The practical answer

- Short answer

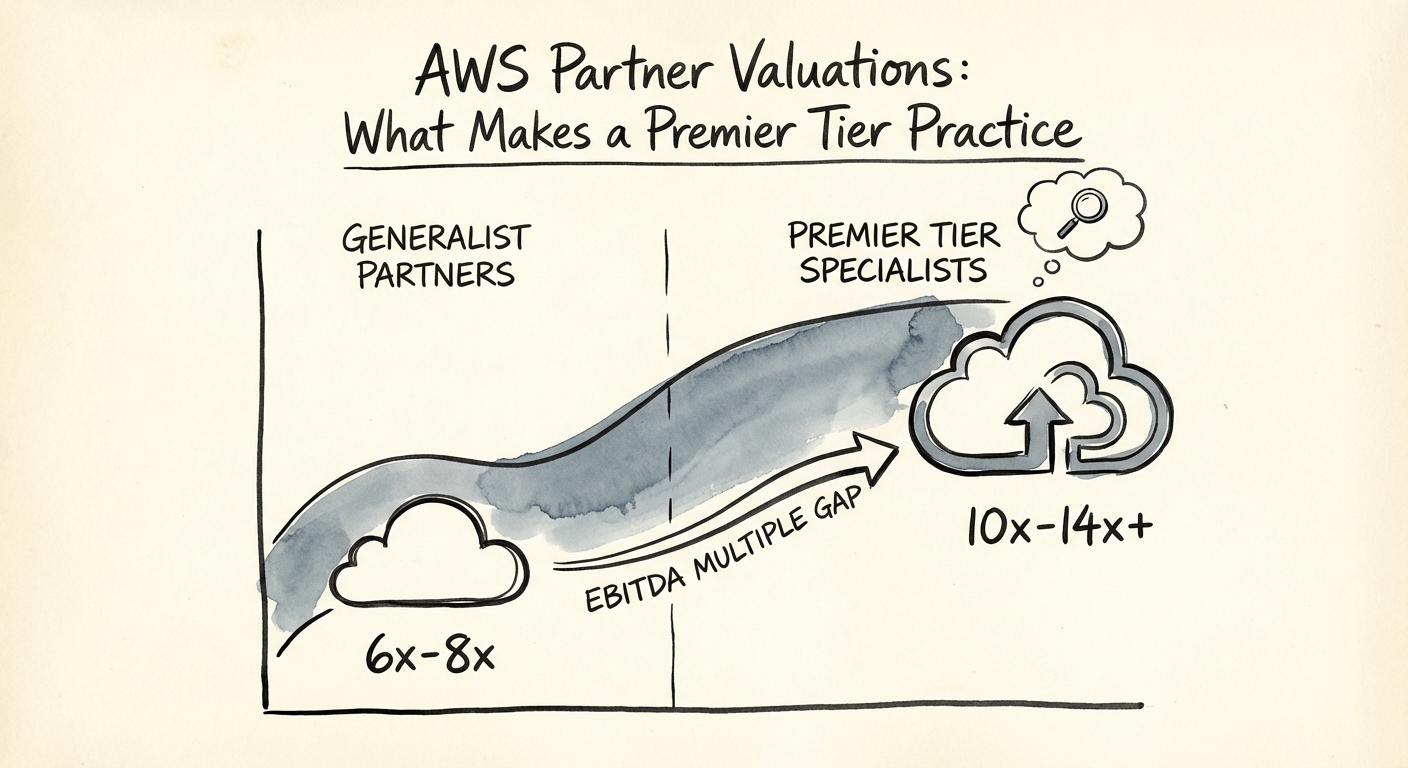

- AWS Premier specialists trade at 12–14x EBITDA; Advanced generalists stall at 6–8x. The certification density, MAP subsidy, and $7.13 math behind the gap.

- Best fit

- Industry: Cloud Consulting / IT Services. Function: M&A / Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- $7.13 Service revenue generated per $1 of AWS sold by 'Expert' partners (Omdia 2025).

The Tale of Two Partners: Why 'Advanced' is the New Average

In the 2026 M&A landscape, the AWS ecosystem has bifurcated. On one side, you have the "Generalist Advanced" partners—firms that achieved the badge through volume resell and basic lift-and-shift migrations. These firms are trading at 6x to 8x EBITDA. They are viewed as commodities, squeezed by rising labor costs and the commoditization of basic infrastructure management.

On the other side, you have the Premier Tier Specialists. These firms aren't just selling EC2 instances; they are engineering outcomes. They command valuations of 12x to 14x EBITDA. Why the massive spread?

The $7.13 Multiplier Effect

The core differentiator is the "Service Revenue Multiplier." According to the 2025 Omdia AWS Partner Ecosystem Multiplier study, highly specialized "Expert" partners generate $7.13 in services revenue for every $1 of AWS consumption they sell. Contrast this with "Focused" (smaller, generalist) partners who generate only $1.26. Private Equity buyers have woken up to this math. They aren't buying the resell margin (which is thin and shrinking); they are buying the attachment rate of high-margin professional and managed services.

The AWS badge on your website is either a marketing sticker or a license to print EBITDA. The difference isn't the logo; it's whether you're selling capacity or capability.

The MAP Moat: How Subsidy Drives Valuation

If your portfolio company is an AWS partner and they aren't leveraging the Migration Acceleration Program (MAP) for at least 40% of their pipeline, they are burning cash. MAP isn't just a discount program; it is a Customer Acquisition Cost (CAC) subsidy funded by Amazon.

Premier Tier partners unlock significantly higher funding tiers than Advanced partners. This allows them to effectively lower the price for the end customer by 25-50% while maintaining (or increasing) their own gross margins. In a competitive bid, the Premier partner uses Amazon's balance sheet to win the deal, while the Advanced partner has to erode their own EBITDA to compete.

The 'Fake Premier' Diagnostic

Be warned: I see "Fake Premier" firms in due diligence constantly. These are firms that bought the badge through aggressive resell tactics but lack the delivery DNA. The tell-tale sign? A low ratio of Pro/Specialty Certifications to Headcount. A true Premier shop runs at a certification density of >2.5x (avg certifications per engineer). If you see a firm with $50M revenue but a 0.8x certification density, you are looking at a low-margin staffing agency masquerading as a high-value consultancy. The valuation haircut on that realization is usually 30%.

Engineering the 14x Exit: The 2026 Playbook

To move a practice from the 8x bucket to the 14x bucket, you must pivot the revenue mix from "Capacity" to "Capability." In 2026, this specifically means Agentic AI and Data Modernization. The "Lift and Shift" era is over; the "Modernize and Intelligence" era is here.

Buyers are paying premiums for specific competencies:

- Data & Analytics: 12x-14x EBITDA

- Security (MSSP): 13x-15x EBITDA

- Agentic AI / Generative AI: Valuation undetermined (often revenue multiples), but highly accretive.

Your strategic roadmap for the next 18 months must be aggressive. Stop chasing generic "Advanced" badges. Focus on deep specialization. If you are a generalist, acquire a boutique Data/AI firm to layer that high-multiplier revenue onto your existing customer base. As noted in our analysis of IT Services M&A Trends, the market rewards depth, not breadth.

Don't just measure your EBITDA; measure your EBITDA Quality. Is it coming from a race-to-the-bottom hourly rate, or stickier, high-value managed services? For a deeper dive on why your metrics might be deceiving you, read about why the Rule of 40 is a lie for services firms.