The practical answer

- Short answer

- A 24.8% average discount cost one SaaS company $18M in enterprise value. Here is exactly how a PE buyer's QofE team finds it in your CRM data.

- Best fit

- Industry: B2B SaaS. Function: Sales Operations

- Operating path

- GTM Execution → Commercial Performance → Performance Improvement

- Key metric

- 2x Churn rate for B2B SaaS deals discounted over 20% compared to full-price contracts.

The scatter plot that repriced a $40M company

Last year I sat in a sell-side data room pulling the raw CRM export of a $40M ARR SaaS company. The VP of Sales had just walked the prospective buyer through a beautiful bookings chart: up and to the right, record quarters, a sales machine. So I did what every Quality of Earnings team does. I dumped every closed-won opportunity into one view, plotted discount percentage against the day of the quarter it closed, and colored each dot by rep. Within ninety seconds the room went quiet.

The dots formed a wall. The first eight weeks of every quarter were a sparse cloud of small deals at 8-12% off. Then, in the final three days, a dense vertical column of large deals closed at 25%, 30%, 38%. The "standard" 15% discount this company believed it ran had quietly drifted to a 24.8% blended average over eighteen months. Bookings were up. ARR-per-deal had collapsed. When we modeled the cohort, that drift had erased more than $18M of enterprise value before the buyer ever made an offer.

Here is the part founders miss: the buyer is not reacting to the discount itself. They are reacting to what the shape of that chart reveals. A column of deals jammed into the quarter's last 72 hours says one thing to an operating partner: your reps have exactly one tool to create urgency, and it is your equity. The discounting death spiral starts the instant a rep trades price for a signature without extracting anything structural in return.

Buyers exploit the pattern because they understand it intimately. They sit on the column you accidentally built. They know your rep is staring at a quota gap on a Thursday afternoon, so they hold the signature hostage until you fold. Gartner's research on B2B buying behavior shows just how deliberately modern procurement teams manage that timing. And if your product genuinely returns 10x, cutting 30% off it tells the buyer the ROI story is fiction. You are not winning a logo. You are filing a confession that you have no pricing power.

The scatter plot does not lie. When every closed-won deal clusters in the last three days of the quarter at a 25% discount, a buyer knows your reps are selling the calendar, not the product, and they price you accordingly.

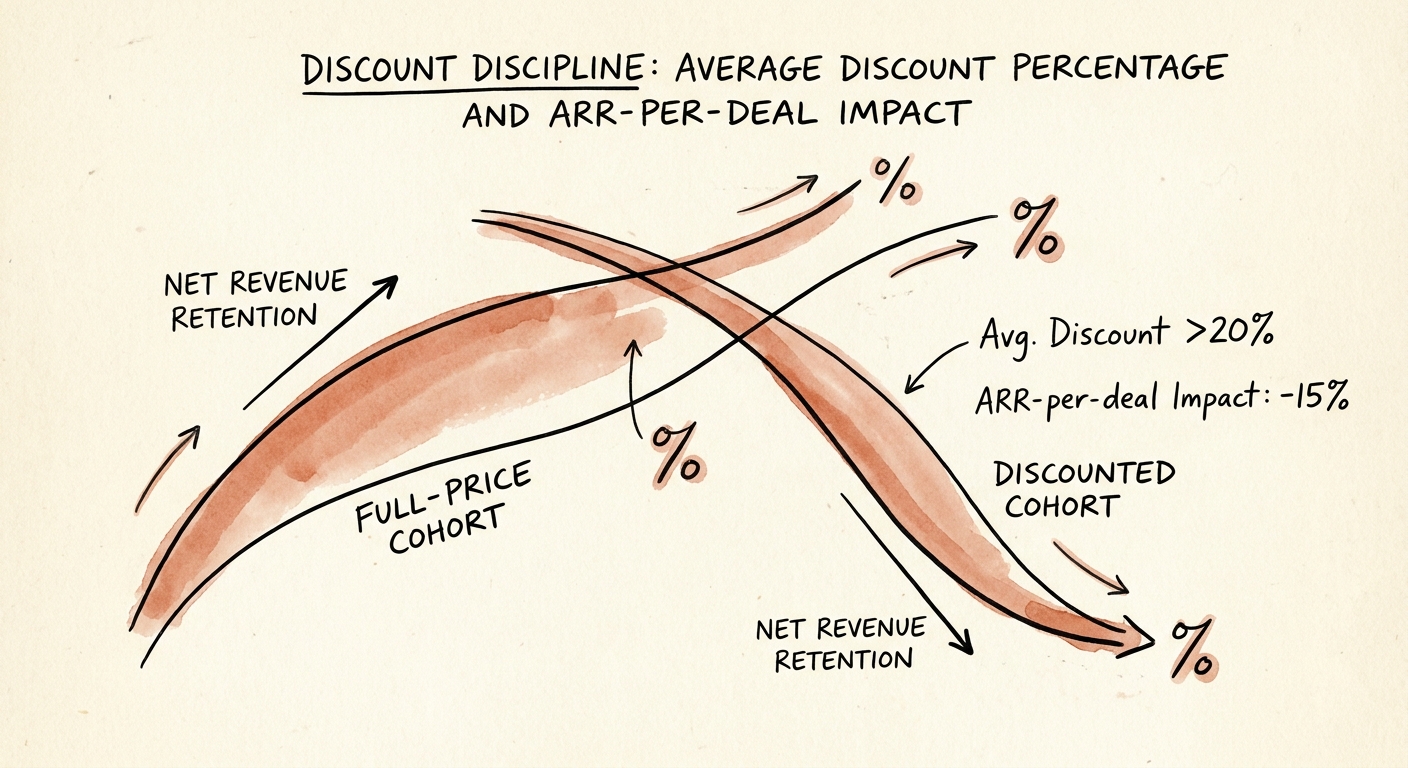

Why a discounted deal is two losses, not one

The first loss is the obvious one: you started ARR-per-deal lower. The second loss is the one that shows up in diligence and ends arguments. ProfitWell's analysis of SaaS discounting found that deals cut by 20% or more churn at roughly twice the rate of full-price contracts. The customer who ground your rep down on price is, statistically, your least committed account, your heaviest support consumer, and the first to leave the moment their own budget tightens. You did not buy market share. You bought a renewal you will probably lose.

Customer Success inherits the liability

The discounted deal does not stay in sales. It lands on a CS manager's desk as a high-risk account that bought your product out of the bargain bin and behaves accordingly. Adoption lags, because customers anchor effort to what they paid. So CS burns disproportionate cycles fighting to keep an account that is already underwater on margin. The cohort in your bottom quartile of realized price routinely carries a noticeably higher cost-to-serve. You are spending more to retain less. That is not a rounding error in a model; it is a structurally broken unit economic.

The renewal math that handcuffs NRR

Walk the arithmetic, because this is where heavy discounting quietly caps your story. Say a deal carries $100,000 of list value and your rep closes it at $75,000. At renewal, a healthy 7% uplift on that $75K yields about $5,250. To merely claw back to the price your software was actually worth on day one, you would need a 33% increase — which triggers a procurement escalation and, often, the churn event you were trying to avoid. Your ability to calculate Net Revenue Retention and tell a premium expansion story starts from a crippled baseline you can never honestly recover.

And the EBITDA cost compounds the damage. McKinsey's pricing research found that a 1% improvement in price realization translates into an 8.7% lift in operating profit. Read that backward: every point of average discount your reps surrender on a Friday is detonating roughly 8.7% of operating profit per point. In a market where buyers underwrite on gross margin and EBITDA rather than top-line, you are handing frontline reps a dial connected directly to your exit multiple — and they are turning it to make their number.

How to rebuild the dial so reps can't reach it

You will not train your way out of this. I have tried, and a one-day pricing workshop survives until the next quarter-end gap. You have to re-engineer the process so that reaching for a discount is the painful path, not the easy one. Start with comp. Decouple commission from gross bookings and tie it to realized price: if a rep discounts a deal 20%, their commission rate on that deal should fall more than proportionally — drop it 40%. Now the rep's wallet and your enterprise value point the same direction. Traditional OTE structures reward closing bad revenue, which is precisely how you built the column in the first place.

Make discount a currency, not a closing tool

Install a rigid give-get. A discount stops being a lubricant and becomes something you sell back. A prospect wants 15% off? Then they sign multi-year with no early-out, agree to a quarterly reference call, and pay annually upfront. No structural concession, no discount, full stop. I have rebuilt this inside three portfolio companies and the pattern repeats: deal velocity dips for about 30 days while reps relearn how to sell, then ARR-per-deal climbs 18-24% and win rates stabilize, because the rep is now forced to defend business value instead of waving a price cut.

Teach the team to walk

A deal that needs 40% off to close is not a win you booked; it is a precedent you set. Buyers in the same market talk. The day you become "the vendor who caves at month-end," you have forfeited pricing power across your entire pipeline, not just one logo. Establish a hard floor and require the rep to politely withdraw when a prospect breaches it. Killing a deal that would have hit your quarterly target takes real nerve from a CEO — that nerve is the line between a 5x and a 12x multiple.

Then close the gate. Anything past 10% requires a written business case from the VP of Sales naming the specific structural advantage the company gains in exchange. Forcing reps to justify, in writing, their inability to sell value to a CFO does something a memo never will: the volume of discount requests quietly drops on its own. Do this now, while it is a process decision you control — or do it later, in a data room, where a buyer does it to your valuation for you.