The practical answer

- Short answer

- A $150M roll-up was leaking $1M/year in idle cash. The exact DCOH, 13-week forecast, and sweep benchmarks that turn a portfolio company's operating account into yield.

- Best fit

- Industry: B2B SaaS, Manufacturing, and Professional Services. Function: Finance & Treasury

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 92% Industry standard for 13-week rolling cash flow forecast accuracy to enable automated sweeps.

The fastest EBITDA you'll find this quarter is already in your own bank account

The first thing I check when I sit down with a portfolio CFO is not the P&L. It's the bank login. Specifically, the rate line on the primary operating account. Nine times out of ten, on a middle-market company carrying tens of millions in deposits, that number starts with a zero and a decimal point.

On a $150M manufacturing roll-up last quarter, it read 0.15%. There was $22 million parked in a single legacy regional bank account — money that had quietly accumulated through three bolt-on acquisitions and never been touched. The CFO wasn't negligent. He was scared. Supply-chain volatility had burned him in 2022, so he'd built a 45-day cushion and slept better for it. The cushion was costing the company north of $1 million a year in foregone yield versus money-market instruments paying multiples of what that deposit earned. That's a million dollars of pure EBITDA, available without shipping one more unit, hiring one more rep, or renegotiating one contract.

This is the part operating partners underestimate. Cash drag doesn't show up as a line you can hunt for — it hides inside "interest income" being a rounding error instead of a number. And it compounds at exit: a million in recurring, zero-effort earnings, capitalized at a mid-market multiple, is several million in enterprise value you are leaving on the table because nobody swept the account.

The instinct behind the buffer isn't irrational, it's just stale. The 2025 AFP Liquidity Survey found that 61% of organizations still name "safety" as their top short-term investment objective and park 46% of short-term cash in plain bank deposits. The problem is that "safe" got redefined. A swollen balance in one commercial bank isn't safety — it's uninsured counterparty concentration earning nothing, which is exactly the exposure that should keep a CFO up at night.

A 45-day cash buffer is not a risk control. It is a confession that the CFO can't forecast the next 13 weeks — and is hoarding to cover the blind spot.

The four numbers that replace the gut-feel buffer

"How much cash should we hold?" is the wrong question. It invites a feeling. The right question is "how much variance do we actually have over the next 13 weeks, and how fast can we get money back out of yield if we're wrong?" Answer that with numbers and the buffer sizes itself. Here are the four I hold portfolio CFOs to.

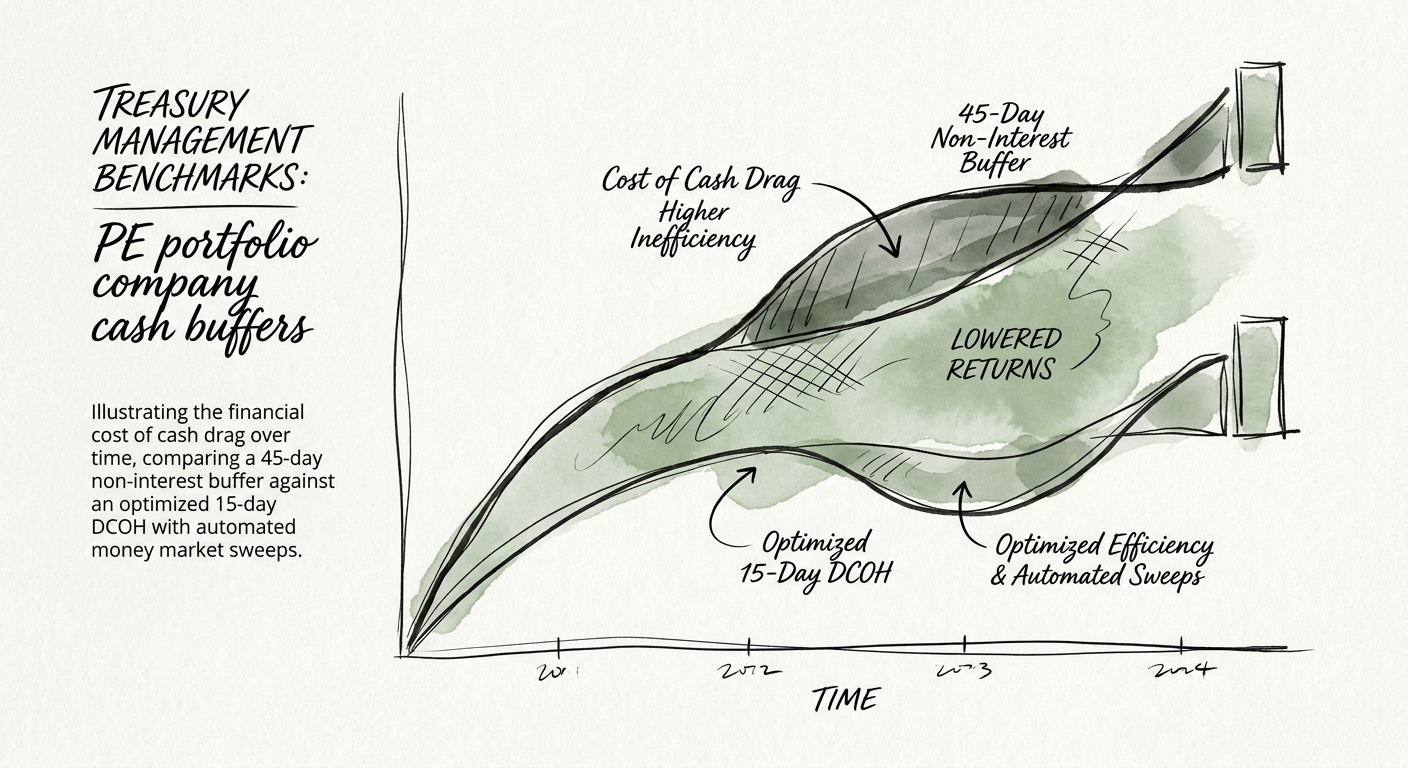

Days Cash on Hand: stop benchmarking against your fear

The buffer is a shock absorber for normal weekly variance — not an insurance policy against the business failing. For a SaaS or tech-enabled company with predictable subscription inflows, 12 to 15 days is plenty. The manufacturing roll-up is different by nature: longer cash conversion cycles, lumpy supplier terms, real receivables risk. There I'll defend 20 days. Past 25, you're no longer managing liquidity — you're hoarding, and the number is telling you the working-capital cycle itself is broken. Note the spread: the right DCOH for a parts distributor is not the right DCOH for a recurring-revenue software company, and a single portfolio standard applied to both is how you end up over-buffered in the predictable businesses and under-disciplined in the volatile ones.

13-week forecast accuracy: the lever that shrinks everything else

You cannot safely run a thin buffer if you can't see the next quarter. The benchmark for a rolling 13-week cash forecast is 92% accuracy. When variance runs hotter than 8%, the finance team has no choice but to hoard — the cash pile is just padding for the forecast they don't trust. Fix the forecast first and the buffer collapses on its own. We treat this as a core line in our weekly portfolio monitoring KPIs, because every other treasury decision downstream depends on it.

The 80/20 split: where the money actually lives

No more than 20% of liquid assets should sit in operating accounts doing transactional work. The other 80% belongs in liquid, yield-bearing vehicles — government or Treasury money-market funds that you can redeem same-day. The CAIA Association has been blunt that unsophisticated cash management is a measurable performance drag on private capital, and this is precisely where it bites: idle deposits earning the bank's spread instead of yours.

Counterparty count: the number nobody tracks

That $22M sat in one bank. If the sweep math says hold less and diversify the rest, you also quietly retire a single-point-of-failure exposure most CFOs never quantify. Same dollars, less risk, more yield — the rare three-way win.

What to actually do before the next board meeting

This isn't a controller's side project. It needs a sponsor mandate and a CFO who'll execute it, because the resistance is psychological as much as operational. Here's the sequence that works, in order.

Week one: pool the cash so you can see it. If your portfolio company runs multiple legal entities — and post-roll-up it almost always does — set up Zero-Balance Accounts that sweep every entity's daily balance into one master header account each night. The point isn't just consolidation; it's that you suddenly have a single, accurate daily cash position. If your CFO can't state the company's total cash by 9 a.m. without three people pulling statements, you don't have a treasury function, you have a scavenger hunt.

Weeks two to four: automate the sweep above the threshold. Once the master account is live, set a standing instruction: anything above the DCOH threshold pushes automatically into institutional money-market funds or short-duration Treasury bills. Automation matters here for a non-obvious reason — it removes the human hesitation. A CFO will always find a reason to leave "just a little extra" in the account this week. The rule doesn't have a feeling. It just sweeps.

In parallel: rebuild the 13-week forecast off live data. A hand-maintained spreadsheet that one person updates is both a control gap and the reason the buffer stays fat. Move to a tool that pulls payables, receivables, and bank feeds straight from the ERP, so the finance team spends its time on variance analysis instead of data entry. When the forecast is trustworthy, the case for a 45-day cushion evaporates — there's nothing left to be afraid of. A new CFO's first 90 days is the natural window to force this, before the old habits re-anchor.

Then use your new leverage. Consolidated liquidity is a negotiating chip. A bank that was paying you 0.15% on scattered balances behaves very differently when it sees one large, well-managed master account it might lose. Make them compete on yield, fees, and earnings credit rate. As the Deloitte Global Corporate Treasury Survey documents, treasury has shifted from back-office plumbing to a strategic function — and your banking relationships should be priced like it. Do these four things and the silent drain on EBITDA stops, the working-capital cycle de-risks, and you've built exactly the financial discipline an acquirer pays a premium for.