The practical answer

- Short answer

- Palo Alto Networks partner valuations are bifurcating. Why Cortex XSIAM and Prisma Cloud specialists trade at 14x EBITDA while firewall resellers stall at 5x.

- Best fit

- Industry: Cybersecurity / Private Equity. Function: M&A / Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14x Average EBITDA multiple for PANW partners with >50% NGS (Prisma/Cortex) revenue mix.

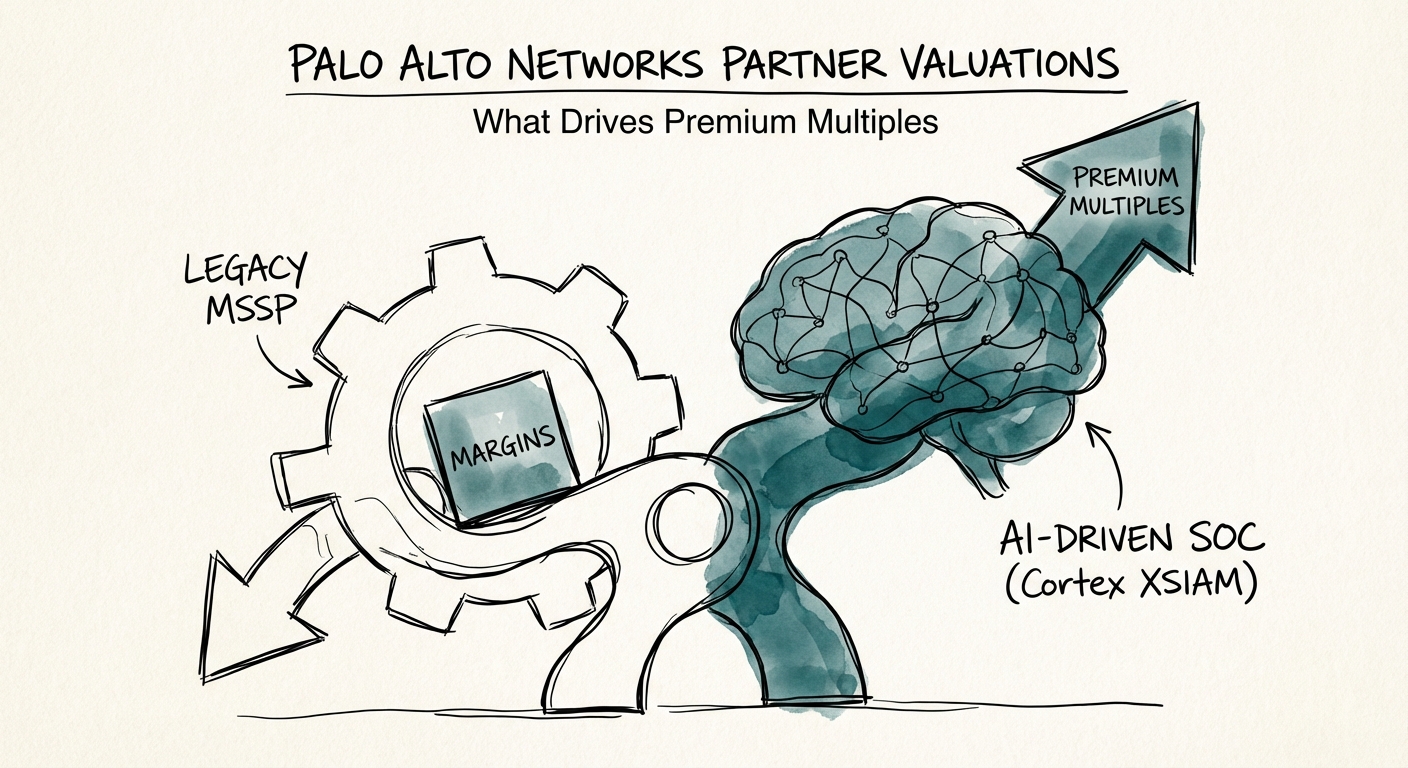

The Valuation Bifurcation: From 'Firewall Refresh' to 'Platformization'

For two decades, the valuation of a Palo Alto Networks partner was simple: volume drove tiering, and tiering drove discounts. If you could move enough hardware boxes (Strata) to hit Diamond status, you secured the margins necessary to trade at a healthy 7x-8x EBITDA. That era is over. The market has bifurcated into two distinct asset classes with wildly different exit profiles.

On one side are the Transaction-Centric Resellers (VARs). These firms still rely on hardware refresh cycles and standard firewall licensing. While they may generate significant top-line revenue, their valuation multiples have compressed to the 4x-6x range. Private equity buyers view this revenue as non-recurring and highly susceptible to direct-to-consumer shifts or cloud displacement.

On the other side are the Next-Gen Security (NGS) Specialists. These firms have pivoted their entire business model around Prisma (Cloud Security) and Cortex (SecOps). They don’t just resell licenses; they wrap them in proprietary Managed Detection and Response (MDR) services. According to 2025 market data, these firms are commanding premiums of 12x-15x EBITDA, with some cloud-native specialists seeing even higher strategic offers.

The 'Platformization' Premium

Palo Alto Networks' CEO Nikesh Arora has aggressively pushed a strategy of "Platformization"—consolidating point solutions into a unified stack. Partners who mirror this strategy are seeing a valuation multiplier. Buyers are no longer paying for access to customers; they are paying for stickiness. A partner managing a client’s entire SASE (Secure Access Service Edge) and SOC (Security Operations Center) architecture is infinitely harder to displace than one simply fulfilling a firewall renewal.

We are seeing a massive divergence in the market. The partner selling firewalls is trading at 5x. The partner selling 'SOC Transformation' with Cortex XSIAM is trading at 14x. It's the same vendor ecosystem, but two completely different business models.

The Three Pillars of a Premium Multiple

In our analysis of recent M&A activity within the cybersecurity channel, three specific variables correlate directly with double-digit EBITDA multiples. If you are preparing a Palo Alto Networks practice for exit, these are your valuation levers.

1. NGS Revenue Composition > 50%

The "Next-Gen Security" (NGS) metric is the primary filter for PE due diligence. Acquirers are discounting hardware revenue by as much as 50% in their internal models. Conversely, revenue derived from Prisma SASE and Prisma Cloud is treated as high-quality, often recurring revenue (ARR). A partner with greater than 50% of their gross profit coming from NGS sources commands a "Cloud Security" premium, aligning them with specialized hyperscaler partners rather than traditional IT VARs.

2. The Cortex XSIAM 'AI' Multiplier

The most significant recent driver of valuation expansion is the adoption of Cortex XSIAM (Extended Security Intelligence & Automation Management). Partners who have successfully built a managed service practice around XSIAM are effectively selling "AI-Driven SOC Transformation." This is not just a marketing buzzword; it represents a fundamental shift in unit economics. Traditional MSSPs struggle with labor scaling—adding more analysts as they add customers. XSIAM-enabled partners leverage automation to break this linear relationship, resulting in gross margins that can exceed 60%, compared to the 35-40% industry average for legacy MSSPs.

3. The 'Unit 42' Alignment

Service attachment is no longer about racking and stacking appliances. Premium valuations are reserved for partners who can deliver high-end incident response (IR) and threat hunting that aligns with Palo Alto’s Unit 42 methodology. Partners who hold the XMDR specialization and can demonstrate a track record of co-delivery with Unit 42 are viewed as strategic assets, capable of capturing the high-margin professional services tail that follows every major breach.

The 'Fake MSSP' Trap in Due Diligence

For Private Equity buyers, the risk in acquiring Palo Alto Networks partners lies in misidentifying the revenue quality. We frequently encounter firms positioning themselves as "Managed Security" players who are, in reality, simply amortizing license costs over a 3-year term. This is financial engineering, not a managed service.

A true MSSP valuation requires intellectual property wrapped around the vendor technology. In the data room, look for the "Service Attach Rate" on Cortex deals. If the partner is selling Cortex XDR licenses but the customer is monitoring the alerts themselves (or ignoring them), that is a churn risk, not a recurring revenue stream. Similar to the SecOps trends we see in the ServiceNow ecosystem, the value lies in the workflow and the response, not the license transaction.

Red Flag: The 'Classic' Firewall Dependency

Finally, audit the customer base for Strata dependency. While the firewall business is stable, it is not a growth engine. A partner with 80% of their base on on-premise firewalls without a clear roadmap to SASE is sitting on a latent risk of technical debt. Premium multiples are awarded to partners who are actively migrating their own base to Prisma Access, effectively cannibalizing their own hardware revenue to secure long-term, high-margin software ARR.