The practical answer

- Short answer

- Diagnostic guide for PE Operating Partners on NetSuite partner valuations. Why SDN IP commands 8x+ multiples while services lag at 1.5x, and how to bridge the gap.

- Best fit

- Industry: Enterprise Software / ERP. Function: M&A / Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 11.7x Median Revenue Multiple for SaaS/SDN companies with >120% Net Revenue Retention (2025 Benchmarks).

The Three-Tier Valuation Hierarchy

In the NetSuite ecosystem, not all revenue is created equal. I see Private Equity firms make the same mistake repeatedly: they acquire a “NetSuite Partner” expecting SaaS metrics, only to realize 90% of the P&L is low-margin professional services. If you are holding or buying a NetSuite asset, you must categorize the revenue streams brutally. The market in 2026 pays for intellectual property (IP), not hours.

1. The Alliance Partner (Pure Services)

These firms provide implementation, optimization, and rescue services. They do not sell software licenses (Oracle Direct does that) and they rarely own defensible IP. Their revenue is “recurring” only in the sense that clients keep buying hours.

- Valuation Metric: EBITDA Multiple

- Typical Multiple: 6x - 10x EBITDA (approx. 1.2x - 2.0x Revenue)

- Key Risk: High churn, key-person dependency, low gross margins (~40-50%).

2. The Solution Provider (Reseller + Services)

Solution Providers have a slightly better moat. They resell the NetSuite license (capturing a margin on the paper) and attach services. The license commission provides a stream of true recurring revenue, but Oracle’s margin squeeze in recent years has made this harder to bank on as a primary value driver.

- Valuation Metric: Blended (EBITDA + small ARR multiple)

- Typical Multiple: 2.0x - 3.0x Revenue

- Key Risk: Oracle channel conflict, license margin compression.

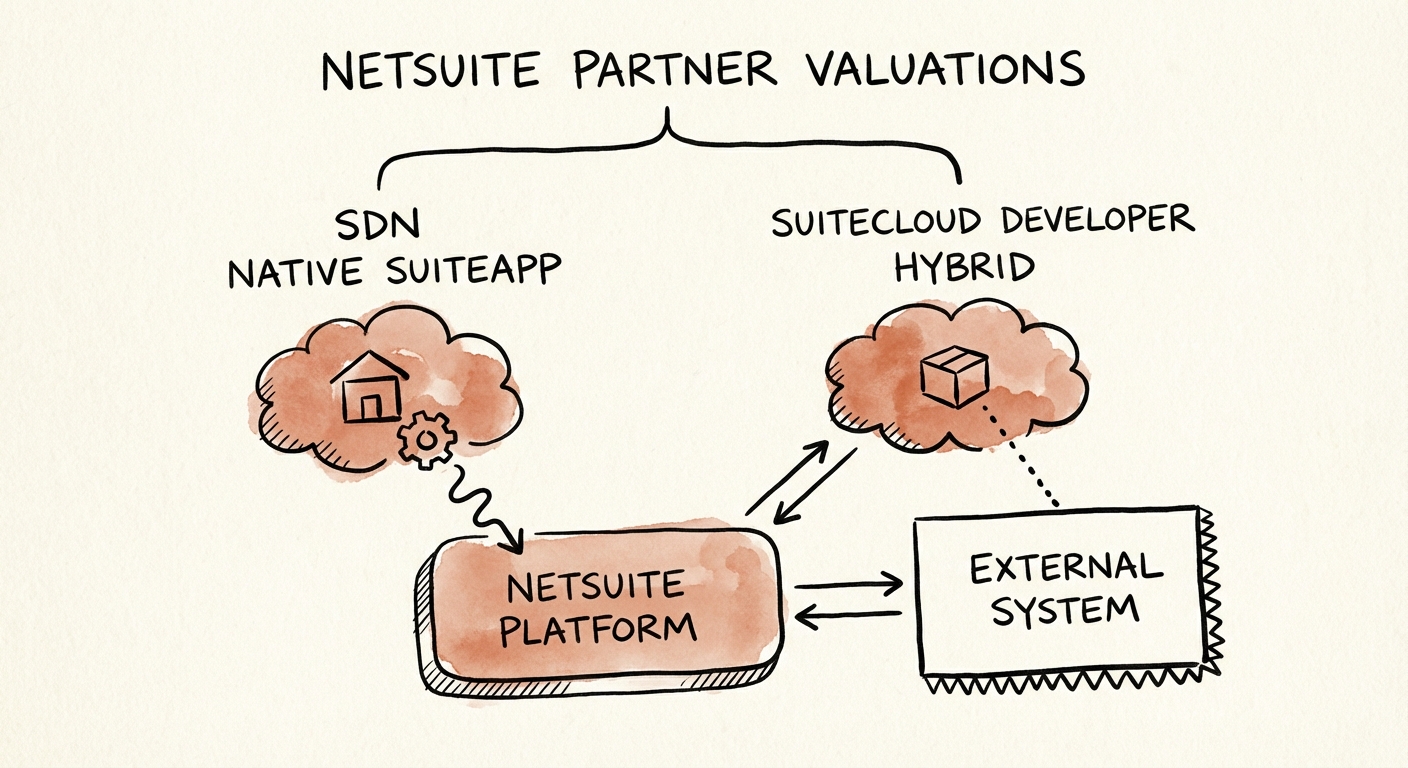

3. The SDN Partner (The “Gold Standard”)

Members of the SuiteCloud Developer Network (SDN) who build Built for NetSuite (BFN) certified SuiteApps. These are product companies. They solve a specific vertical problem (e.g., “Field Service for HVAC” or “Automated Intercompany Billing”). Once installed, they are incredibly sticky.

- Valuation Metric: Revenue Multiple (ARR)

- Typical Multiple: 6x - 12x Revenue (highly dependent on NRR)

- Key Advantage: 80%+ Gross Margins, NRR > 110%, low labor intensity.

The Diagnostic Warning: Many services firms claim to be SDN partners because they wrote a few custom scripts. Unless that code is packaged, managed, and sold as a SKU with a separate contract, it is not IP. It is tech-enabled services, and it should be valued at 2x, not 8x.

You don't get a SaaS multiple for 'recurring' admin hours. You get it for intellectual property that makes money while your engineers sleep. If you can't push an update to 500 customers with one click, you don't have a product—you have a project library.

The Technical Due Diligence: Vaporware vs. Defensible IP

When evaluating a “product-led” NetSuite partner, you cannot trust the marketing deck. You need to look at the code structure and the distribution model. I’ve audited “SuiteApps” that were nothing more than a collection of saved searches and a few lines of SuiteScript 1.0 glue code.

The “Wrapper” Test

Real SDN value comes from extending the platform, not just configuring it. Ask these three questions during technical diligence:

- Is the IP Native or Hybrid?

Native SuiteApps run entirely inside NetSuite. They are easier to sell but harder to defend (NetSuite might build the feature next release). Hybrid apps (external platform connected via REST/SuiteTalk) offer a stronger defensive moat but higher infrastructure costs. In 2026, Hybrid apps with AI capabilities are commanding the highest premiums. - Where is the Logic Hosted?

If the “IP” resides in unmanaged bundles customized for each client, you don’t have a product; you have a template library. True valuation value requires a Managed Bundle or SuiteApp distribution model where updates are pushed centrally to 500+ tenants simultaneously. - What is the “Upgrade Risk” Score?

NetSuite updates twice a year. If your partner’s IP breaks every time NetSuite upgrades (requiring manual fixes), your churn will skyrocket. Demand to see the “Release Preview” testing logs for the last four cycles.

The “Recurring Services” Trap

Be wary of revenue labeled “Managed Services.” In the NetSuite world, this is often a retainer for ad-hoc admin work. It is not SaaS. It has services margins (40%) and high churn. To get the SDN multiple, the revenue must be tied to the license of the IP, not the availability of a human.

The Pivot: From Service Shop to 8x Exit

If you are a PE Operating Partner stuck with a low-margin services firm, you have a specific play to execute over 18-24 months. You cannot simply “will” a higher valuation; you must engineer it.

1. Identify the “Repeater”

Analyze your last 50 implementations. What custom code did you write 30 times? That is your product. It might be a connector to a specific 3PL, a commission calculator for a niche industry, or a compliance module. Isolate it.

2. Productize the Code (The “Build”)

Move that code into a Managed Bundle. Get the Built for NetSuite (BFN) badge. This is non-negotiable. The BFN badge is social proof for the ecosystem and a quality stamp for acquirers. It proves the code follows Oracle’s security and architectural standards.

3. Bifurcate the P&L

This is where most fail. You must separate the “Product” financials from the “Services” financials. Create two distinct business units.

Unit A (Services): Measures utilization, billable rates, project margin.

Unit B (IP/SDN): Measures CAC, ARR, NRR, Churn.

When you go to market, you sell a “Sum of Parts.” You might get 1.5x on the $10M of services revenue, but you could get 8x on the $3M of newly minted IP revenue. That split alone can add $20M to your Enterprise Value.

4. The Distribution Moat

Finally, stop selling the IP only to your own implementation clients. The hallmark of a true SDN partner is that other Solution Providers sell your product. If you can demonstrate a channel strategy where competitors are reselling your tool, you have validated the standalone value of the asset.