The practical answer

- Short answer

- Two Azure partners with identical $2M EBITDA can be worth $12M apart. Here is how to convert project work into Lighthouse-leveraged recurring revenue.

- Best fit

- Industry: Cloud Services / MSP. Function: Revenue Operations

- Operating path

- Revenue Architecture → Commercial Performance → Office of the CFO

- Key metric

- 12x EBITDA multiple for Premium MSPs (>70% Recurring Rev) vs 4-6x for Project Firms.

Two Azure partners, same EBITDA, $12M apart

Picture two Microsoft Partners. Both did $9M in revenue last year. Both cleared $2M in EBITDA. Both are Azure shops run by a founder who can still recite the firewall rules from memory. On paper they are twins.

One sells migrations, modernization, and the occasional landing-zone build. Lumpy work. Every January the pipeline resets to zero and the team starts hunting again. That founder is a System Integrator, and in the 2026 market integrators trade at roughly 4x to 6x EBITDA — call it $10M.

The other founder runs 70%-plus recurring revenue through standardized managed-services contracts on top of the exact same Azure workloads. Premium MSPs in that band trade at 9x to 12x EBITDA (see First Page Sage's 2025 multiples report and Viaductus's IT-industry overview). Call it $22M.

Twelve million dollars of enterprise value, decided entirely by how the revenue is shaped — not how much of it there is. That is the trap. Project revenue feels like the win because the invoice is big and it lands now. But a $500K migration is a one-time event that a buyer discounts to almost nothing in diligence, because nobody can underwrite it recurring. The retainer you forgot to attach to it is the asset.

A CSP markup is a 6% commission a client can cancel by email. A flat-fee governance wrapper on the same Azure tenant is a 45% margin they will not rip out without a board fight. Same workload, two completely different exits.

Reselling Azure is not a business — it is a billing relationship

Here is the conversation I have with Azure founders constantly. They tell me they are already an MSP because they transact Cloud Solution Provider (CSP) licenses and bill the client's consumption. Then they wonder why their valuation conversation goes nowhere.

Transacting CSP is a distribution mechanic, not a moat. The partner margin on pure Azure resale runs roughly 4% to 15% depending on tier and incentives, and — this is the part founders underrate — it is the most rippable revenue you own. A client can re-point their CSP relationship to a competitor with one email and a billing-profile change. You did not lose a contract; you lost a permission. There is no switching cost because you never built one.

Margin lives in the layer above consumption

The economics flip the moment you stop billing the client's compute and start billing your own intellectual property on top of it. That wrapper — security posture, identity hardening, cost governance, compliance attestation — is where gross margin climbs from the mid-teens to 45%+, because the client is now paying for an outcome they cannot reproduce internally, not a license they could buy direct.

The two sentences that separate the two valuations:

- The commodity: "We resell your Azure licenses at a small markup."

- The asset: "We run a flat-fee Azure governance, security, and FinOps function so your tenant stays patched, compliant, and right-sized — and we eat the variance."

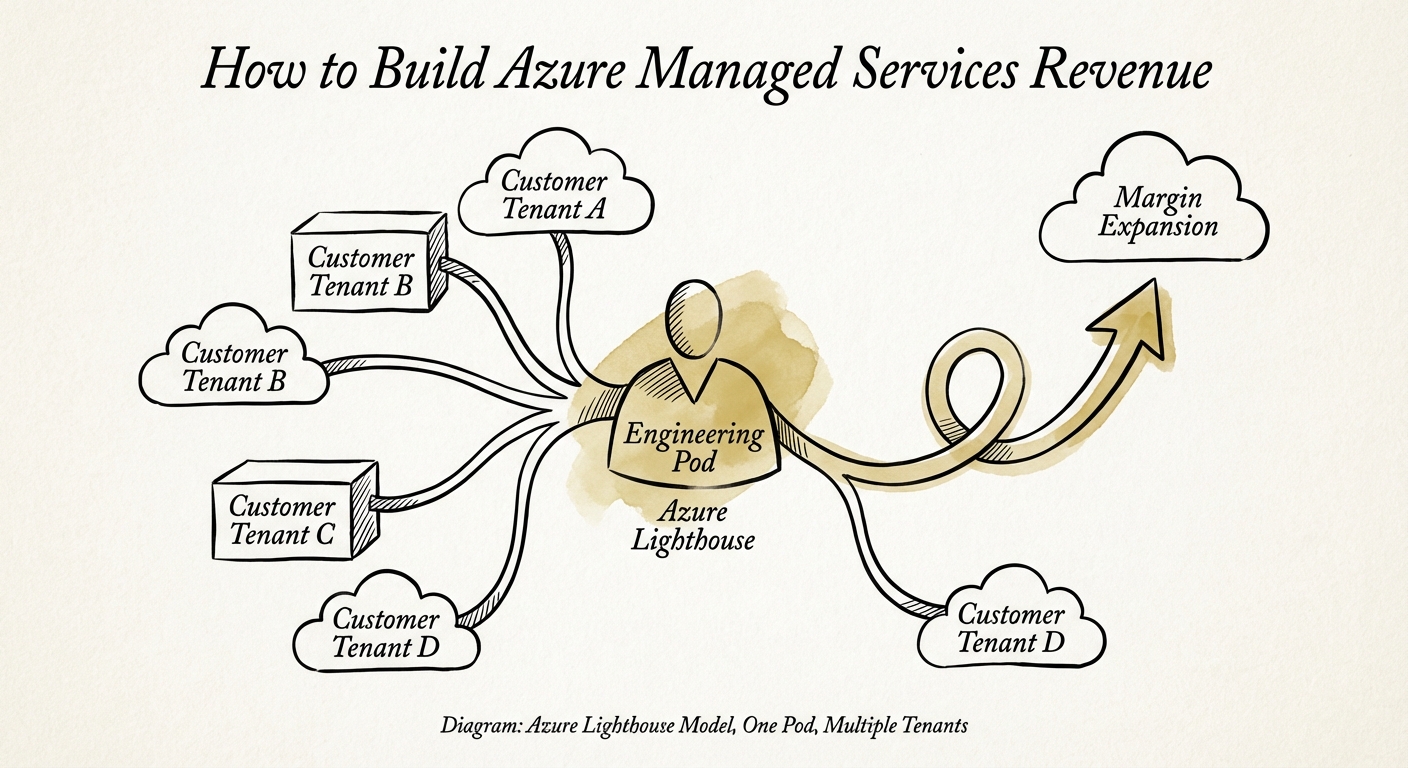

The leverage that makes the second sentence profitable is Azure Lighthouse. Delegated resource management lets one engineering pod operate across dozens of customer tenants from a single control plane — apply a Sentinel rule once, push it everywhere, monitor it centrally. That breaks the linear tie between revenue and headcount, and breaking that tie is precisely the EBITDA expansion a PE buyer is modeling when they justify a 10x.

What you can do Monday, in order

You do not pivot to an MSP model with a new pricing page. You do it by mining work you have already delivered, then refusing to sell support the old way. Three moves, sequenced.

1. Run the Day-2 audit on your last 20 migrations

Every Azure project you closed created a Day-2 problem the day you handed over the keys: who patches it, who watches the sign-in logs, who catches the orphaned $4K/month dev VM nobody decommissioned. Open your last 20 engagements this week and mark which ones you are actively managing. The unmanaged column is recurring revenue you already earned the right to and walked away from. That list is your first MSP pipeline — and the warmest one you will ever have.

2. Productize three SKUs, kill the custom support quote

The fastest way to look like a retainer instead of an MSP — and get valued like one — is to scope every support agreement bespoke. Build three fixed tiers and stop negotiating below the floor. Anchor each to Azure-native capabilities the client cannot easily DIY:

- Security & identity: Microsoft Sentinel monitoring, Defender posture, Entra conditional-access hardening.

- Cost & FinOps: a monthly right-sizing and reservation review — frame it honestly, because the savings frequently cover your fee, which makes the contract self-funding in the client's eyes.

- Compliance: Azure Policy and blueprint adherence mapped to the regimes your clients actually face (SOC 2, HIPAA).

3. Earn the Azure Expert MSP badge as your diligence proxy

If your roadmap runs toward a sale, the Azure Expert MSP designation is worth the pain. It demands an independent third-party audit and a meaningful threshold of Azure Consumed Revenue, which is exactly why it functions as shorthand for operational maturity in a diligence room — it is hard to fake, so a buyer treats it as evidence your delivery is repeatable rather than founder-dependent.

The mindset shift underneath all three: stop celebrating the $500K migration as the trophy. Celebrate the $10K/month governance contract you attach to it. The migration pays this quarter's bills. The contract — recurring, leveraged through Lighthouse, defensible in an audit — is the thing that actually gets priced when you sell.