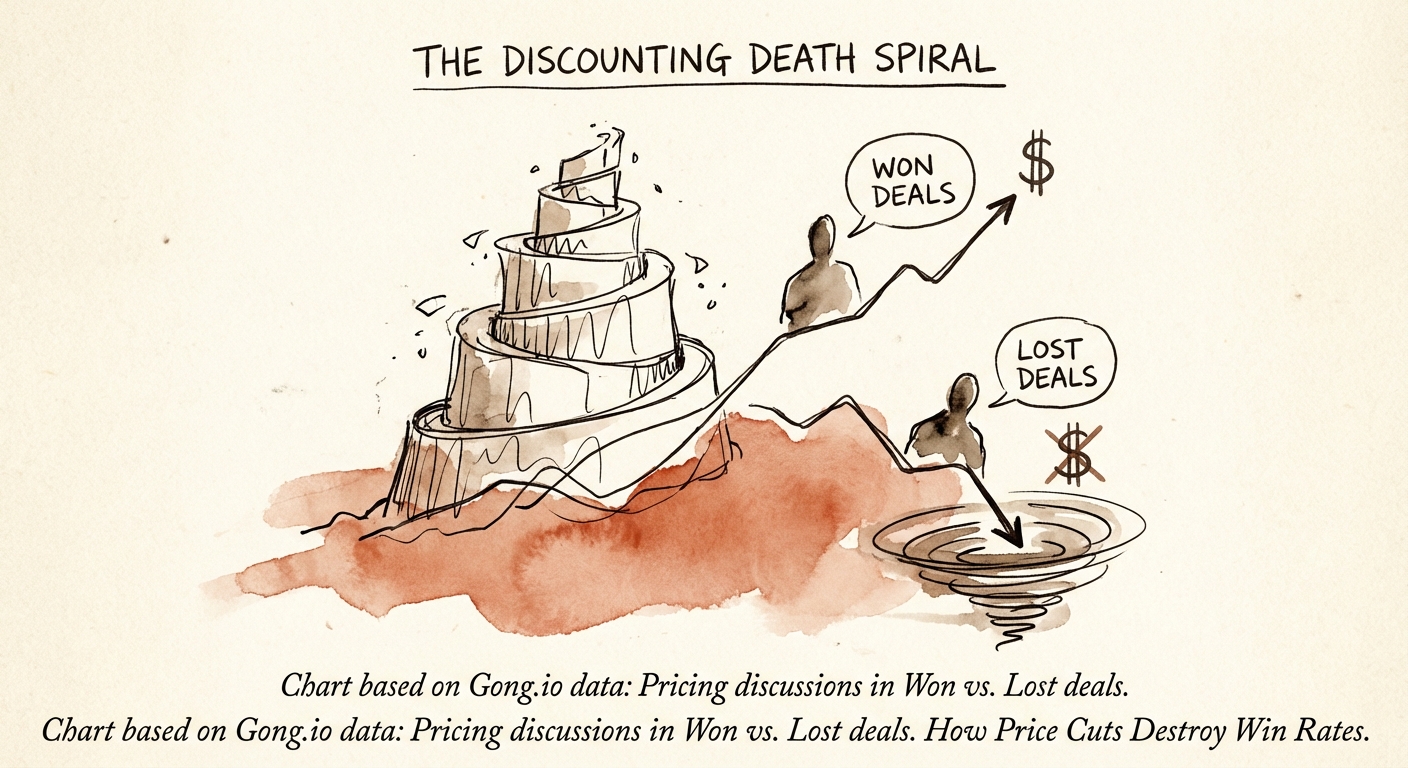

- New 2026 data reveals a counter-intuitive truth: deals with higher discounts have lower win rates. Here is the diagnostic guide for PE sponsors to stop the margin bleed.

- Best fit

- Industry: B2B Technology. Function: Sales

- Operating path

- Revenue Architecture → Commercial Performance → Office of the CFO

- Key metric

- 10% Increase in win rates when pricing is discussed on the first call (Gong.io Data).

The 11.1% EBITDA Mirage

For decades, the standard sales playbook in the final week of the quarter has been predictable: cut the price to close the deal. It is a reflex embedded deep in the muscle memory of nearly every VP of Sales. It is also, according to 2025 data, empirically wrong.

We analyzed deal data across mid-market B2B SaaS portfolios and found a stark correlation that contradicts the "discount-to-win" dogma. Successful deals almost always have lower average discounts than lost deals. Specifically, deals with discounts exceeding 20% actually have a lower win rate than those with discounts under 10%. This phenomenon, known as the "Discounting Death Spiral," occurs because price concessions late in the sales cycle are rarely about price elasticity—they are about value uncertainty.

When a sales rep offers a discount to "create urgency," they are often signaling desperation or commoditization. McKinsey’s data reinforces this, showing that a mere 1% improvement in price realization can yield an 11.1% increase in operating profit. Conversely, the 20% discount granted to "save the quarter" doesn't just erode margin; it statistically reduces the probability of the signature landing at all. In proposal win rate optimization, the data suggests that pricing integrity acts as a trust signal to executive buyers, whereas discounting signals risk.

The "Spillover" Effect

The damage isn't contained to a single deal. New research from the Journal of the Academy of Marketing Science identifies a "discount spillover" effect in B2B markets. When a supplier grants a targeted price reduction to one buyer, it triggers a chain reaction of concession demands from others, eroding profitability by nearly 3x the cost of the original discount. For private equity sponsors, this is a silent valuation killer. You aren't just losing margin on one contract; you are repricing your entire book of business downwards.

Sales reps often argue that higher discounts are necessary to win deals, but our research across companies consistently shows the opposite to be true: successful deals almost always have lower average discounts than deals that were lost.

The Anatomy of a Losing Deal

Why do heavily discounted deals fail to close? The answer lies in the timing of the price conversation. Data from Gong.io analysis of over 1 million sales interactions reveals that win rates are 10% higher when pricing is discussed on the first call. Top-performing reps introduce pricing models between the 38th and 46th minute of the discovery call. In contrast, losing deals typically feature pricing discussions that are delayed until the proposal stage, where the conversation immediately pivots to negotiation rather than value alignment.

When pricing is withheld until the end, the buyer has already framed the solution as a commodity. The request for a discount is a test of that framing. If the rep concedes, they confirm the commodity status. If they hold firm, they force a value conversation—but by then, it is often too late.

The "Rushed Deal" Fallacy

Another correlate of high discounting is the "rushed close." Sales leaders often authorize deep discounts to pull deals forward into the current quarter. However, data from MergeYourData indicates that deals closing in under 7 days have a close rate of just 37%, compared to 67% for deals that follow a 7-14 day closing sequence. The deep discount doesn't buy speed; it buys skepticism. The buyer wonders: "If the price can drop 30% because it's September 30th, was the original price real?" This erosion of trust often stalls the deal in procurement, ironically pushing it into the next quarter anyway—but at a lower contract value.

The 2026 Pricing Discipline Playbook

For Operating Partners and CEOs, breaking the discounting spiral requires a structural shift in how revenue teams are incentivized and managed. It is not enough to simply say "no discounts." You must build a value framework that makes discounting unnecessary.

1. Implement "Give-Get" Trading Rules

Never concede price without extracting value. If a discount is necessary, it must be traded for terms that improve cash flow or predictability. Legitimate trades include:

- Payment Terms: Net 15 or Upfront Annual Payment in exchange for 5%.

- Term Length: 3-year committed contract in exchange for price protection.

- Case Study Rights: Public referenceability in exchange for a one-time credit.

If the buyer refuses the trade, they don't need the discount; they are bluffing.

2. The "No-Decision" Benchmark

Track your "Closed-Lost to No Decision" rate specifically for discounted vs. full-price proposals. You will likely find that discounted proposals have a higher "No Decision" rate. Use this data to show your Board and sales leaders that price isn't the friction point—value is. As noted in our guide on CAC payback benchmarks, inefficient pricing extends your payback period twice: first by lowering the ARR, and second by extending the sales cycle through protracted negotiations.

3. The 38-Minute Rule

Mandate early pricing discussions. Audit discovery calls to ensure reps are anchoring price ranges before the 45-minute mark. This disqualifies mismatched buyers early (saving CAC) and frames the subsequent solution presentation against a known investment level.