The practical answer

- Short answer

- Veeva partners face a historic valuation gap. Why Vault R&D specialists trade at 14x while Commercial CRM generalists stall at 8x. The 2026 exit guide.

- Best fit

- Industry: Life Sciences Technology. Function: Executive Leadership

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14.5% CAGR of the Life Sciences IT market through 2025, driven by R&D digitization.

The 'Vault Migration' Supercycle: A 5-Year Window to Double Your Valuation

In the world of Life Sciences IT, we are entering a \"forced migration\" event that occurs once every decade. With Veeva's divorce from Salesforce and the mandatory transition to Vault CRM by 2030, the entire ecosystem is being reset. For partners, this creates a bifurcated market: those who view this as a \"lift and shift\" project (trading at 8x EBITDA) and those who position it as a \"commercial transformation\" (trading at 14x EBITDA).

The data is clear. Generalist IT services firms—even those with Veeva badges—are seeing multiples compress as PE buyers scrutinize \"body shop\" revenue. Conversely, firms with specialized IP around Vault migration accelerators, data integrity, and automated validation (IQ/OQ/PQ) are commanding premiums comparable to SaaS companies. Why? Because the migration to Vault CRM isn't just a software swap; it is a data governance crisis for pharma companies. Acquirers know that partners holding the \"migration keys\" have locked-in revenue visibility through 2029.

The 2026 Valuation Cliff

Private Equity firms have adjusted their thesis. In 2023, capacity was king. In 2026, competency is king. If your revenue mix is heavy on legacy Veeva CRM administration (Salesforce stack), you are holding a depreciating asset. The \"smart money\" has already moved to the R&D side of the house—Clinical, Quality, and Regulatory—where stickiness is higher and rate pressure is lower.

The migration to Vault CRM is not just a technical event; it is a market consolidation event. Partners who treat it as a 'staffing' opportunity will be acquired for parts. Partners who build IP around the data transition will set the price.

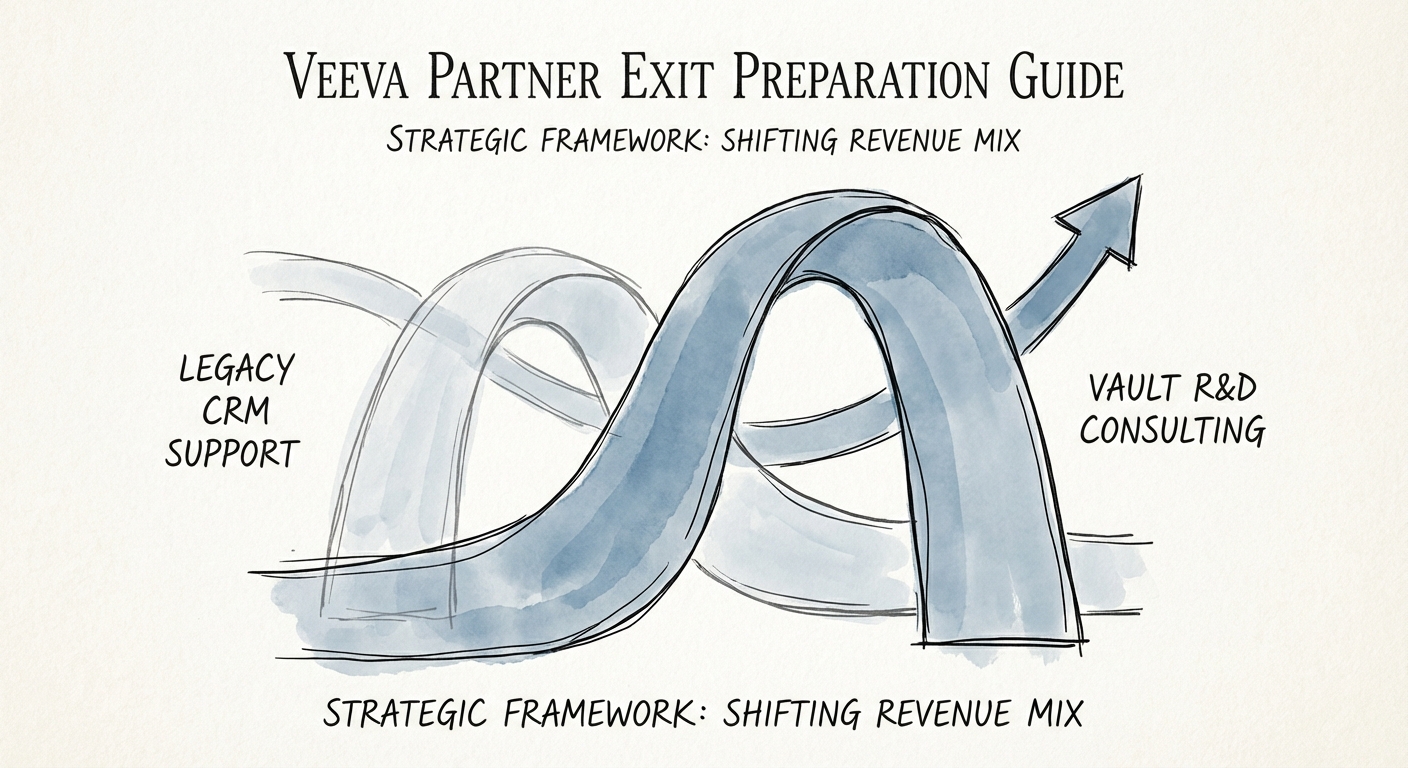

The 'Commercial' vs. 'R&D' Valuation Split

Not all Veeva revenue is created equal. Our analysis of recent M&A activity in the Life Sciences sector reveals a stark \"Valuation Split\" based on which side of the Veeva cloud you service. The market has effectively separated into a Red Ocean (Commercial) and a Blue Ocean (R&D).

The Commercial Discount (8x - 10x EBITDA)

Partners focused primarily on Commercial Cloud (CRM, Events, Align) are facing commoditization. As Salesforce exits the picture, the barrier to entry for \"configuration shops\" lowers. If your team consists largely of admins running ticket-based support for field sales reps, buyers view you as a commodity service provider. The bill rates here ($150-$185/hr) reflect this, and so do the exit multiples.

The R&D Premium (12x - 15x EBITDA)

The real alpha lies in Development Cloud (Vault Clinical, Quality, Regulatory, Safety). Here, the consultants aren't just configuring software; they are interpreting FDA 21 CFR Part 11 requirements. The scarcity of talent who understand both the technology (Vault Java SDK) and the science (Good Clinical Practice) drives bill rates north of $250/hr. PE buyers pay a premium for this because R&D systems are \"systems of record\" for drug approval—they are never ripped out. If you want a 14x exit, your revenue mix needs to pivot toward R&D and Quality.

The 'IP' Multiplier: Automated Validation

In a standard Salesforce practice, IP might look like a \"Lightning Accelerator.\" In a Veeva practice, IP looks like Automated Validation. The single biggest drag on margin in Life Sciences projects is the validation burden—the endless cycle of Installation Qualification (IQ), Operational Qualification (OQ), and Performance Qualification (PQ).

Partners who have built proprietary test automation suites (e.g., using Tricentis or Selenium wrapped for Vault) are trading at significantly higher multiples. Why? Because they can deliver a project 30% faster than a manual competitor while retaining higher margins. In due diligence, we see PE firms specifically asking for \"asset-based delivery\" metrics. If you are billing every hour of validation manually, you are leaving 4 turns of EBITDA on the table.

Actionable Exit Prep Checklist

- Audit Your Revenue Mix: Aim for at least 40% of revenue from Vault R&D/Quality/Regulatory.

- Productize Migration: Build and document a \"Vault CRM Migration Framework\" that is distinct from Veeva's standard tools.

- Certify for Complexity: Shift training budgets from \"White Belt\" admins to \"Vault Java SDK\" developers.