The practical answer

- Short answer

- New data reveals a massive valuation gap in the Palo Alto Networks partner ecosystem. Why Prisma Cloud specialists trade at 14x while firewall generalists stall at 6x.

- Best fit

- Industry: Cybersecurity. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14.3x Average revenue multiple for high-growth (>20%) cloud security companies in 2025.

The Great Bifurcation: Strata vs. Prisma

In the private equity ecosystem, the "Palo Alto Networks" brand used to be a singular stamp of quality. If a portfolio company was a Platinum Partner, it commanded a premium. That era is over. In 2026, the market has rigorously bifurcated the ecosystem into two distinct asset classes with wildly different valuation profiles: the Hardware Generalist and the Cloud Specialist.

According to Q4 2025 data from Solganick & Co and Finro Financial Consulting, the valuation gap between these two profiles has widened to a chasm. Cybersecurity vendors and service providers with low growth (<10%)—typically those tethered to hardware refresh cycles—are trading at a median of 4.7x revenue. In contrast, high-growth cloud security specialists (>20%) are commanding multiples of 14.3x revenue.

For a PE sponsor, this means two partners with identical top-line revenue can have Enterprise Values that differ by tens of millions of dollars. The driver is the revenue mix. The Strata (firewall) business is becoming a commodity game of low-margin resale and "break-fix" support. The Prisma Cloud (CNAPP) business is a high-margin, recurring revenue engine embedded deep within the customer's CI/CD pipeline. One is a vendor relationship; the other is a strategic dependency.

The gap between a 6x and a 14x exit isn't the logo on your website; it's the revenue mix in your P&L. Hardware is a commodity. Cloud security is a currency.

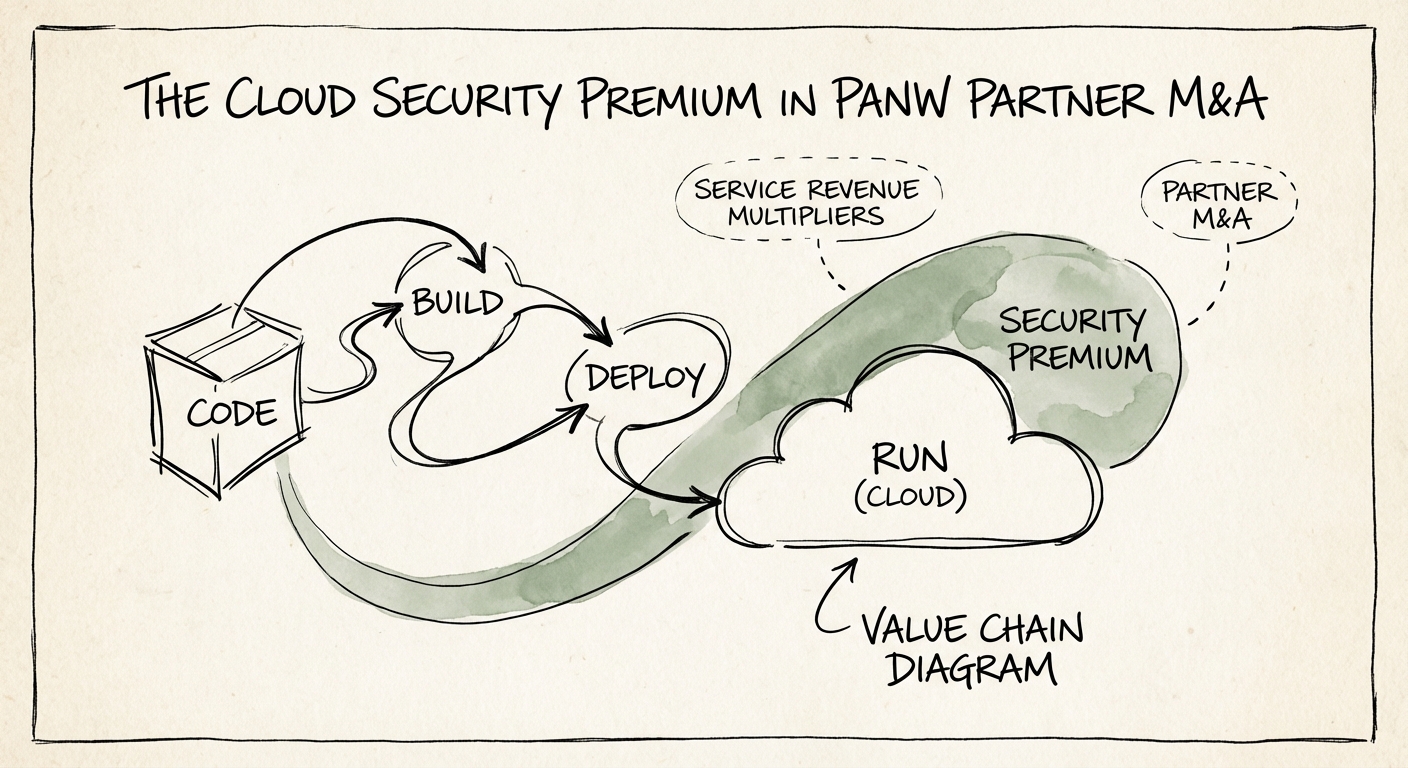

The Unit Economics of "Code-to-Cloud" Stickiness

Why are acquirers paying a 200% premium for Prisma Cloud revenue? It comes down to the unit economics of retention and expansion. Traditional firewall managed services are susceptible to "rip and replace" cycles every 3-5 years. If a competitor undercuts your hardware pricing, the perimeter can move.

Prisma Cloud, however, operates on a "Code-to-Cloud" continuum. It is not just securing a server; it is integrated into the client's engineering workflow, from infrastructure-as-code (IaC) scanning to runtime protection. Once a partner installs Prisma, they aren't just the "security guy"; they become the enabler of the client's DevOps velocity. This results in significantly higher Net Revenue Retention (NRR).

The $6.50 Multiplier

Palo Alto Networks' own data supports this valuation shift. IDC estimates that for every $1 of Palo Alto Networks licensing revenue, partners generate $6.50 in associated services—but this multiplier is not evenly distributed. Hardware resale drags this average down. The real margin expansion happens in the "Day 2" services associated with Prisma and Cortex:

- Cloud Security Posture Management (CSPM): Recurring advisory fees.

- DevSecOps Implementation: High-bill-rate consulting.

- SOC Automation (Cortex XSIAM): Managed Detection and Response (MDR) contracts.

Partners who successfully pivot to these services don't just see revenue growth; they see margin growth, breaking the "linear scaling" trap of traditional MSPs.

The Valuation Bridge: From Reseller to Platform Player

For PE Operating Partners—the PE Operating Partner managing a mid-market cyber firm—the mandate is clear. You cannot exit a generalist reseller in 2026 and expect a premium multiple. You must engineer a mix-shift pivot before you go to market.

This requires a disciplined audit of your revenue quality. If 60% of your EBITDA is derived from hardware resale and renewal churn, your MSP valuation is capped at 6-8x. To unlock the security specialization premium, you need to demonstrate "Prisma Revenue Quality":

- Consumption vs. CAPEX: Shift customers from prepaid hardware to consumption-based cloud security credits.

- IP-Led Services: Distinct from generalist support, offering proprietary policies or automation on top of the Prisma platform.

- Next-Gen Security (NGS) Alignment: Align your growth with PANW's NGS metrics. With PANW's NGS ARR growing at 37% YoY, your practice should be matching that pace. If you are growing at 10% while the NGS ecosystem grows at 37%, you are losing market share.

The "Cloud Security Premium" is real, but it is not given to those who merely carry the badge. It is reserved for partners who have fundamentally transformed their business model from protecting the perimeter to securing the pipeline.