The practical answer

- Short answer

- A diagnostic guide for PE Operating Partners on merging Azure practices. Covers MCPP consolidation, CSP billing leakage, and preventing rebate loss.

- Best fit

- Industry: Private Equity / Technology Services. Function: Post-Merger Integration

- Operating path

- Migration & Integration → Turnaround & Restructuring → Transaction Advisory Services

- Key metric

- 18mo Average delay in cross-sell realization when 'Infra' and 'Data' sales teams are left unintegrated.

The 'One Microsoft' Trap: Why Financial Integration Isn't Enough

You didn’t just acquire a company; you acquired a Partner Global Account (PGA), a disparate set of Azure tenants, and a completely different billing engine. In the standard Private Equity playbook, integration focuses on the P&L—consolidating back-office functions, rationalizing SG&A, and merging sales teams. In the Microsoft ecosystem, that approach is a material risk for your incentives.

Here is the reality check: Microsoft’s incentives (Rebates and Co-op Funds) often constitute 15-20% of an Azure MSP’s net profit. These incentives are tied to the Microsoft Cloud Partner Program (MCPP) capability scores. When you acquire a target, you are often buying two entities that, individually, might be scraping by with a score of 75 (70 is the minimum for the designation). If you fail to merge the PGAs correctly before the renewal anniversary, or if you split the technical talent pool without mapping them to the correct new PartnerID, you don't just miss synergies—you lose the "Solutions Partner" badge entirely.

We recently audited a portfolio company that acquired a $15M Azure Data shop to complement their $40M Infrastructure practice. Because they delayed the Partner Center merger to "Phase 2" (Month 9), they missed the renewal window. The result? $420,000 in lost rebates over two quarters because the combined entity technically had zero certified staff in the eyes of Microsoft’s automated systems. The lesson: Partner Center integration is not an IT ticket; it is a CFO-level priority.

You didn't buy a company; you bought a PartnerID and a billing headache. If you don't merge the Partner Centers by Day 90, you aren't just missing synergies—you're actively donating margin back to Microsoft.

The 3% EBITDA Killer: CSP Billing Leakage

If there is one place where deal value silently evaporates in Azure M&A, it is in the Cloud Solution Provider (CSP) billing reconciliation. Your platform company uses ConnectWise with a specific API connector; the add-on uses Autotask or a home-brewed Excel spreadsheet. When you merge these customer bases, you enter the "Billing Grey Zone."

The Leakage Math

Benchmarks show that manual or poorly integrated CSP billing results in 1% to 3% revenue leakage. On a $50M Azure resell book, that is $500k to $1.5M in annual pure margin lost. This happens in three ways:

- Orphaned Resources: Azure resources that are running but not mapped to a contract line item.

- Proration Errors: Mismatched dates between Microsoft’s invoice (consumption-based) and your client invoice (often fixed or estimated).

- The "Double-Pay" Trap: Paying for licenses in the acquired tenant while simultaneously provisioning new ones in the platform tenant during migration.

Stop asking "Are the invoices going out?" and start asking "What is our reconciliation variance?" If the answer is "we don't track that," you have a leakage problem. You need a third-party CSP management platform (like Work365 or Cloudmore) implemented effectively on Day 30, not Day 180.

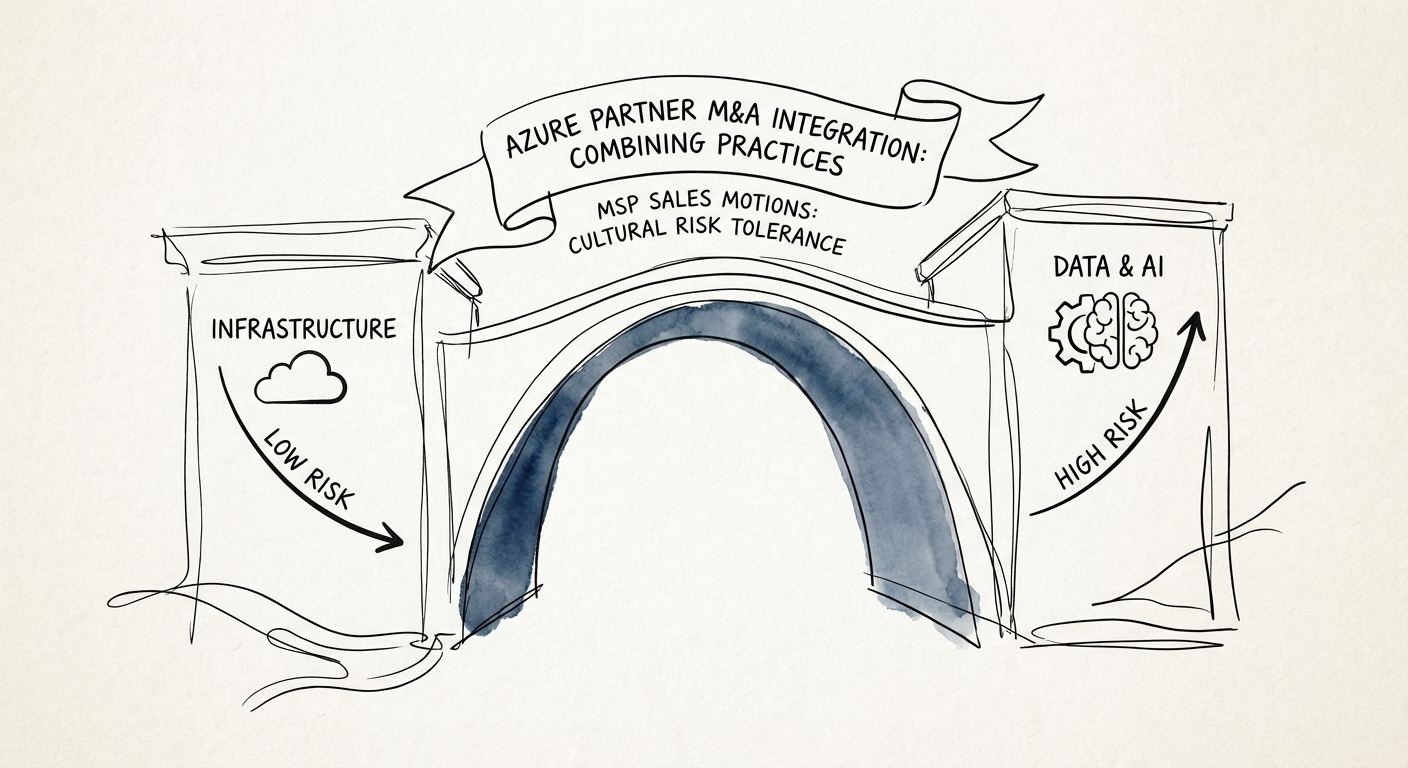

The Culture War: Infrastructure vs. Data & AI

The strategic logic of most recent Azure M&A is "Cross-Sell." You buy a boring, stable Infrastructure MSP (Lift & Shift, Server Migration) and bolt on a high-growth Data & AI shop (Fabric, Synapse, Databricks). The thesis is that you will sell high-margin AI projects to the Infra client base. This rarely works without a specific operational intervention.

Why? Because "Infra" and "App Dev/Data" are opposing cultures.

- Infrastructure Teams sell risk reduction, uptime, and "keeping the lights on." They are conservative.

- Data & AI Teams sell innovation, disruption, and "fail fast" experiments. They are aggressive.

When you merge these practices, the Infra Account Managers (AMs) are reluctant to introduce the Data team because they fear a blown AI project will jeopardize the stable managed services contract. To fix this, you cannot rely on "synergy meetings." You must implement a technical overlay model where Data Architects are incentivized solely on account penetration, not just project delivery, and Infra AMs are protected from churn risk on the core contract. Without this structural safety net, the cross-sell revenue stays at zero.