The practical answer

- Short answer

- Transform your SAP practice from a project-based treadmill to a recurring revenue asset. Learn why recurring revenue commands a 3x valuation premium and how to build it.

- Best fit

- Industry: SAP Consulting & Technology Services. Function: Business Model Strategy

- Operating path

- Revenue Architecture → Commercial Performance → Office of the CFO

- Key metric

- 2.5x Valuation premium of recurring revenue vs. project revenue (Integra Brokers, 2025)

The Project Revenue Treadmill: Why You Start Every Year at Zero

If you are running an SAP consulting firm in 2026, you are likely riding the S/4HANA migration wave. The market is hot. Your pipeline is full. But ask yourself this: What is your firm actually worth?

Most founders I talk to are inhigh-riskated by top-line growth. They see revenue jumping from $10M to $15M and assume their enterprise value is climbing at the same rate. It isn't.

The hard truth of the 2025 valuation landscape is that not all revenue is created equal. According to 2025 data from Integra Brokers, traditional project-based services firms are trading at revenue multiples of 1.01x to 1.37x. Meanwhile, firms with recurring revenue models (Managed Services, IP-led subscriptions) are commanding 2.28x to 2.53x revenue multiples—and often significantly higher (up to 7.0x) if they look like pure-play SaaS.

The "January 1st" Problem

The problem with project revenue is volatility. You kill yourself to deliver a massive implementation, burning out your best architects to hit a go-live date. You secure the revenue, you book the EBITDA, and then the project ends. On January 1st of the next year, your revenue resets to zero. You have to hunt and kill all over again.

This "feast or famine" cycle destroys valuation because it screams risk to a potential acquirer. Private Equity buyers and PE operating partners don't pay premiums for heroics. They pay for predictability. If your revenue depends on you selling a new $2M deal every quarter, you have a job, not a business.

Furthermore, the economics of pure services are deteriorating. Recent benchmarks from Deltek show that average billable utilization rates dropped to 68.9% in 2025, dragging EBITDA margins down to 9.8%. You are working harder for thinner margins, all while building an asset that buyers value at 1x revenue. It’s time to get off the treadmill.

You don't get paid for how hard you work. You get paid for how predictable your revenue is. A dollar of project revenue is worth 80 cents. A dollar of recurring revenue is worth four dollars. Do the math.

The Pivot: Architecting "The Forever Contract"

The shift from project-based to recurring revenue isn't just a pricing change; it's an architectural overhaul of your business model. You cannot simply charge a monthly fee for the same ad-hoc consulting hours. That’s just a retainer, and clients will cut it the moment budgets tighten.

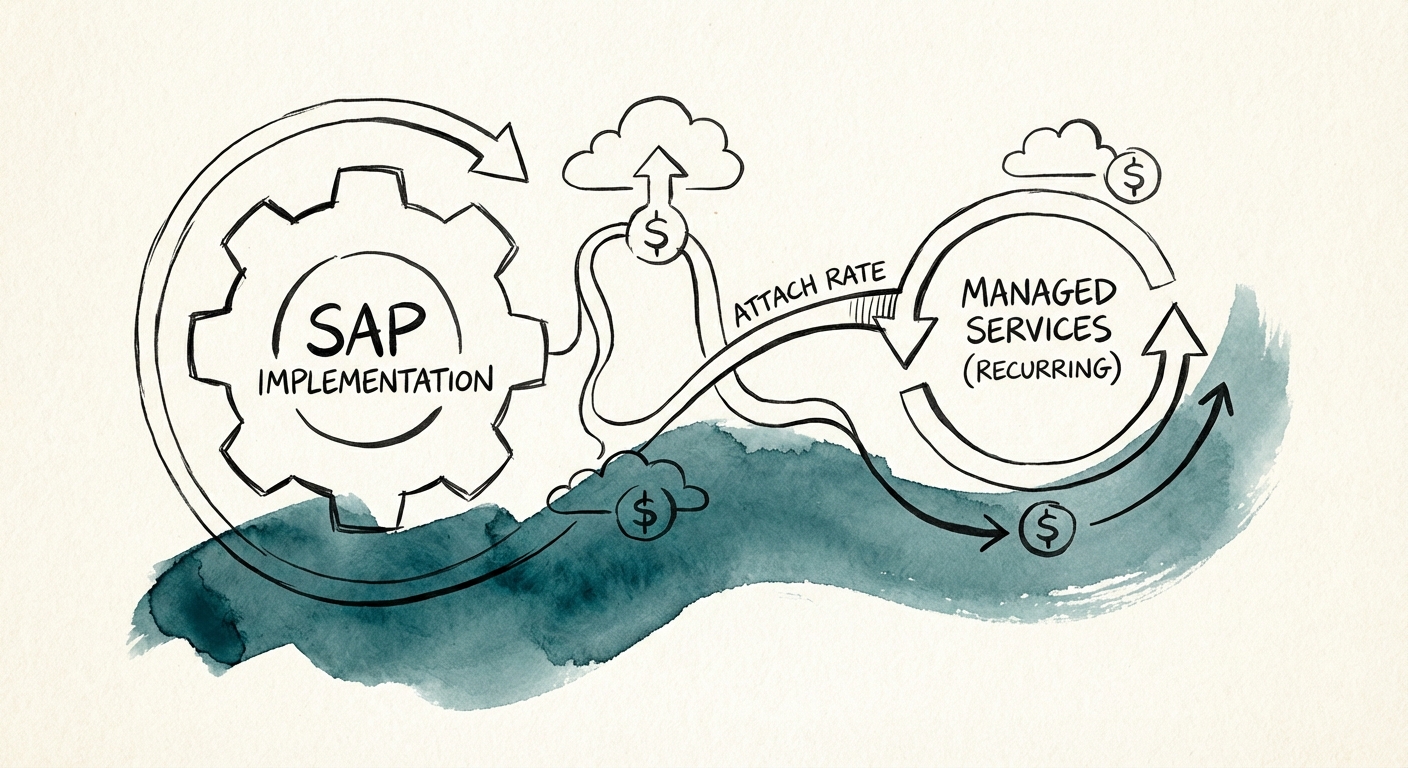

To build genuine enterprise value, you need to productize your expertise into Managed Services and IP-Led Solutions. Here is the blueprint for the "Forever Contract":

1. Application Management Services (AMS) 2.0

Stop selling "break/fix" support. It’s a commodity race to the bottom with offshore giants. Instead, sell "Continuous Optimization." Package your AMS as a strategic service that includes quarterly roadmap reviews, automated testing, and proactive feature activation.

- The Metric: Target an Attach Rate of 50%+. For every implementation project you sign, you must attach a 3-year managed services contract. If your sales team is closing implementations without the AMS tail, they are leaving 60% of the customer lifetime value (LTV) on the table.

2. IP-Led Revenue (The Valuation Kicker)

Identify the custom code you write repeatedly. Is it a specific supply chain configuration for Pharma? A tax reporting add-on for Brazil? Package it. Wrap it in a subscription license.

Even if this IP only accounts for 10% of your revenue, it changes the narrative. It tells a buyer, "We aren't just renting bodies; we own intellectual property." This is how you bridge the gap between a 1x services multiple and a 7x SaaS multiple.

3. The "Land and Expand" Reality Check

Many founders claim they have a "land and expand" strategy, but what they really have is "land and hope." True recurring revenue requires a Customer Success function distinct from delivery. Their sole job is Net Revenue Retention (NRR). If your NRR is below 100%, your recurring revenue bucket is leaking. Best-in-class managed services firms operate at 110-120% NRR, meaning their existing customers grow more valuable every year without a single new logo.

The Exit Arbitrage: Doing the Math

Let’s look at the financial impact of this pivot. This is the math that changes lives.

Imagine two SAP consultancies, both doing $10M in Revenue.

Company A: The Project Shop

- Revenue: $10M (100% Projects)

- EBITDA: $1.5M (15% Margin)

- Valuation Multiple: 5x EBITDA (Typical for pure services)

- Exit Value: $7.5M

Company B: The Hybrid Model

- Revenue: $10M ($5M Projects + $5M Recurring Managed Services/IP)

- EBITDA: $2.0M (20% Margin - recurring is higher margin)

- Valuation Strategy: Sum-of-the-parts

- Project Valuation: $5M Revenue -> ~$1M EBITDA @ 5x = $5M

- Recurring Valuation: $5M ARR @ 5x Revenue (SaaS/Recurring benchmark) = $25M

- Exit Value: $30M

The Result: Company B is worth 4x more than Company A, despite having the exact same top-line revenue. This is the arbitrage. By converting project revenue into recurring revenue, you are essentially transmuting lead into gold.

Stop obsessing over your bookings number for this quarter. Start obsessing over your Revenue Mix. If you are a Founder looking to exit in 24-36 months, your number one strategic priority must be shifting the weight of your revenue from "one-time" to "recurring." The market has spoken, and it is paying a massive premium for predictability.