The practical answer

- Short answer

- Atlassian resale margins are gone and migrations are drying up. Here's how partners build recurring managed-services revenue around Cloud governance, JSM, and Confluence sprawl.

- Best fit

- Industry: IT Services. Function: Revenue Operations

- Operating path

- Revenue Architecture → Commercial Performance → Office of the CFO

- Key metric

- 45% Target Attach Rate for MSP contracts on new Atlassian implementations.

The renewal that used to be a paycheck is now a commodity

Picture the Atlassian practice you could build in 2018. A new logo migrates from Server to Data Center, you bill for the project, you take a cut on the license renewal every year, and a Jira admin clears a ticket queue at an hourly rate. Predictable. Comfortable. And, in 2026, mostly gone.

Two things broke that model at once. Atlassian killed Server, and the 2025 Data Center price increases pushed the holdouts toward Cloud — which means the migration wave that funded years of growth is now tapering into a long tail of optimization work. At the same time, Cloud resale margins are a fraction of what license arbitrage used to deliver. If a meaningful slice of your revenue is still resale points plus one-off migration SOWs, you are selling a depreciating asset, and any buyer doing diligence will price it that way. (See GLiNTECH's breakdown of the Data Center pricing changes and the Cloud shift.)

Here is the gap that should keep you up at night. A reseller-and-projects shop changes hands somewhere around 0.8x to 1.2x revenue, because the buyer sees a book of renewals that could walk the day Atlassian changes its program terms. A genuine Atlassian managed-services practice — contracted, recurring, expanding — trades at a multiple several times higher, because the buyer is purchasing an annuity with room to grow inside each account. Same logos, same products, radically different valuation, and the only variable is whether the revenue recurs and expands without a new statement of work. We unpack that spread in Managed Services vs. Professional Services Valuation.

Anyone can renew an Atlassian license. The partner who governs the Cloud tenant when JSM bleeds into HR, Legal, and Finance is the one nobody dares to fire.

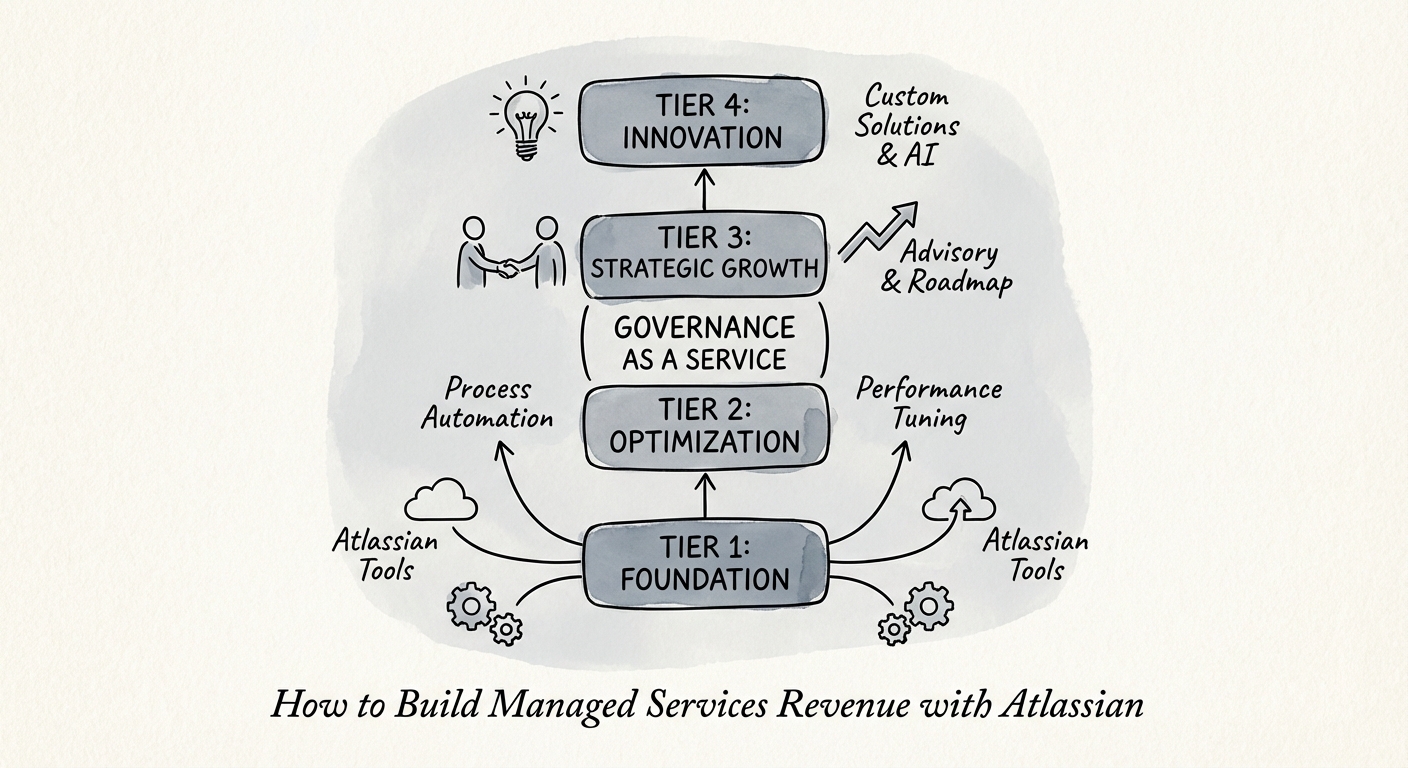

Stop selling "support." Sell the thing that's actually broken: sprawl

The reflex when an Atlassian partner first tries to build recurring revenue is to package "support" — a bucket of hours, a faster SLA, a named admin. The problem is that support is a cost line. It signals that something is broken, and in a Cloud-first world, the platform itself breaks far less often than it did on-prem. So you end up defending a contract against a CFO who can't see what they're paying for.

What actually breaks in Cloud is governance. The moment a company puts Jira Service Management and Confluence in front of "business teams" — and Atlassian is pushing hard in exactly that direction — the tool stops being an engineering utility and starts touching HR onboarding, legal intake, and finance approvals. Projects multiply. Permission schemes drift. Marketplace apps stack up. Nobody owns the whole tenant. SoftComply's argument that solution partners must pivot to business users lands here: the growth isn't in more developer seats, it's in the non-technical departments now living inside the platform.

That reframes what you sell. Instead of a block of hours, structure recurring tiers around governance outcomes:

- Platform health — the insurance policy. Automated user lifecycle (joiners/movers/leavers), license right-sizing so they stop paying for shelfware, and security-posture monitoring across the tenant. Low labor, high margin, and it quietly pays for itself by killing wasted seats.

- Business enablement — the expansion engine. Quarterly workflow audits for the non-engineering teams, turning a Jira Software client into a JSM-for-HR and Confluence-for-Legal account. This is where you grow inside the logo; see our vertical vs. horizontal expansion framework.

- Strategic governance — the CIO partner. A dedicated virtual admin, an architecture review cadence, and compliance readiness (SOC 2 / ISO) for the now-business-critical tenant.

The point of the ladder isn't tier names. It's that you've moved the budget line from "IT support OpEx" — the first thing cut in a downturn — to "the team that keeps a system every department depends on from falling over." That contract is much harder to sign away.

The one number that tells you whether you have an MSP or a help desk

Track attach rate: the share of your implementation and migration customers who convert into a recurring managed-services contract. It's the cleanest read on whether your motion is actually working. The strong Atlassian practices are landing somewhere near a 45% attach. If you're stuck under 20%, the diagnosis is almost always the same — you're pitching the managed-services contract after the project ships, when the budget is spent and the champion has moved on.

Fix it by selling Day 2 before Day 1. Bake "Day 2 operations" into the original SOW instead of treating it as an upsell. Say a 120-person company is migrating to Cloud: offer to trim the implementation fee modestly in exchange for a 24-month managed commitment that starts at go-live. You trade a little project margin for a recurring revenue bridge — and that bridge is precisely what a buyer pays a premium multiple for, because it converts a project shop into a subscription business on paper.

Then watch net revenue retention, because that's the difference between the two valuations from the top of this piece. Atlassian reports NRR well above 100% with its larger customers (the FY26 shareholder letter shows roughly 147% for that cohort) — they grow inside accounts by expanding into new teams, and your practice should ride the same wave by pushing JSM into HR, Confluence into Legal, automation into Finance. Flat NRR means you're a support desk holding a fixed-scope contract. Growing NRR means you're embedded and expanding, and that's the practice that commands the higher multiple. When Atlassian's own price increases hit, protect that retention with our value communication framework so a renewal conversation never turns into a re-shopping conversation.