The practical answer

- Short answer

- Analysis of 2026 Workday partner M&A trends. Why niche firms with Financials & AI expertise trade at 14x EBITDA while generalist HCM shops stall at 6x.

- Best fit

- Industry: Private Equity / Technology Services. Function: M&A / Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14x EBITDA multiple for Workday partners with 'Full Platform' (Fins + AI) capabilities.

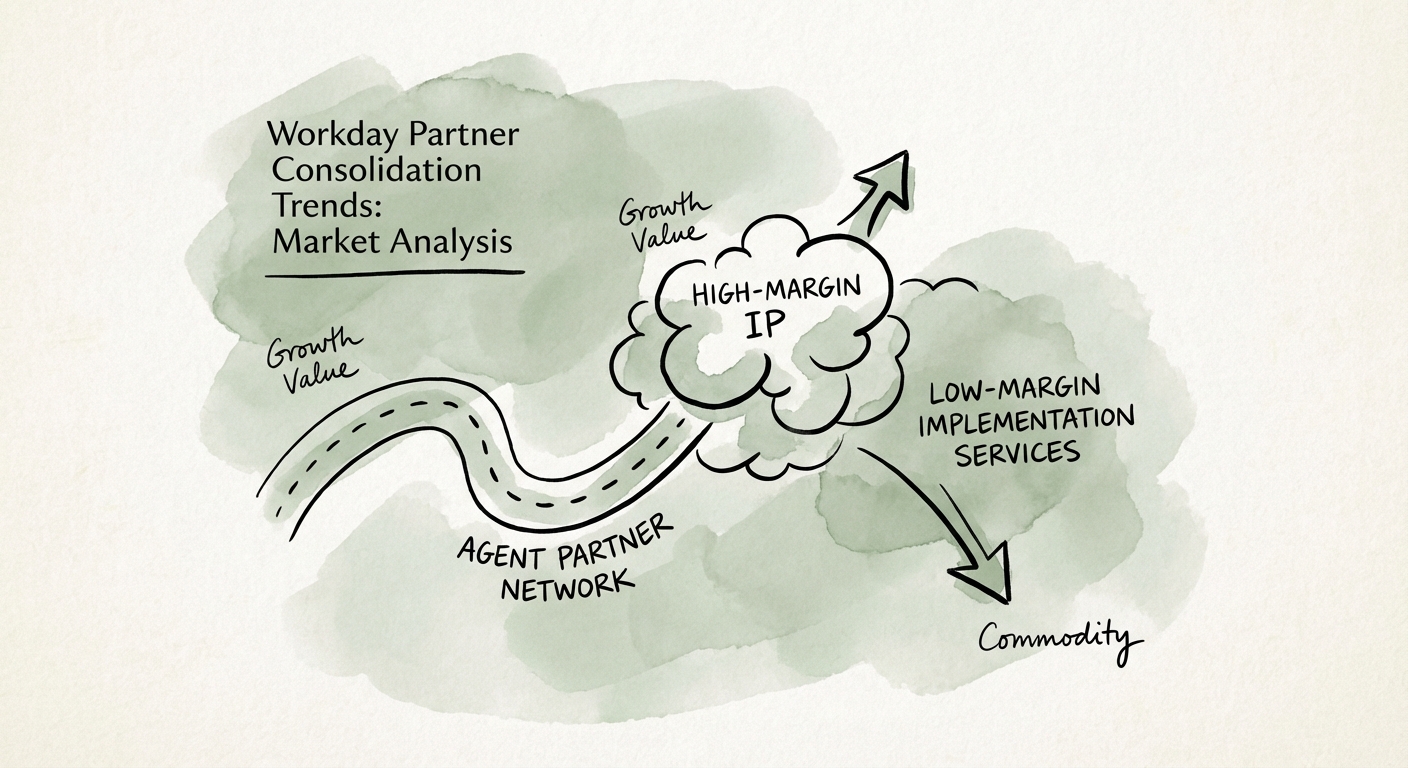

The Great Bifurcation: Platforms vs. Body Shops

For the last decade, the Workday ecosystem was a rising tide that lifted all boats. If you had a badge and a pulse, you could bill out functional consultants at $225/hour and trade for 8x-10x EBITDA. That era ended in late 2025.

We are now witnessing a violent bifurcation in the market. On one side, we have the "Platform" Partners—firms that have successfully crossed the chasm from HCM implementation to Strategic Transformation (Financials, Adaptive Planning, and the new Agent Partner Network). These assets are commanding premium multiples, often trading north of 14x EBITDA because they own the customer roadmap for the next five years.

On the other side are the "Body Shops." These are the generalist HCM firms that rely on staff augmentation and "lift and shift" deployments. Their valuations have collapsed to 5x-6x EBITDA. Why? because Workday's own certification barriers (the Velvet Rope) and the rise of AI-driven implementation accelerators have commoditized basic deployment. If your only value proposition is "we have certified bodies," you are no longer an asset; you are a commodity.

In 2026, you cannot multiple-arbitrage your way to a win in the Workday ecosystem. You either build a 'Platform' that owns the Office of the CFO, or you own a 'Body Shop' that bleeds margin until it dies.

The New Valuation Drivers: Financials, Agents, and IP

The delta between a 6x exit and a 14x exit is no longer determined by headcount growth; it is determined by Revenue Quality and Technical Density. Private Equity buyers have realized that the real stickiness in the Workday ecosystem isn't in HR—it's in the Office of the CFO.

1. The Financials (Fins) Premium

Partners with deep expertise in Workday Financial Management are trading at a 4-turn premium over HCM-only shops. The logic is simple: HR systems are sticky, but Financial systems are concrete. Once a partner owns the General Ledger and Adaptive Planning workflows, they are irremovable.

2. The "Agent" Multiplier

With Workday's launch of the Agent Partner Network in late 2025, the definition of "service" changed. High-value partners are now building proprietary AI agents that sit on top of Workday, driving outcomes rather than just billing hours. This shift from Services Revenue to IP-Enabled Revenue is the single biggest driver of multiple expansion in 2026. If you aren't building agents, you're just renting time.

Investors are also scrutinizing labor costs and margin erosion caused by the talent shortage. Firms that have solved this with IP (automating configurations) are winning; those fighting the war for talent with higher salaries are bleeding margin.

The PE Roll-Up Trap: Don't Buy a Frankenstein

I see a lot of Operating Partners trying to play the "Roll-Up Game" by acquiring three or four small, regional Workday partners to create a "Global Challenger." On paper, the arbitrage looks brilliant: Buy at 6x, integrate, sell at 14x. In reality, this strategy fails 60% of the time.

The failure point is almost always Integration Debt. Workday consultants are the prima donnas of the tech services world. They know their market value. When you mash together three different cultures, three different compensation models, and three different delivery methodologies, you don't get synergy—you get attrition. And in this ecosystem, when the talent leaves, the value leaves.

The Winning Play: Instead of rolling up generic capacity, focused investors are buying capabilities. They acquire a platform anchor (usually a mid-sized firm with strong Financials expertise) and bolt on technical niche players (specialists in Prism, Extend, or specific Industry Accelerators). They aren't buying volume; they are buying the ability to say "Yes" to the complex, high-margin projects that the Global SIs are too slow to handle and the body shops are too unskilled to touch.