The practical answer

- Short answer

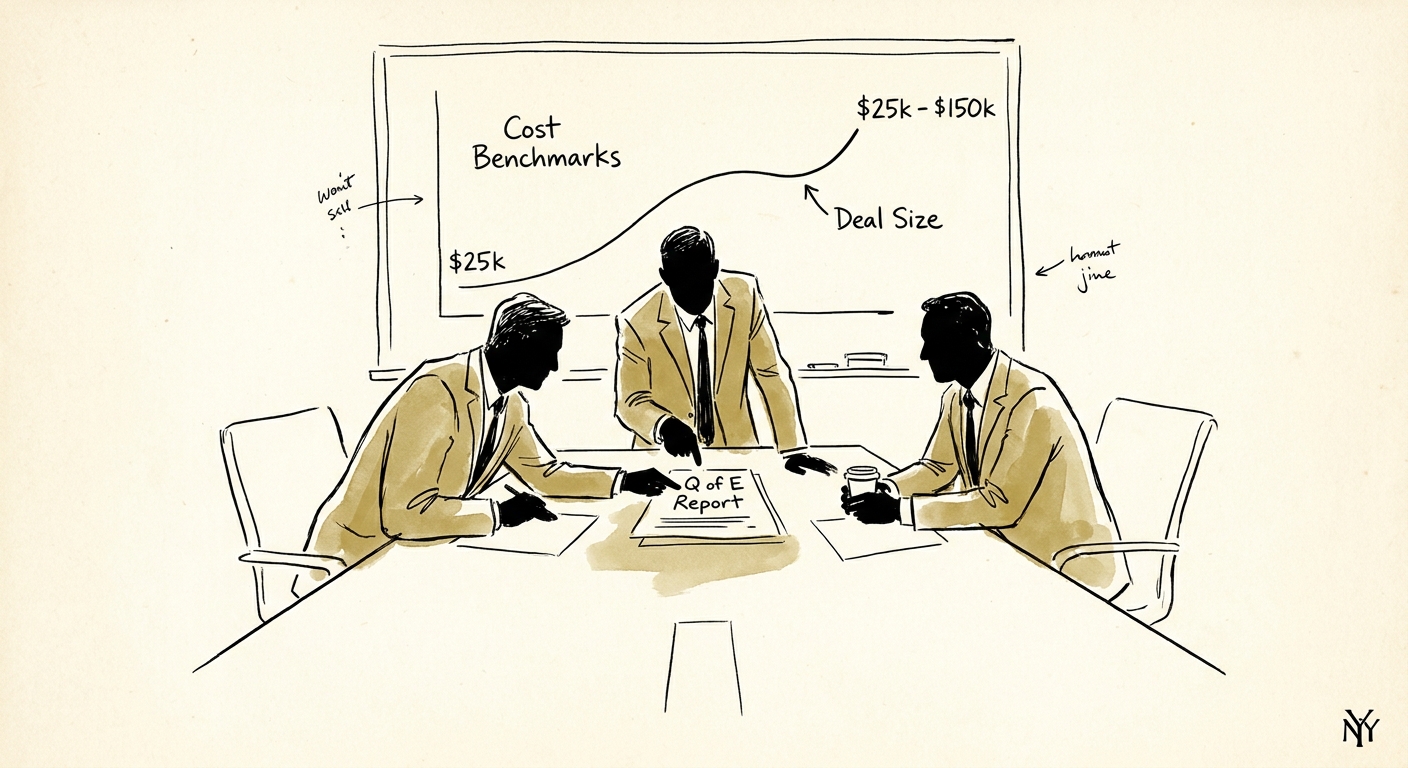

- An operator's guide to Quality of Earnings report costs, with $25k-$150k benchmarks by deal size and the seller preparation areas that protect enterprise value.

- Best fit

- Industry: Technology & B2B SaaS. Function: M&A Diligence

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- $25k-$150k Common QoE cost range by deal size and reporting complexity.

The Cost of Being Unprepared

Founders who treat the Quality of Earnings (QoE) report as an optional due diligence expense often give buyers more room to renegotiate enterprise value late in the process. A CEO may hand over three years of GAAP-compliant financials and assume the numbers speak for themselves. They rarely do. Buyers are underwriting repeatable cash flow, revenue quality, working-capital needs, and normalized EBITDA, not just historical accounting compliance.

In sell-side preparation work, the most common QoE disputes involve deferred revenue schedules, commission capitalization, one-time add-backs, customer concentration, and the working-capital peg. A credible sell-side QoE does not eliminate buyer diligence, but it gives the seller a documented baseline before exclusivity pressure builds. The alternative is negotiating from the buyer's model after the diligence clock is already running.

For technology and tech-enabled services deals, sell-side QoE work commonly lands in the mid-five-figure to low-six-figure range, depending on revenue complexity, entity count, reporting quality, and the advisory firm involved. Understanding the Quality of Earnings vs. Audit distinction is a critical capability for a founder or portfolio company CEO approaching a liquidity window.

A sell-side QoE gives the seller a documented baseline before exclusivity pressure builds and buyer diligence starts shaping the narrative.

Cost Benchmarks: What You Will Actually Pay by Deal Size

The cost of a QoE report scales with the complexity of your revenue recognition, the number of legal entities being consolidated, and the cleanliness of your historical trial balances. A standard audit proves that your accounting was prepared under an accepted standard. A QoE helps buyers evaluate whether the earnings are repeatable.

Sub-$25M EV: The $25,000 to $45,000 Range

For lower-middle-market companies, buyers need a foundational view of normalized EBITDA and cash proof. The scope is narrower, but it still matters. The advisory team focuses on reconciling cash to revenue, verifying one-time EBITDA add-backs, and analyzing customer concentration.

$25M to $100M EV: The $45,000 to $85,000 Range

This is the core middle market, where private equity platform acquisitions live. The scope expands to ARR waterfalls, cohort retention, pricing discounts, executive hiring run-rate impacts, and a defensible EBITDA bridge. Speed is a major ROI driver because clean seller materials reduce avoidable diligence cycles.

$100M+ EV: The $85,000 to $150,000+ Range

At the nine-figure mark, a QoE report becomes a detailed review of the business model across entities, geographies, revenue streams, and product lines. Fees can move past $100,000 because the deliverable may require tax structuring input, IT diligence overlays, ASC 606 revenue recognition review, and working-capital modeling.

The Cheap QoE Trap and the Retrade Reality

The most expensive Quality of Earnings report is the one that fails to earn buyer confidence. If a local tax CPA prepares a financial diagnostic that does not meet institutional diligence standards, the buyer will still hire a transaction advisory firm and may use the new findings to reduce purchase price, narrow add-backs, or tighten indemnification.

When buyers dictate the diligence process, they interpret ambiguity conservatively. If a buyer rejects $500,000 in pro-forma adjustments on a business trading at 10x EBITDA, the seller has a $5,000,000 valuation problem. The point of a sell-side QoE is not to make aggressive claims; it is to prepare the support that makes appropriate adjustments defensible.

A true sell-side Quality of Earnings (QoE) report acts as a credible anchor in negotiations. It forces the buyer to argue against an established, data-dense baseline rather than constructing a conservative model from scratch. Transaction advisory fees are not sunk overhead when they protect the value generated in operations.