The practical answer

- Short answer

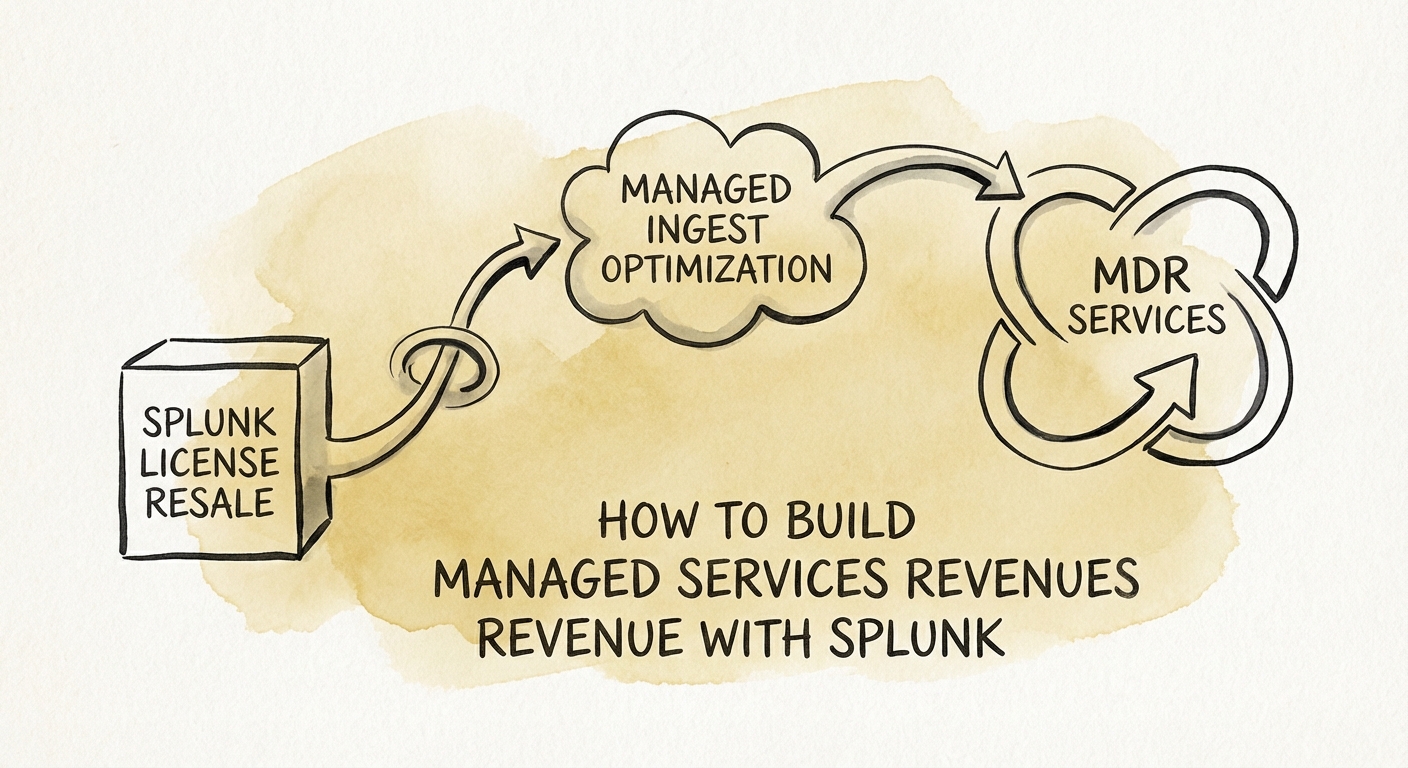

- Stop reselling Splunk licenses and start selling outcomes. Learn how to pivot from a 5x EBITDA VAR to a 14x EBITDA MSSP by building a Managed Detection and Response (MDR) practice.

- Best fit

- Industry: Cybersecurity / Data Analytics. Function: Revenue Operations

- Operating path

- Revenue Architecture → Commercial Performance → Office of the CFO

- Key metric

- 14x EBITDA multiple for specialized MSSPs, compared to 5x for traditional Splunk resellers.

The Reseller Trap: Why 'Ingest' is Killing Your Margins

For the last decade, the Splunk partner ecosystem operated on a simple, lucrative equation: sell the license, bill for the implementation, and renew the contract. But the ground has shifted beneath your feet. With Splunk’s acquisition by Cisco and the maturing of the log analytics market, the “resell and install” model is no longer a viable path to a premium exit.

The core problem is the “Ingest Trap.” Splunk Enterprise pricing often hovers around $1,800 to $2,500 per GB/day annually for smaller deployments. As your customers scale, their data volume explodes, but their budget does not. This creates an adversarial relationship where you, the partner, are the bearer of bad news every renewal cycle. Your “growth” is tied to their pain.

From a valuation perspective, this model is high-risk. Private equity buyers view Value-Added Resellers (VARs) as low-margin, high-risk commodities, typically trading at 4x to 6x EBITDA. Your revenue is lumpy, dependent on vendor renewal cycles, and prone to “optimization churn,” where clients rip out Splunk for cheaper open-source alternatives like ELK or Grafana simply to survive the bill.

If you aren't managing the value of the data, you are just a vendor passing through the bill. The partners winning today are the ones who use services to lower the license cost, funding their own margins in the process.

The MSP Pivot: From 'Admin for Hire' to 'Cost Governance'

To break the 5x valuation ceiling and push toward the 12x-14x multiples commanded by Managed Security Service Providers (MSSPs), you must decouple your revenue from the license bill. The most effective wedge for a Splunk practice today is not “more data,” but “better data economics.”

1. Offer 'Ingest Optimization' as a Managed Service

Instead of charging for hours to install forwarders, sell a recurring “Splunk Cost Governance” service. Your team continuously tunes data pipelines, filtering noise at the source and routing low-value logs to cheaper storage tiers (like AWS S3 or Splunk SmartStore) while keeping high-value security events in hot storage.

The Math: If you save a client $50,000 in annual ingest license costs through optimization, you can capture $25,000 of that as high-margin managed services revenue. You haven't increased their total spend; you’ve just shifted it from a low-margin vendor license to your high-margin service.

2. Build the SOC-as-a-Service Layer

The “Admin for Hire” model—where you patch servers and manage users—is a commodity race to the bottom. The premium tier is Managed Detection and Response (MDR). By layering a 24/7 Security Operations Center (SOC) on top of the customer’s Splunk instance, you transform from a tool maintainer to a risk mitigator.

With Cisco’s integration of XDR into the Splunk ecosystem, partners who can deliver outcomes (e.g., “15-minute mean-time-to-detection”) rather than outputs (e.g., “we patched the indexer”) are seeing gross margins jump from 15% (resell) to 45-60% (managed services).

The Exit Math: Why MSSPs Trade at 14x

The transition from project-based Splunk work to Managed Services is not just an operational upgrade; it is a valuation multiplier. In the current M&A climate, “pure-play” professional services firms are struggling to clear 8x EBITDA, while MSSPs with high recurring revenue retention (90%+) are seeing offers start at 12x.

To capture this premium, your revenue mix needs to shift. A target profile for a “Premium” Splunk Partner looks like this:

- Recurring Revenue: >50% of total revenue (vs. typical 20% for VARs).

- Gross Margins: >50% (driven by tech-enabled services, not just bodies).

- Concentration: No single customer >15% of revenue (hard to do with large ingest deals, easy to do with managed retainers).

The goal is to stop being the “Splunk Shop” that gets called when the indexer crashes, and become the “Security Partner” that owns the outcome. The former is a 1x revenue business; the latter is a strategic asset.