The practical answer

- Short answer

- Why specialized Adobe Experience Platform (AEP) partners trade at 13.6x EBITDA while generalist AEM shops stall at 6x. A diagnostic for PE sponsors.

- Best fit

- Industry: Digital Transformation / MarTech. Function: M&A Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 13.6x EBITDA multiple for Adobe Partners with AEP/CDP Specialization vs. 6.2x for AEM Generalists.

The Great Bifurcation: Why 'Gold' Status Is No Longer a Valuation Driver

In the vintage era of 2018, having an Adobe badge and a bench of AEM (Adobe Experience Manager) developers was enough to command a premium. Private equity firms bought "digital agencies" because the underlying software (Adobe Experience Cloud) was growing at 20%+ annually. That tide lifted all boats.

In 2026, the tide has gone out, and it revealed which firms were exposed. We are witnessing a sharp bifurcation in the Adobe partner ecosystem.

On one side, we have the Generalist Implementation Shops. These firms primarily deploy AEM Sites and Assets. Their revenue is project-based, their margins are compressed by offshore competition (mostly from Global SIs), and their differentiation is "creative heritage." These firms are trading at 5x to 7x EBITDA.

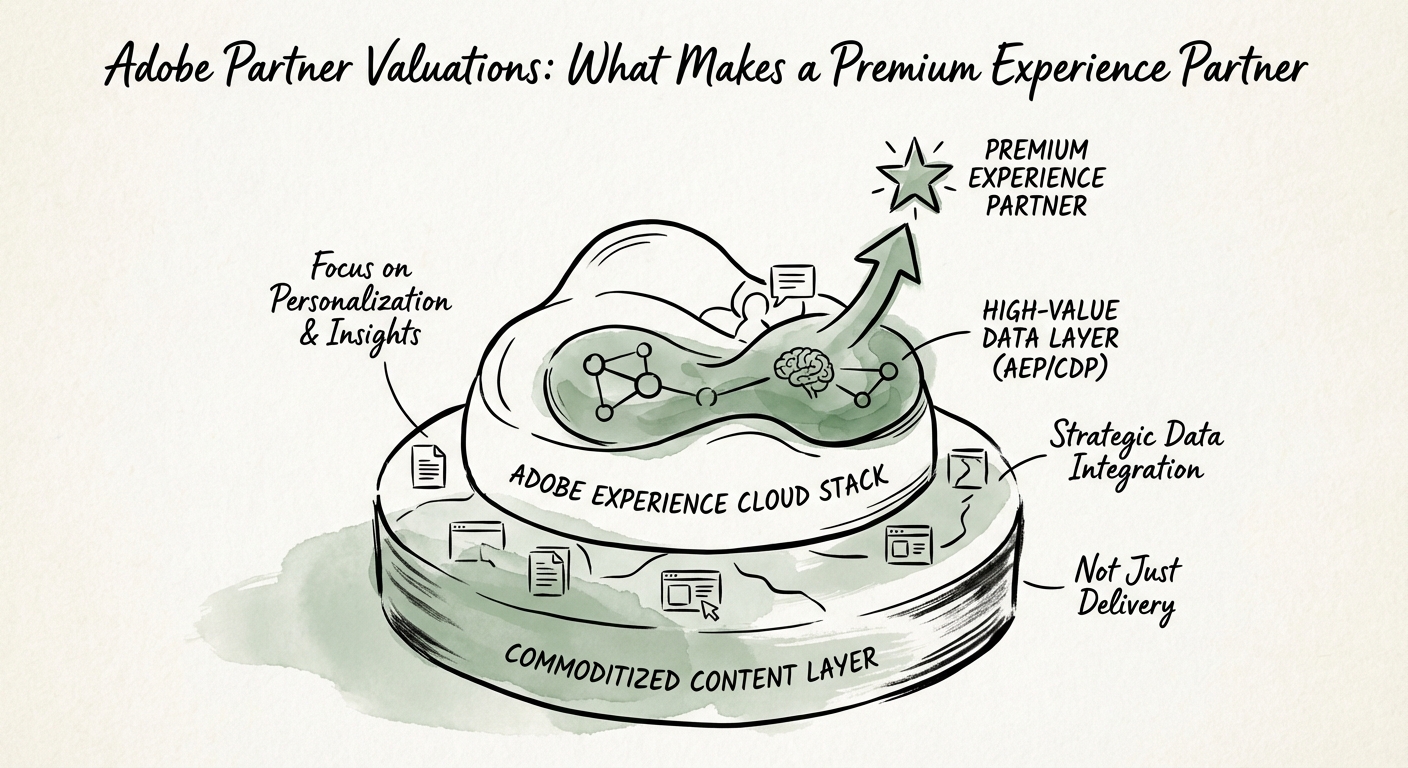

On the other side, we have the Data-First Digital Product Studios. These firms focus on the "hard" side of the stack: Adobe Experience Platform (AEP), Real-Time CDP, and Adobe Commerce (Magento). They don't just "implement CMS"; they architect customer data infrastructure. These firms are trading at 12x to 14x EBITDA.

For Private Equity sponsors, the danger is conflating the two. A "Gold" partner with $20M in revenue might look like a platform target, but if 80% of that revenue is low-margin content authoring and creative services, you are paying a software multiple for a staffing business.

Private equity buyers aren't looking for another AEM shop. They are hunting for the 'data plumbing' experts who can knit AEP, Commerce, and Analytics into a single source of truth. That capability is worth 14x.

The Specialization Premium: AEP is the New Oil

Why does an AEP specialist command a 13.6x multiple while an AEM generalist struggles to hit 7x? The answer lies in scarcity and stickiness.

Implementing AEM Sites is now a commoditized skill. There are thousands of developers who can set up templates and components. However, architecting Adobe Real-Time CDP to ingest petabytes of data, resolve identities across channels, and trigger real-time actions in Journey Optimizer is a rare engineering discipline. It requires data architects, not just web developers.

The Multi-Solution Moat

Buyers are paying a premium for partners who can bridge the gap between Marketing and IT. The "Premium Experience Partner" doesn't just talk to the CMO; they are deeply embedded with the CIO and CTO. They are solving data governance, security, and integration challenges.

Diagnostic Question: Look at your portfolio company's "Active Certifications." If they are predominantly "Certified Professional" or "Certified Expert" in AEM Sites, you own a commodity. If they hold "Specialized" status in Adobe Real-Time CDP or Adobe Journey Optimizer, you own a strategic asset. Adobe's own data shows that Specialized partners drive 3x larger deal sizes, but for an investor, the metric that matters is that they drive 2x higher retention because they own the data layer, not just the presentation layer.

The Revenue Quality Trap: Escaping the 'Project' Hamster Wheel

The final driver of the valuation gap is revenue composition. Traditional Adobe agencies are addicted to the "Big Bang" reimplementation. They pursue large projects, operate at full capacity for six months, and then starve until the next RFP win. This volatility kills EBITDA multiples.

Premium partners have industrialized their IP to create Managed Services revenue streams that go beyond simple support.

- The 6x Shop: Sells "Support Blocks" or "Retainer Hours" for ad-hoc bug fixes. This is low-margin and high-churn.

- The 13.6x Shop: Sells "MarTech Orchestration" or "Data Activation-as-a-Service." They use their own IP (accelerators, connectors, monitoring tools) to manage the client's AEP instance proactively.

If your Adobe partner portfolio company doesn't have at least 15% of revenue from IP-led Managed Services, you are leaving massive exit value on the table. The market does not pay 14x for billable hours; it pays for recurring outcomes anchored by proprietary intellectual property.