The practical answer

- Short answer

- For GCP partners, Chronicle (Google SecOps) offers a path from low-margin resell to high-margin MSSP revenue. Analysis of valuation multiples, service margins, and execution strategy.

- Best fit

- Industry: Cloud Consulting & MSSP. Function: Revenue Strategy

- Operating path

- GTM Execution → Commercial Performance → Performance Improvement

- Key metric

- 42% Average Gross Margin for Managed Detection & Response (MDR) services in 2025, compared to ~20% for infrastructure resale.

The Generalist's Trap vs. The SecOps Premium

If you are running a generalist Google Cloud Platform (GCP) consultancy with $10M–$50M in revenue, you are likely feeling the squeeze. The era of "easy" lift-and-shift migrations is over. Global systems integrators (GSIs) have industrialized the low-end migration market, compressing margins to 20-25%. Meanwhile, the valuation multiple for generalist IT services firms has stabilized at a modest 8x EBITDA.

However, a new tier of partner is trading at 12x to 15x EBITDA. These firms have pivoted from infrastructure to intelligence. Specifically, they have built Managed Security Service Provider (MSSP) practices around Google Security Operations (formerly Chronicle).

The Valuation Arbitrage

The market signals are clear. Private equity buyers are paying a premium for "stickiness." Infrastructure managed services are commoditized; security managed services are critical. Data from 2025 tech services M&A activity shows a stark divergence:

- Generalist GCP Partners: Valued at 0.8x–1.2x Revenue / 8x EBITDA.

- Specialized SecOps/MSSP Partners: Valued at 2.5x–3.5x Revenue / 14x EBITDA.

For a partner doing $5M in EBITDA, this pivot is the difference between a $40M exit and a $70M exit. The driver isn't just revenue growth—it's Gross Margin. While infrastructure resale margins hover around 15-20%, specialized managed security services (MDR/EDR) are delivering 42% to 55% gross margins.

In simple terms, Google SecOps is a mass risk-reducer. Threats that would have impacted our business no longer do, because we have greater observability, better mean time to detect, and better mean time to respond.

The "Google Scale" Unfair Advantage

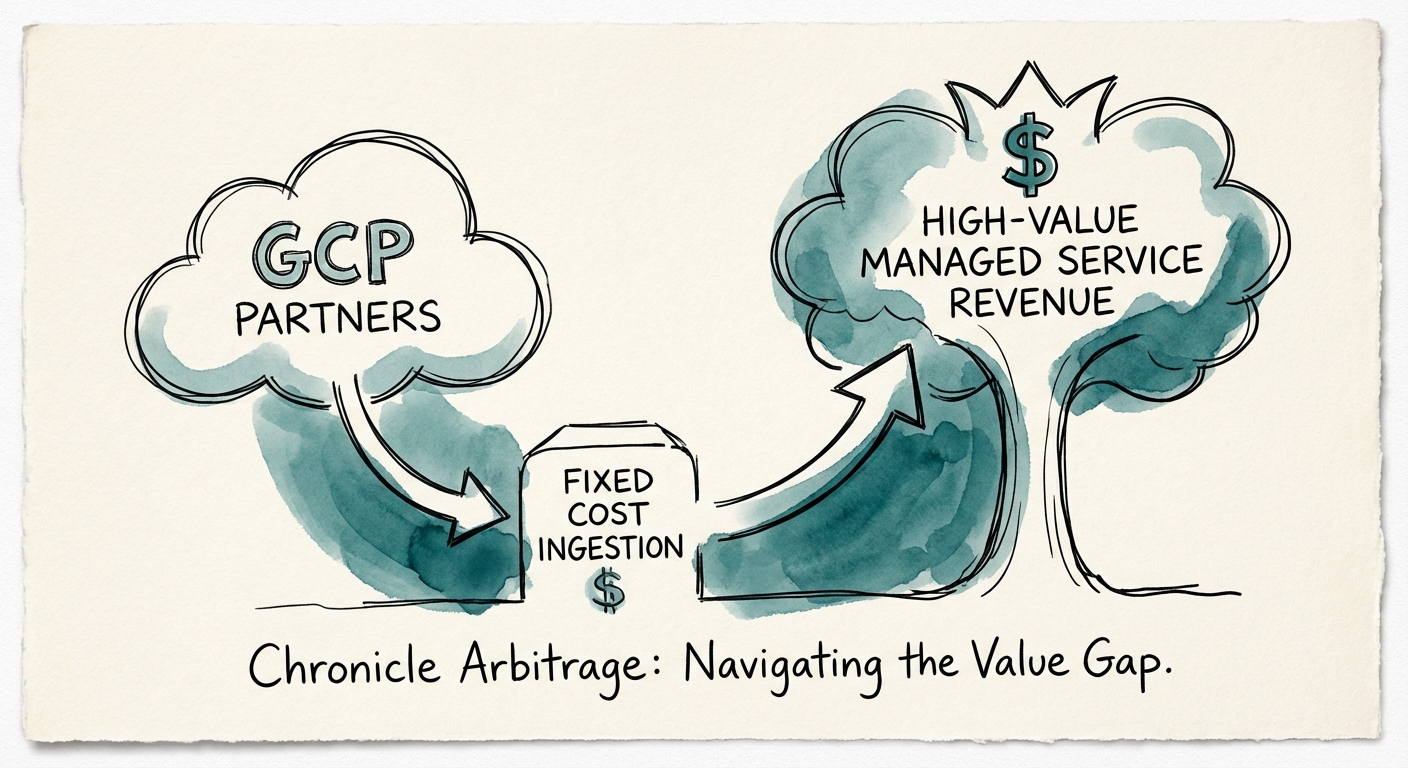

Why Chronicle? Why now? The opportunity lies in the pricing model disruption that Google introduced and partners can exploit. Legacy SIEM providers (like Splunk or Microsoft Sentinel) often charge based on ingestion volume. This creates a perverse incentive where customers are penalized for logging more data, leading to blind spots.

Google Security Operations flips this with a pricing model often tied to employee count or fixed capacity, allowing for "unlimited" ingestion of telemetry. For a partner, this is an arbitrage opportunity:

- Fixed Cost Structure: You pay Google a predictable rate for the tenant.

- High-Value Deliverable: You ingest everything—Cloud logs, EDR, SaaS data—giving the client 100% visibility.

- Service Wrap: You charge the client for the outcome (Threat Detection & Response), not the gigabyte.

The Mandiant Multiplier

The integration of Mandiant threat intelligence into the Google SecOps platform has created a "defense-in-depth" product that mid-market enterprises (your clients) desperately need but cannot build themselves. By wrapping Mandiant's frontline intelligence with your managed services, you are effectively selling "Google-grade security" to mid-sized companies.

According to valuation data on security premiums, partners who own the "risk" relationship with the CISO are viewed as strategic partners, whereas those who own the "infrastructure" relationship with the CIO are viewed as vendors. Strategic partners get renewed; vendors get bid out.

Execution Playbook: From Reseller to MSSP

Pivoting to a Chronicle-led MSSP model requires more than just updating your website. It requires a fundamental shift in your delivery architecture.

1. Stop Reselling, Start Wrapping

Do not sell Chronicle licenses. If you sell the license, the client sees a software cost. If you sell "Managed Threat Detection," the client sees a solution. Bundle the license cost into a per-user, per-month managed service fee. Aim for a 50% gross margin on the bundled offering.

2. The Talent Gap is Your Moat

The biggest barrier to entry for your competitors is talent. SecOps analysts are expensive and hard to find. Leverage Google's AI capabilities (Gemini in Security Operations) to augment junior analysts. Forrester reports that Google SecOps can improve investigation speeds by 50% and reduce the time-to-productivity for new analysts by 70%. Use this efficiency to lower your delivery costs while maintaining high prices for the client.

3. Target the "Splunk Fatigue"

Your sales motion should be surgical. Target organizations with high technical debt in their SOC—specifically those drowning in Splunk renewal costs. Show them a TCO reduction of 30% including your managed service fee. This is the "Chronicle Arbitrage" in action: you lower their total spend while increasing your own margins.

The Window is Closing

Google is currently aggressive with partner incentives to gain SIEM market share. As they move from "Visionary" to established "Leader" (as seen in the 2025 Gartner MQ), these partner incentives will likely normalize. The time to build this practice and lock in the 14x valuation multiple is now.