The practical answer

- Short answer

- Why very high utilization can weaken Databricks partner valuations. 2026 benchmarks for Data Engineers vs. Architects, and the strategy that preserves time for IP.

- Best fit

- Industry: Data & AI Services. Function: Operations

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 68.9% Average PS Billable Utilization in 2025 (Source: SPI Research)

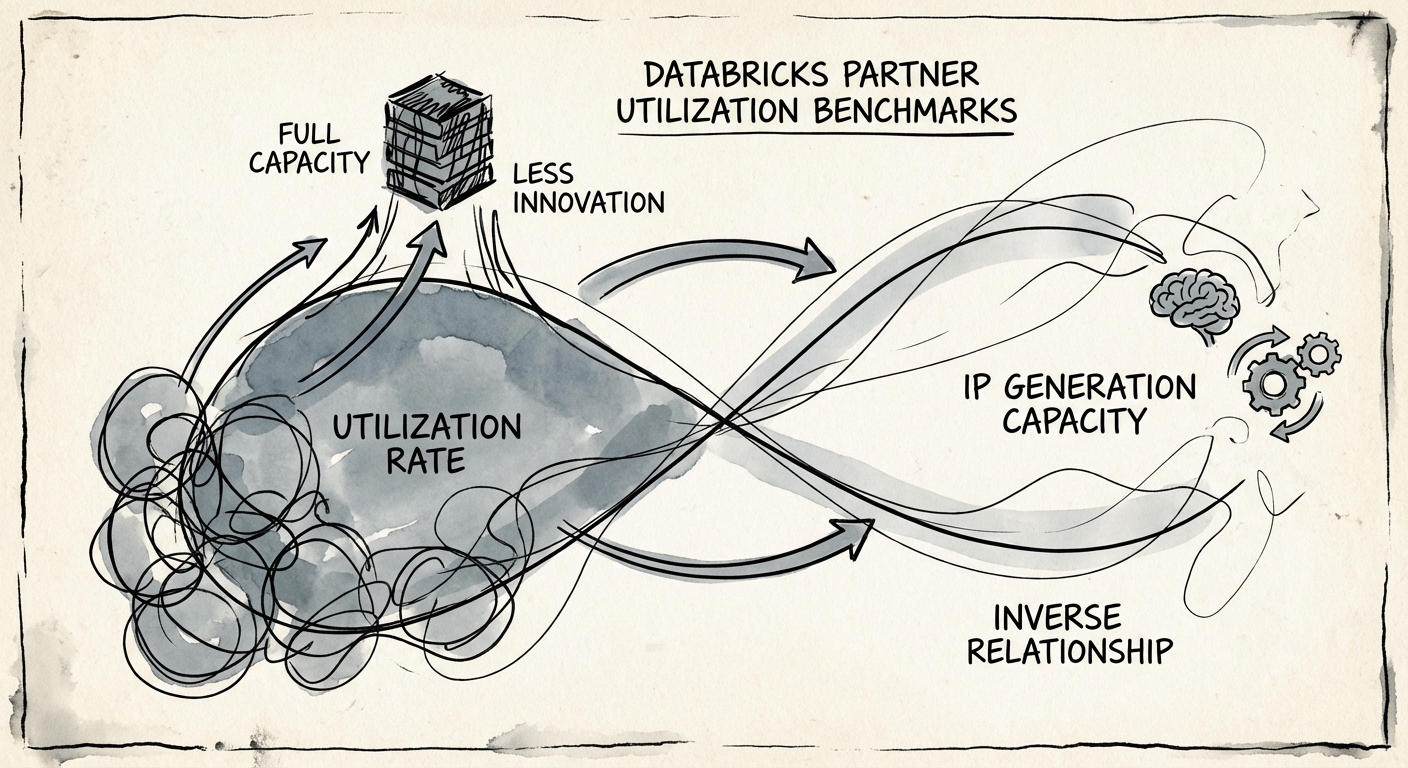

The 'Body Shop' Trap: Why 85% Utilization Kills Deal Value

For most professional services firms, 85% billable utilization is the holy grail. It implies efficiency, demand, and maximized revenue per head. In the Databricks ecosystem, however, sustaining 85% utilization is a leading indicator of a firm that is about to stall.

The Databricks partner economy functions differently than traditional IT staffing. The platform’s velocity—specifically the rapid adoption of Unity Catalog, Delta Live Tables, and MosaicML—renders technical skills obsolete every 9 to 12 months. A Data Engineer billed out at 40 hours a week (100% utilization) or even 34 hours (85%) has zero capacity for the upskilling required to maintain Elite partner status or deliver the high-margin 'Data Intelligence' projects that Private Equity buyers value.

We call this the “Body Shop Discount.” Firms running at 85% utilization are invariably delivering legacy “compute and storage” migrations rather than high-value GenAI implementations. While their P&L looks efficient in the short term, their revenue quality degrades. Buyers see a commodity staffing firm trading at 6x EBITDA, not a specialized strategic partner trading at 12x. The 2025 SPI Research benchmarks indicate that while the broader professional services average has dropped to 68.9% due to market cooling, high-performing Databricks partners deliberately target 72%—not because they lack work, but because they are reinvesting capacity into IP.

In the Databricks ecosystem, utilization is not the whole story. Buyers want to see enough delivery capacity left for IP, specialization, and the next wave of platform demand.

2026 Databricks Role-Based Utilization Benchmarks

Operational excellence in a Databricks practice requires a bifurcated utilization model. You cannot apply a blanket target across your org chart without burning out your Architects or underworking your Juniors. Based on data from top-tier Elite and Select partners, these are the targets you should operationalize in 2026.

1. The Delivery Engine (Junior to Mid-Level Data Engineers)

Target: 78% - 82%

These resources execute the ‘heavy lifting’ of migrations and pipeline construction. Their work is scoped, predictable, and less dependent on cutting-edge features. If they drop below 75%, you have a pipeline or scoping problem.

2. The Strategic Layer (Solution Architects & Principals)

Target: 65% - 70%

This is the danger zone for most firms. If your SAs are billing 80%+, they are not supporting pre-sales, they are not mentoring juniors, and they are not capturing the ‘Harvestable IP’ from projects to build accelerators. SAs must have slack to drive the Consumption metrics Databricks cares about, rather than just burning hours.

3. The Innovation Wedge (GenAI & MosaicML Specialists)

Target: 55% - 60%

This is counter-intuitive but critical. These resources command the highest bill rates ($300/hr+), which compensates for lower utilization. The remaining 40% of their time must be dedicated to R&D—building Brickbuilder solutions and validating new Databricks features. This “unbillable” time creates the defensible moat that drives valuation.

Turning ‘Bench Time’ into 12x EBITDA

The difference between a 72% utilization rate that destroys margin and one that drives valuation is what happens with the non-billable 28%. Low-valuation firms treat the bench as a waiting room; high-valuation firms treat it as an R&D lab.

To command a premium multiple, you must operationalize ‘Bench Management’ into ‘IP Generation.’ Private Equity investors are actively hunting for partners who have productized their service delivery through the Brickbuilder program. Specifically, they look for:

- Industry Accelerators: Pre-built code for specific verticals (e.g., ‘Retail Demand Forecasting on Delta Lake’) that reduces time-to-value by 40%.

- Migration Factories: Automated tooling for converting legacy ETL (Informatica, SSIS) to Databricks Jobs.

- Unity Catalog Templates: Standardized governance frameworks that can be deployed in days, not months.

By capping utilization at 72%, you unlock the capacity to build these assets. This shifts your revenue mix from 100% services (valued at 1x revenue) to a blend of Services + IP (valued at 3x-5x revenue). As noted in our analysis of Data & AI Specialization Premiums, this strategic reinvestment is the single strongest lever for multiple expansion in 2026.