The practical answer

- Short answer

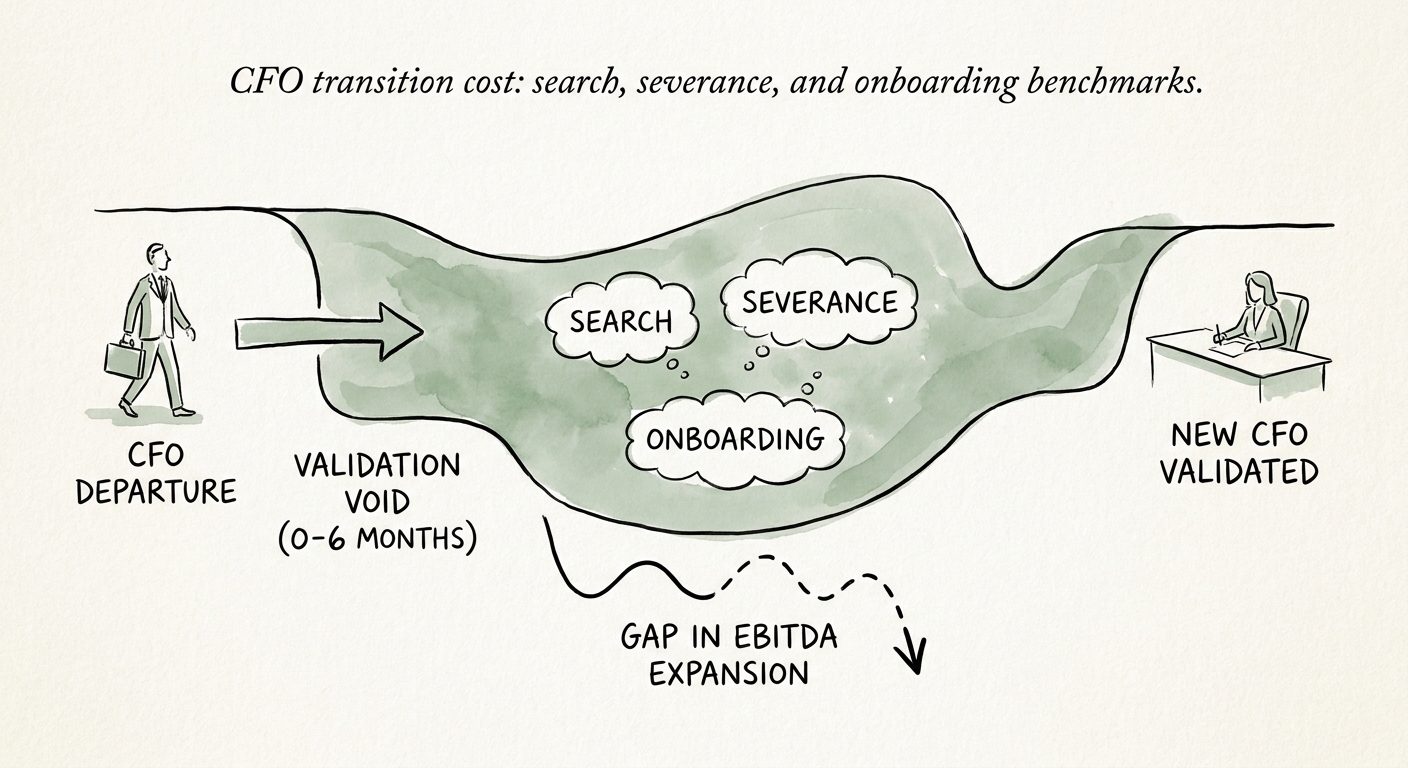

- Replacing a PE portfolio CFO mid-hold runs ~$750K in cash and a $2.1M EV tax. The severance, search, and interim day-rate math sponsors skip until it's too late.

- Best fit

- Industry: Private Equity & B2B SaaS. Function: Finance & Executive Search

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 33% Standard retained executive search fee based on the CFO's first-year projected cash compensation.

Fourteen months after close on a $75M manufacturing roll-up, the board decided the portfolio CFO had to go. The recruiter quoted a $150,000 search fee, the deal team nodded, and everyone moved on to the next agenda item. By the time the replacement was fully productive, the swap had cost north of $2.1 million in enterprise value — and almost none of it appeared in the recruiter's invoice.

I've run this exact transition more than a dozen times across middle-market buyouts, and the financial anatomy of a mid-hold CFO change never varies. There are two ledgers. The first — severance, interim coverage, search — is the one everyone budgets. The second is the one that actually moves your return, and most sponsors don't model it until the value-creation plan is already six months behind.

The tenure math tells you why this keeps happening. Spencer Stuart's CFO Route to the Top puts median PE-backed CFO tenure at roughly 2.8 years, with nearly a third exiting before the 18-month mark. That isn't bad luck. It means a CFO swap is a near-certainty over a typical hold, not an edge case — and a near-certain event you don't price is just a deferred surprise.

Ledger one: the cash you can see

Walk the hard costs in the order they hit the bank account, because that sequencing is what makes them painful. Start with severance. For a portfolio CFO at a $350,000 base, standard agreements run six to twelve months of base continuation, the prorated target bonus, and often a slice of accelerated time-based equity. Cash out the door routinely clears $400,000 before the replacement has even been sourced.

Then you bridge the gap, because you cannot run a portfolio company through a quarter-end close with an empty finance chair. Retained search takes 90 to 120 days. A high-quality interim PE CFO commands $2,500 to $3,500 a day; at four days a week across a four-month search, that's another $160,000 to $224,000 of unbudgeted OPEX. These bands scale tightly with revenue — the portfolio CFO compensation benchmarks by revenue band show exactly how fast they climb past $100M ARR.

The $150K search fee is the line item everyone sees. The six months of stalled value creation is the line item that actually moves your IRR.

Last comes the search fee itself. The retained firms that actually land a proven operator — not a corporate lifer who's never sat through a sponsor board meeting — charge 30% to 33% of first-year projected cash comp. On a $350,000 base with a 40% bonus target, that's $147,000 to $161,000. Stack severance, interim coverage, and the fee, and the visible cash cost of a single CFO swap sits at roughly $750,000.

Now ledger two, the one that decides whether the deal still works. Call it the validation void: the six-month stretch covering the search plus the new CFO's first 90 days. During that window, integration pauses, the margin-expansion projects lose their sponsor, and the 100-day plan quietly slides off the calendar. Heidrick & Struggles' Global CFO Survey finds a newly placed CFO needs roughly six months to reach full productivity — and a portfolio CFO spends most of that runtime rebuilding the model, re-validating the Quality of Earnings, and finding what the last person buried.

That last part is where the EV tax lives. A new CFO almost always opens a few skeletons in the deferred-revenue schedule or the capitalization policy, and "derisking the balance sheet" usually means resetting the EBITDA baseline down 5% to 10%. Apply that reset to the multiple you're carrying the company at, and the visible $750K is the smaller number on the page.

Why three lost quarters wrecks the IRR

The void doesn't just cost money — it costs time, and in a leveraged structure time is the expensive input. If the value-creation plan stalls six months while the new CFO finds their footing, your hold extends by roughly three quarters. With the cost of capital where it is, three extra quarters of carrying cost against a flat EBITDA line is what actually compresses IRR — far more than the search fee ever did. The fix is to collapse the void: the CFO's first 90 days have to move from historical validation to forward capital allocation inside 30, not 90.

What you negotiate before you ever terminate

Every dollar of this tax is cheaper to manage in the offer letter than in the exit. Start with severance triggers. BDO's Private Equity Survey reports that 68% of PE CFOs now push for 12-month severance on a termination without cause. Hold the line at six months of base continuation, conditioned on real transition assistance and non-compete enforcement — not a no-strings payout.

Get the equity mechanics right at grant, because they're unfixable at exit. Never accelerate performance-based equity on termination. The moment an underperforming CFO walks with accelerated carry, you've diluted the pool you need to attract the replacement. Structure agreements so unvested carry is forfeited and recycled straight into the inducement grant for the incoming leader.

Then compress onboarding before day one. Make the interim CFO's deliverable a complete data room of the financial infrastructure — every balance-sheet account tied to its sub-ledger — so the new hire walks into a mapped system instead of tribal knowledge. If you're inserting a first-timer rather than a repeat operator, the playbook for installing a first-time CFO is the difference between a 30-day ramp and a six-month one.

Here's the Monday move: before the next board meeting where someone proposes the change, build the two-ledger model. Line one is the ~$750K of cash. Line two is the EBITDA reset times your carrying multiple, plus three quarters of hold extension against your fund's cost of capital. Put both numbers in front of the board, then decide. You'll either keep the CFO and fix the gaps, or you'll terminate with the interim coverage, severance cap, and 30-day onboarding plan already locked — which is the only version of this transition that protects the multiple.