The practical answer

- Short answer

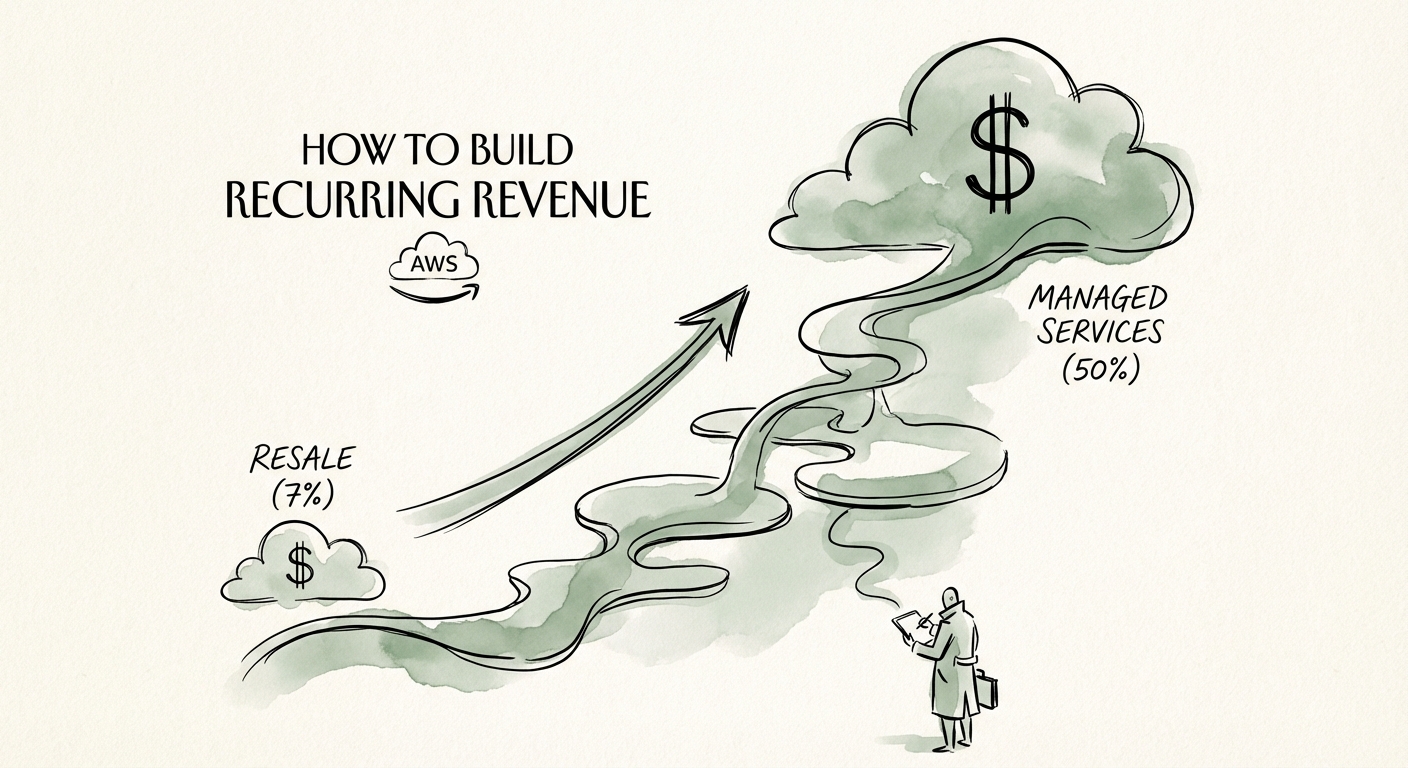

- The AWS resale arbitrage is dead. Discover the 2026 playbook for pivoting from low-margin resale to high-margin Managed Services (MSP) and unlocking a 10x EBITDA exit.

- Best fit

- Industry: Cloud Computing / IT Services. Function: Revenue Operations

- Operating path

- Revenue Architecture → Commercial Performance → Office of the CFO

- Key metric

- 12x EBITDA multiple for recurring revenue MSPs vs 1.5x for resale-focused partners.

The June 2025 Wake-Up Call: Why Resale Is No Longer a Business Model

For the last decade, thousands of AWS partners built "businesses" on a single, fragile premise: Arbitrage.

You bought Reserved Instances (RIs) or Savings Plans at a discount on your master payer account, sold the compute to your customers at on-demand rates, and pocketed the difference. It wasn't value creation; it was financial engineering. And as of June 2025, AWS effectively killed it.

The new policy blocking RI discount sharing across unrelated accounts didn't just change the rules; it vaporized the profit margins of resale-only MSPs overnight. If your EBITDA relied on keeping the spread between wholesale and retail, you no longer have a defensible business. You have a billing administration function.

This is the harsh reality for founders: you hit $20M in top-line revenue, but 80% of it is low-margin resale pass-through. Your "Gross Revenue" looks impressive on a slide, but your "Net Revenue" is thin, and your valuation is stuck at 1.0x - 1.5x revenue. Private Equity buyers aren't fooled by pass-through revenue. They strip it out during the Quality of Earnings (QofE) analysis.

The pivot required in 2026 is not just about survival; it's about valuation physics. Pure-play resellers trade like low-margin distributors. True Managed Service Providers (MSPs) with intellectual property (IP) and sticky recurring revenue trade at 10x - 12x EBITDA. To bridge that gap, you must stop selling access to the cloud and start selling outcomes in the cloud.

If your EBITDA relied on keeping the spread between wholesale and retail, you no longer have a defensible business. You have a billing administration function.

The 3-Layer MSP Stack: Moving Beyond "Keeping the Lights On"

To build genuine Recurring Revenue (ARR) that commands a premium multiple, you must productize your services. The days of "Time & Materials" support contracts are over. Modern MSPs package their expertise into three distinct layers.

Layer 1: CloudOps (The Utility Layer)

This is the baseline. Patching, monitoring, backups, and 24/7 incident response. In 2026, this is a commodity. If this is all you offer, you are in a race to the bottom on price. However, it is the ticket to play. You automate this using Infrastructure as Code (IaC) to keep your gross margins above 50%.

Layer 2: FinOps (The New Arbitrage)

Since you can no longer arbitrage the billing secretly, you must do it transparently. You act as the client's CFO for Cloud. You charge a percentage of savings found or a flat monthly fee to manage their spend. With AI driving cloud bills through the roof, FinOps is no longer optional. It is the primary retention hook. You aren't just sending a bill; you are justifying it.

Layer 3: SecOps & Compliance (The Premium)

This is where the 12x multiple lives. Integrating continuous compliance monitoring (SOC 2, HIPAA) into your MSP offering makes you "un-fireable." A client might switch vendors to save 5% on compute, but they will never switch vendors if it risks their SOC 2 status. This layer transforms your revenue from "maintenance" to "insurance."

According to Canalys data, partners who build this full-stack approach realize a $6.40 multiplier for every $1 of AWS compute sold. That is the difference between a reseller and a strategic partner.

The Unit Economics of the Pivot: Surviving the Valley of Death

Transitioning from project-based revenue or resale arbitrage to a true MSP model creates a temporary cash flow trough—the "Valley of Death." Here is the math you need to survive it.

1. Gross Margin Targets

Your target Gross Margin for Managed Services must be 45% - 55%. If you are below 40%, you are over-servicing or under-automating. This is a common trap for firms coming from a "white glove" consulting background. You cannot fix every server manually. You need a library of scripts and a bench utilization strategy that leverages junior talent for Level 1 tickets while your seniors build automation.

2. The Churn Metric

In the resale world, churn is low because switching billing is annoying. In the MSP world, you have to re-earn the business every month. Your Net Revenue Retention (NRR) is the single most important metric for your exit. PE firms look for 105%+ NRR. This means your upsells (adding security modules, new workloads) must outpace your churn. If your NRR is 90%, your business is a leaking bucket, and your valuation will be penalized accordingly.

3. The "Rule of 40" Reality Check

Don't get distracted by the Rule of 40 if you are under $10M ARR. Focus on Gross Profit Growth. A service business with 50% growth and 0% EBITDA is investable. A service business with 10% growth and 10% EBITDA is the walking dead. You need to invest aggressively in your "Service Product Management"—the team that builds the reusable IP that makes your service scalable.

The path is clear. The June 2025 policy change was the asteroid that killed the dinosaurs. You can either be a fossil or evolve into a high-margin, recurring revenue machine.