The practical answer

- Short answer

- The Copilot sugar rush is over. Discover why Azure OpenAI partners building custom IP are trading at 12x EBITDA while resellers stall at 6x. 2026 Benchmarks.

- Best fit

- Industry: B2B Tech Services. Function: Revenue Strategy

- Operating path

- GTM Execution → Commercial Performance → Performance Improvement

- Key metric

- 70% Failure rate of 2024 Copilot pilots to renew at full volume in 2025 due to lack of demonstrated ROI.

The 'Copilot Sugar Rush' Is Over. Here’s the Hangover.

If you are a Microsoft partner still banking your 2026 growth forecast on reselling Copilot licenses, you are walking into a margin buzzsaw. The 'easy money' era of 2024—where clients bought thousands of seats just to see what would happen—has officially ended. The data from Q4 2025 is brutal for generalists: 70% of pilot programs failed to renew at full volume because CIOs couldn't prove ROI beyond 'email summarization.'

The October 2025 restructuring of the Microsoft-OpenAI partnership didn't just change the cap table; it changed your battlefield. With Microsoft losing exclusive compute rights (though retaining API exclusivity on Azure), the 'lock-in' has shifted. The cloud provider is no longer the moat. The moat is the data layer you build on top of it.

For partners stuck around $15M revenue, this is the 'Integration Gap.' Your clients have the licenses. They have the Azure credits. What they lack is the operational inference layer to make it work without hallucinating. Partners who solve this 'Last Mile' problem are seeing valuation multiples expand to 12x, while pure resellers are being compressed to 6x.

The 'easy money' era of reselling Copilot seats is over. The next $100M of value will be created by partners who can architect reliability into the chaos of inference.

The Money Is in 'Inference Architecture,' Not Licenses

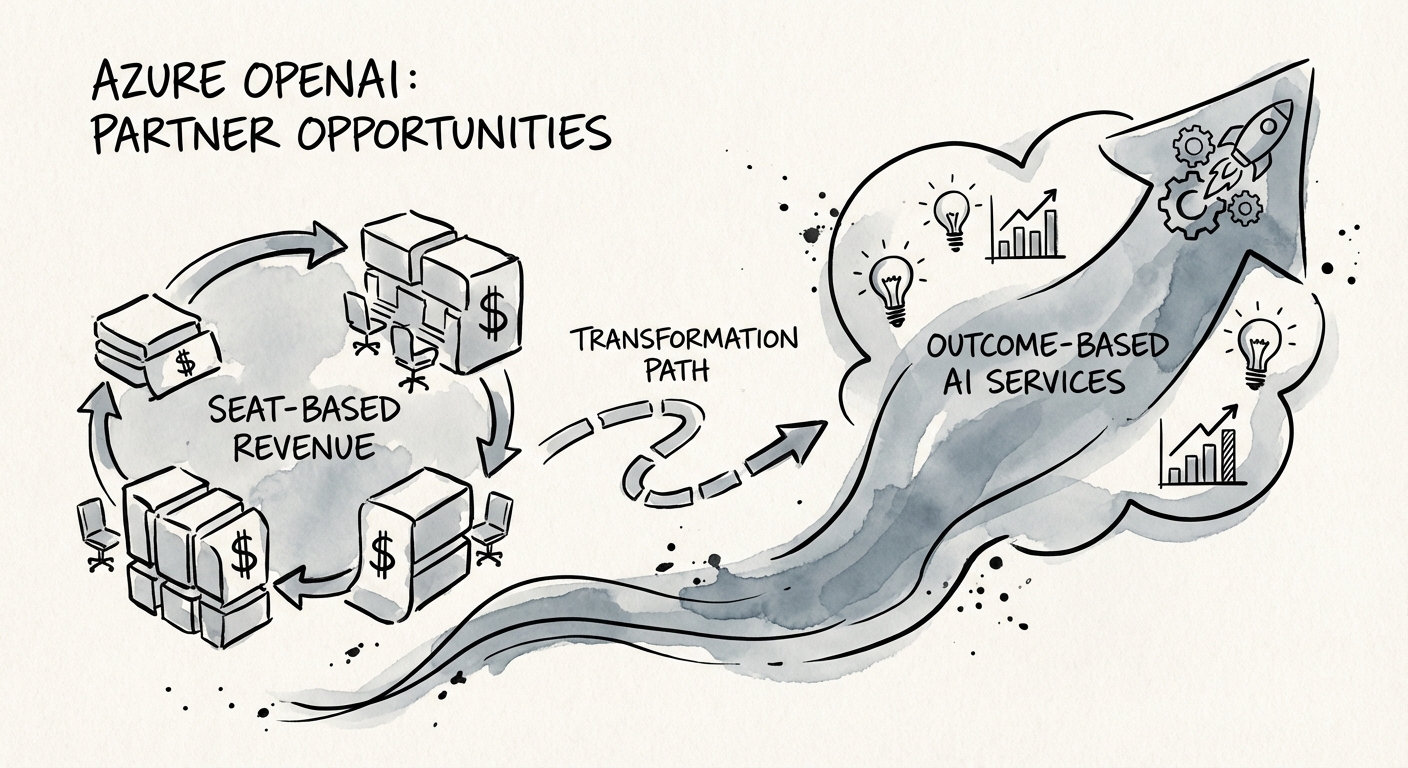

Stop selling seats. The 2026 revenue quality benchmarks are clear: 'Seat-based' revenue is trading at a discount. 'Consumption-based' and 'Outcome-based' revenue is trading at a premium. Why? Because seat-based revenue churns when the CFO does a utilization audit. Outcome-based revenue sticks because it powers a core business process.

According to Forrester's Q4 2025 AI Services report, the primary bottleneck for enterprise AI isn't 'model power'—it's inference cost and reliability. Clients are terrified of variable Azure bills. Partners who can wrap a 'fixed-fee outcome' around a variable-cost Azure OpenAI instance are winning 68% of competitive RFPs.

The 2026 Service Mix Pivot

We are seeing top-quartile partners shift their revenue mix aggressively:

- Legacy Mix: 80% Implementation / 20% CSP Resale. (Result: 15% EBITDA margins).

- 2026 Leader Mix: 40% Data Engineering / 30% AI Model Tuning / 30% Managed 'Inference' Services. (Result: 28% EBITDA margins).

This isn't just about technical capability; it's about escaping the reseller trap. If your 'AI Strategy' is waiting for Microsoft to release a new feature you can turn on, you are a feature, not a business.

Valuation Reality: The 'Generic Partner' Discount

In 2026, Private Equity firms are bifurcating the Microsoft ecosystem. They are looking for 'AI-Native' Service Providers who understand Semantic Kernels, Vector Database optimization, and Agentic Workflows. They are actively avoiding 'Generalist' partners who simply deploy standard models.

The valuation gap is stark:

- Generalist Microsoft Partners: Trading at 5x-7x EBITDA. Viewed as "staff augmentation" with low barriers to entry.

- AI-Specialized Partners (Verticalized): Trading at 10x-14x EBITDA. Viewed as "IP-lite" businesses because they own the industry-specific prompts and data structures.

If you want to break the $20M ceiling, you must stop treating Azure OpenAI as a 'SKU' and start treating it as a development platform. Your intellectual property is no longer the code; it is the context you provide to the model. The partner margin cliff is real for those who refuse to adapt.