The practical answer

- Short answer

- Private equity is rolling up Adobe partners. Learn why AEP specialization commands 14x multiples while generalist agencies stall at 6x.

- Best fit

- Industry: Digital Experience / MarTech. Function: M&A / Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 40% Projected growth in Adobe Experience Platform adoption, driving the demand for specialized technical partners.

The March 2026 Catalyst: Convergence or Death

For the last decade, the Adobe partner ecosystem was neatly divided: creative agencies designed the assets, and systems integrators (SIs) wired the plumbing. That division of labor is officially dead. With the launch of the unified Adobe Digital Experience Partner Program on March 1, 2026, the market is forcing a convergence that is driving a massive wave of consolidation.

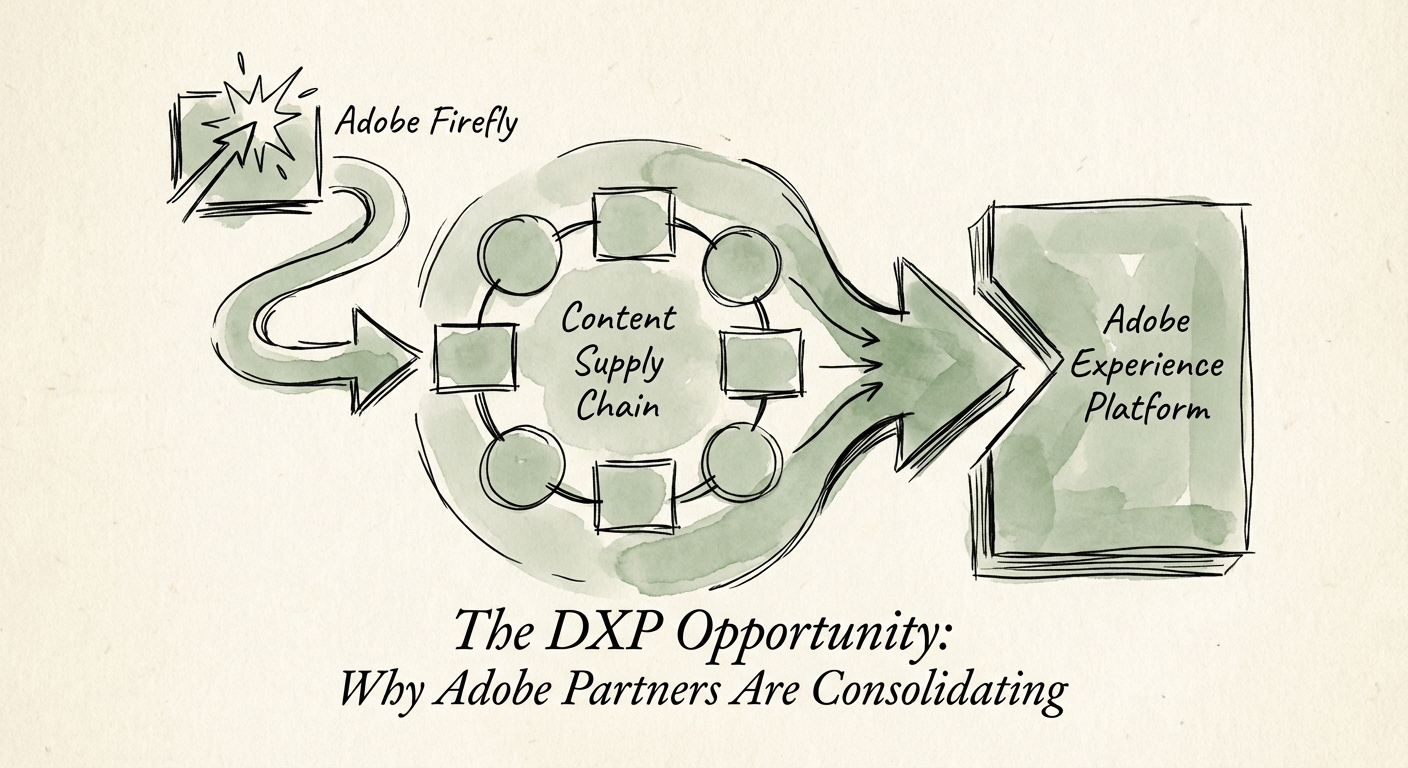

The catalyst isn't just a program change; it's a fundamental shift in how enterprise value is created. The old model of billing hourly for Adobe Experience Manager (AEM) implementations is now a commodity service trading at 6x EBITDA. The new model—building the "Content Supply Chain"—is where the alpha lives. This involves linking Generative AI (Firefly) to workflow (Workfront) to experience delivery (AEP), creating a closed loop of data and content.

Private equity sponsors have noticed. They are no longer buying standalone creative shops or pure-play Magento dev shops. They are rolling up specialized assets to create "Full Stack" solution partners capable of executing the entire content lifecycle. If your firm is still positioning itself as an "AEM Shop" or a "Creative Agency," you are essentially invisible to the buyers paying premium multiples.

The era of the 'AEM Shop' is over. Buyers today aren't paying for CMS implementation; they are paying for the data infrastructure that powers the entire customer journey.

The Valuation Gap: Why 6x and 14x Look the Same on the Surface

In 2026, two Adobe Gold Partners can generate $20M in revenue and $4M in EBITDA, yet one will trade for $24M and the other for $56M. The difference lies in the composition of revenue and the technical depth of the practice.

The "Generalist Discount" applies to firms that rely on:

- Creative Services Retainers: High churn, low defensibility, and vulnerable to in-housing or AI displacement.

- Standard AEM Implementations: "Lift and shift" projects that compete on price against global SIs.

- Reselling Licenses: Low-margin pass-through revenue that inflates top-line but adds zero enterprise value.

Conversely, the "Specialist Premium" (trading at 12x-14x) is awarded to firms that have mastered the Adobe Experience Platform (AEP). These firms aren't just building websites; they are architecting Real-Time CDP infrastructures that act as the central nervous system for their clients. Buyers are paying for the intellectual property and specialized talent required to implement Adobe Journey Optimizer (AJO) and Customer Journey Analytics (CJA)—skills that are in critically short supply.

The PE Playbook: Rolling Up the Content Supply Chain

The current consolidation wave is driven by a simple math problem: there aren't enough organic growth opportunities to satisfy the demand for DXP transformation. PE firms are responding by executing "Buy and Build" strategies to manufacture the scale and capability mix that Adobe's new program requires.

The playbook involves acquiring a "Platform" asset—usually a strong technical integrator with deep AEP chops—and then bolting on:

- Data & Analytics Boutiques: To capture the CJA/CDP opportunity.

- Workfront Specialists: To own the operational workflow layer.

- Commerce Agencies: To close the loop on transaction data.

However, this strategy is fraught with risk. Integrating a creative culture with an engineering culture is historically the fastest way to destroy value. Successful sponsors are avoiding the "Frankenstein" portfolio by enforcing a unified operating model and focusing on integrated offerings—like "GenAI for Commerce"—rather than just cross-selling disparate services. If you are a founder looking to exit, your ability to demonstrate how you fit into this wider Content Supply Chain is the single biggest determinant of your exit multiple.