The practical answer

- Short answer

- Why Palo Alto Networks partners specializing in Cortex and Prisma trade at 14x EBITDA while firewall resellers stall at 6x. A field diagnostic for PE deal teams.

- Best fit

- Industry: Cybersecurity Services. Function: Corporate Development

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14x EBITDA Valuation multiple for PANW partners with >50% revenue from Cortex/Prisma Managed Services.

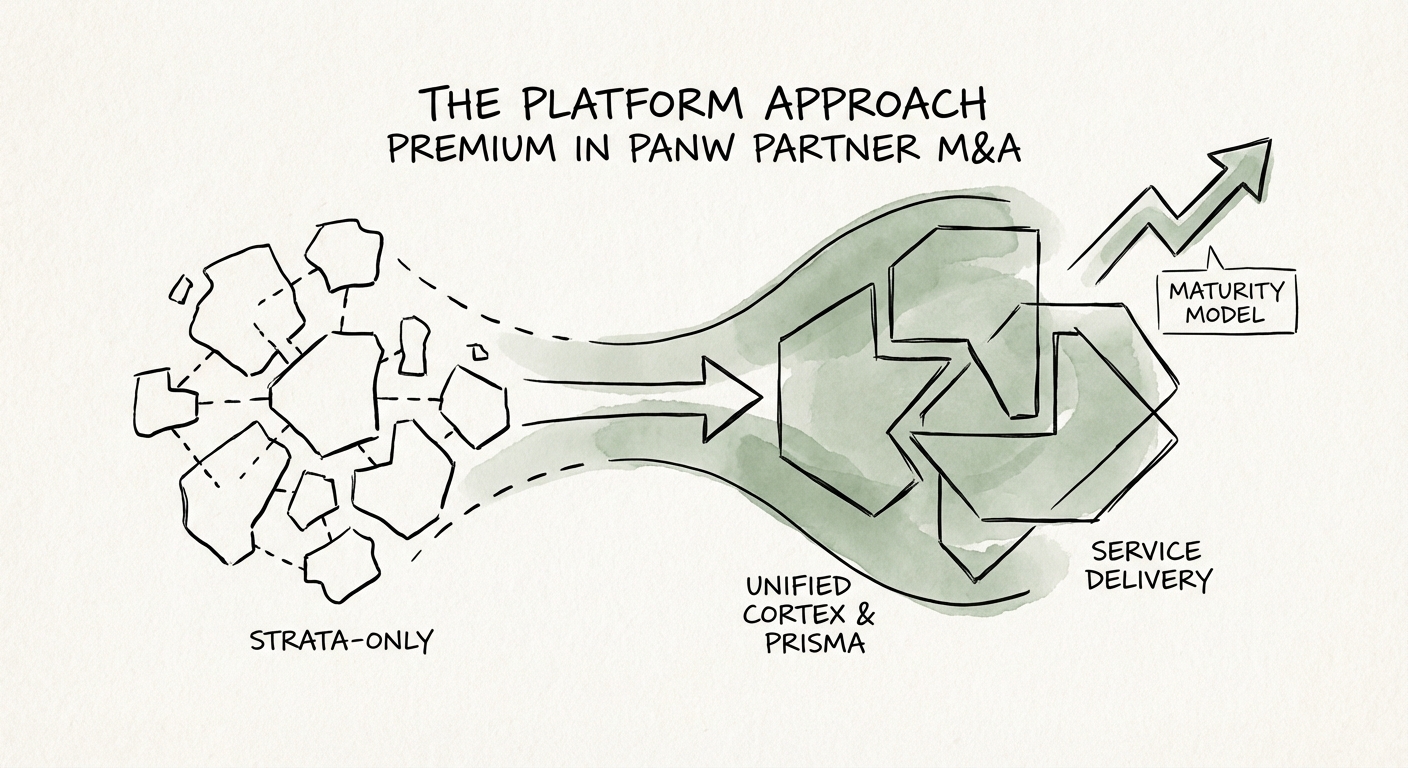

The 'Firewall Trap': Why Strata-Only Shops Are Trading at 6x

For the last decade, the Palo Alto Networks (PANW) ecosystem was a simple volume game. If you could move Strata hardware—the legendary Next-Generation Firewalls (NGFWs)—you had a business. With PANW holding dominant market share, the resale margin was thin but the volume was reliable.

That era is over. In 2026, a Strata-only partner is viewed by private equity acquirers as a logistics provider, not a technology consultancy. The valuation ceiling for these firms is hard-capped at 6x EBITDA. Why? Because hardware resale is non-recurring, low-margin (typically 8-12%), and defenseless against direct procurement. If your value proposition is "we get the boxes there on time," you are competing with CDW, not consulting firms.

We are seeing a significant bifurcation in the due diligence of PANW partners. Acquirers are stripping out hardware resale revenue from the quality of earnings (QofE) entirely, treating it as pass-through revenue with zero multiple value. If 80% of your revenue is Strata resale, your effective enterprise value might be lower than your trailing twelve-month revenue.

In this new era, security is no longer a bolt on. It is a foundational enabler of transformational success... AI is going to act as an accelerant towards the desire to consolidate.

The 'Platformization' Multiplier: The Math Behind 14x

While resellers struggle, a new class of PANW partners is commanding 14x EBITDA multiples. These firms have aligned their service delivery with Nikesh Arora’s aggressive "Platformization" strategy—specifically focusing on Prisma (Cloud Security) and Cortex (AI-Driven SOC).

The valuation premium comes from the shift in revenue quality. A partner deploying Cortex XSIAM isn't just installing software; they are often displacing legacy SIEMs (like Splunk) and taking over the customer's entire Security Operations Center (SOC) workflow. This creates high-margin, sticky managed services revenue (MDR) that trades at premium multiples.

The Margin Mix Shift

Compare the unit economics:

- Strata Reseller: 10% Gross Margin, Transactional relationship.

- Prisma SASE Implementer: 45% Gross Margin, Project-based relationship.

- Cortex/XSIAM Managed Partner: 65% Gross Margin, Multi-year recurring relationship.

Private equity firms are paying the "Platform Premium" for partners who can execute this vendor consolidation. If you can show that your implementation of Prisma Cloud led to the displacement of three point-solution vendors, you demonstrate strategic value that protects your margins from procurement pressure.

The Pivot: From Box Mover to Platform Player

For partners stuck in the "Firewall Trap," the exit strategy requires a rapid pivot to services that support the entire platform. This is not about abandoning Strata—it’s about using the firewall as the wedge to sell the platform.

1. Build the Cortex XSIAM Service Layer: Do not just resell XSIAM. Build a managed detection and response (MDR) wrapper around it. Clients do not want another tool; they want an outcome. Selling "SOC Modernization" services allows you to bill for high-level engineering time rather than SKU resale.

2. Target the 'Vendor Consolidation' KPI: PANW’s own growth metric is "Platformization"—the number of customers using all three pillars (Strata, Prisma, Cortex). Align your own sales compensation to this metric. Partners who drive 3-pillar adoption are receiving preferential deal registration protection and higher backend rebates, which directly flow to EBITDA.

3. Audit Your Technical Debt: A platform approach requires different talent. You cannot service a Cortex deployment with network engineers. You need data analysts and cloud architects. In M&A, we often see "phantom margins" where a partner claims high EBITDA but is severely understaffed on the delivery side for the new technologies they are selling. Fix this ratio before you go to market.