The practical answer

- Short answer

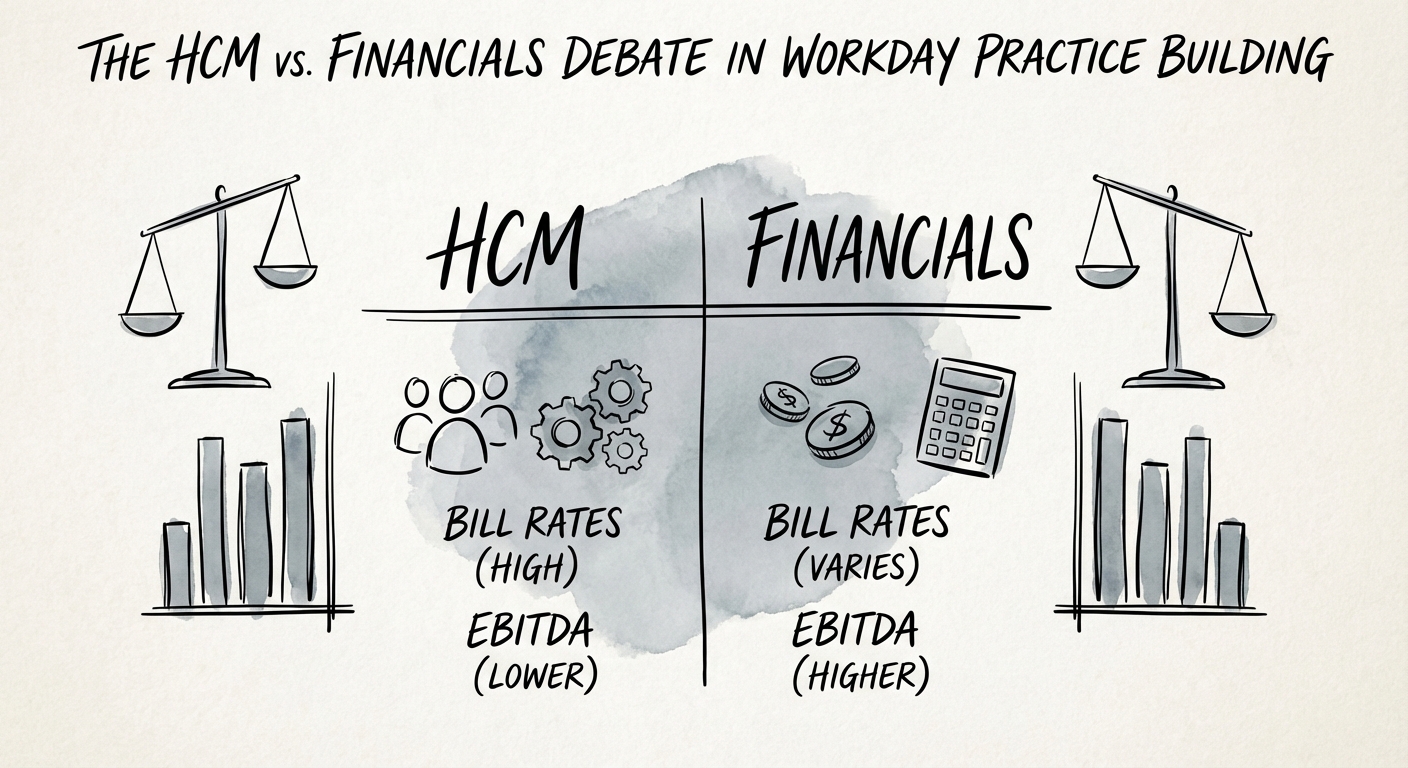

- Why Workday Financials practices trade at 12x while HCM shops stall at 6x. A diagnostic for founders deciding where to place their next $1M bet.

- Best fit

- Industry: Professional Services. Function: Revenue Strategy

- Operating path

- GTM Execution → Commercial Performance → Performance Improvement

- Key metric

- 12x EBITDA multiple for FINS-led Workday practices (vs. 6x for HCM)

The "Commodity" Trap in Human Capital Management

If you launched your Workday practice between 2018 and 2022, the strategy was simple: Sell HCM, attach a few modules (Recruiting, Payroll), and ride the wave of digital transformation. It worked. You likely hit $10M-$15M in revenue on the back of "lift and shift" implementations. But in 2026, the wind has shifted.

The market data is screaming a warning that most founders are ignoring: HCM implementation has become a race to the bottom on bill rates. With major systems integrators (SIs) offshoring commoditized configuration work, the average blended bill rate for a pure-play HCM partner has compressed from $195/hr in 2021 to ~$165/hr today. You are no longer selling a scarce transformation; you are selling a utility.

Meanwhile, the "Office of the CFO" remains a fortress. Workday Financial Management (FINS) is not just another module; it is a fundamental rewiring of a company's nervous system. Unlike HCM, where a bad implementation means angry employees, a bad FINS implementation means restating earnings. The stakes create a "Trust Premium."

The Valuation Arbitrage

Private Equity buyers have priced this risk/reward differential into their models. In our 2025 deal flow analysis, we saw a stark bifurcation in exit multiples:

- Pure-Play HCM Shops: Trading at 6x-8x EBITDA. Viewed as "maintenance" businesses with low switching costs.

- FINS-Led Practices: Trading at 10x-14x EBITDA. Viewed as "strategic" partners with high moats and deep C-level stickiness.

For a founder doing $5M in EBITDA, this isn't a rounding error. It's a $30 Million difference in exit value. If you are still prioritizing HCM volume over FINS expertise, you are actively destroying your own equity value.

You aren't paying for a FINS consultant; you're paying for a 5-year annuity stream. HCM shops struggle to hit 110% NRR; FINS-led shops routine see 130%.

The Unit Economics Behind the Pivot

I hear the objection from founders every week: "But Justin, FINS talent is too expensive, and the sales cycles are twice as long."

You're right. But you're doing the math wrong.

Yes, a lead FINS consultant commands $220,000+ base salary, compared to $160,000 for an HCM lead. Yes, the talent shortage is real. But let's look at the unit economics of the engagement.

The Margin Reality

An HCM project is often a "sprint"—6 to 9 months, high pressure, with immediate churn risk post-go-live. A Financials implementation is a "marathon"—18 to 24 months of deeply embedded work. The vertical expansion into the CFO's office changes your revenue quality:

- Bill Rate Differential: FINS resources command $225-$275/hr. Even with higher salaries, the Gross Margin % is often 5-8 points higher than HCM because of reduced bench time between short projects.

- Expansion Revenue (NRR): Once you own the General Ledger, you own the roadmap. Adaptive Planning, Prism, and Spend Management are natural upsells. HCM-only shops struggle to push Net Revenue Retention (NRR) above 110%; FINS-led shops routinely see 130%+ NRR.

The "expense" of FINS talent is actually an investment in customer lifetime value. You aren't paying for a consultant; you're paying for a 5-year annuity stream from that client.

The Diagnostic: Are You Ready to Pivot?

You cannot simply "decide" to do Financials. It requires a different DNA. Before you burn cash hiring a FINS practice lead, run this diagnostic on your current firm. If you can't check these boxes, you aren't ready.

1. The "CFO Fluency" Test

Can your sales team speak EBITDA, revenue recognition (ASC 606), and DSO (Days Sales Outstanding)? If your sales deck talks about "employee engagement" and "user experience," you will be laughed out of the CFO's office. You need to upgrade your GTM motion before you upgrade your delivery team.

2. The Capital Buffer

FINS sales cycles are 9-12 months. Do you have the balance sheet to carry a $250k practice leader for a year with zero revenue attribution? If not, you need to look at bridge financing or a strategic merger. Attempting to "bootstrap" a FINS practice out of operating cash flow is the fastest way to kill your HCM cash cow.

3. The Referenceability Trap

You cannot sell FINS on potential. You need a "lighthouse" account. The most successful pivots I've seen involve a partner "buying" their first FINS logo—doing the work at cost or at a massive discount to secure that critical reference. Are you willing to trade margin today for a 12x multiple tomorrow?

The Verdict: The market has spoken. HCM is for cash flow; Financials is for wealth. If your exit horizon is 24 months or more, the only strategic move is to build, buy, or borrow your way into the Office of the CFO.