The practical answer

- Short answer

- Not all ARR is created equal. Learn how PE firms score revenue quality in 2026 and why low-quality revenue streams trigger 30% valuation discounts.

- Best fit

- Industry: Private Equity / B2B SaaS. Function: Finance / Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 110% NRR threshold required to command premium (10x+) valuation multiples in 2026, provided GRR remains above 90%.

The $10M Lie: Why Your Top-Line Number is Misleading

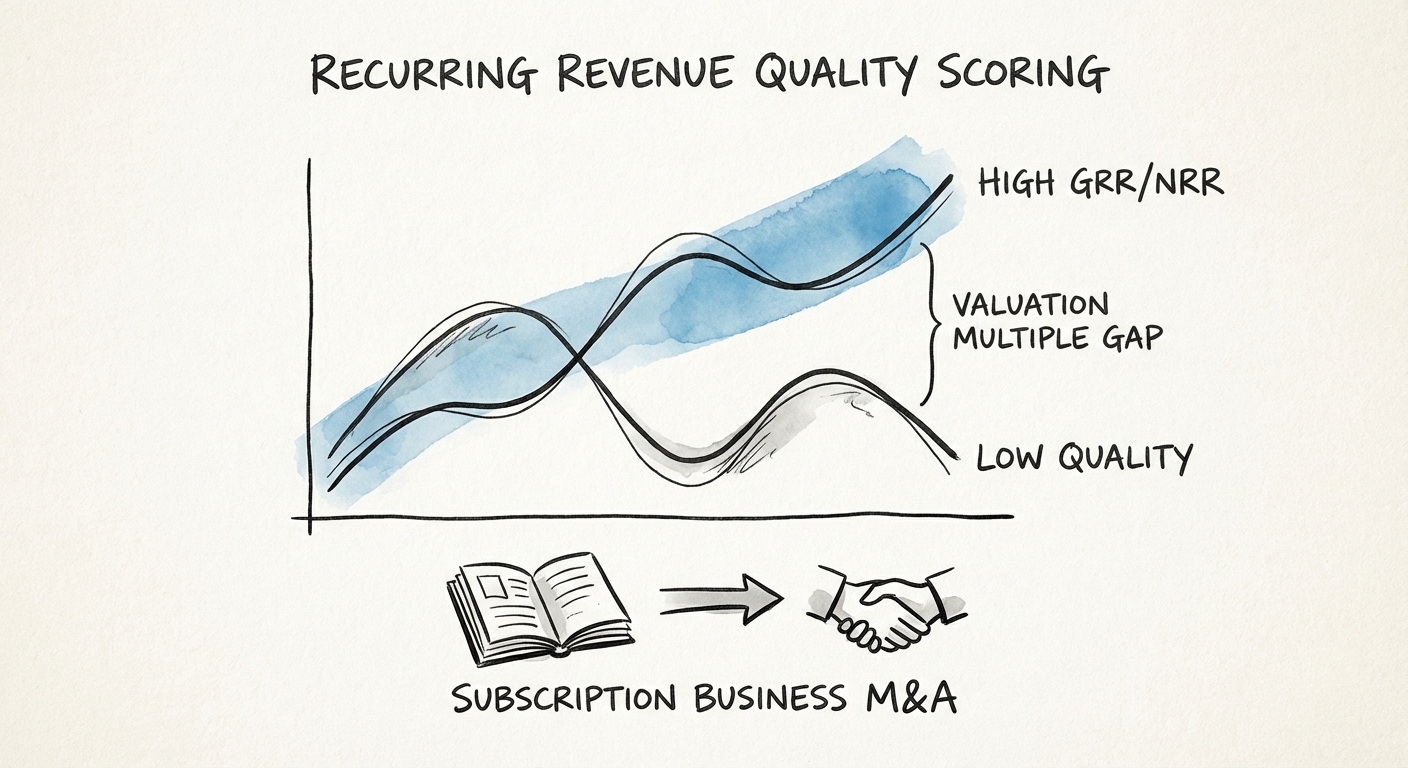

In the zero-interest rate era, Annual Recurring Revenue (ARR) was treated as a monolith. A dollar of revenue from a month-to-month SMB contract was valued roughly the same as a dollar from a three-year enterprise agreement. In 2026, that logic has been inverted. Private Equity firms and strategic acquirers have moved from "Growth at All Costs" to "Quality of Earnings," creating a bifurcated market where two companies with identical $10M ARR figures can trade at vastly different multiples—one at 4x and the other at 12x.

The differentiator is Revenue Quality. Sophisticated buyers now apply a "Quality Score" to every dollar of ARR, penalizing revenue streams that carry hidden risks such as high churn, low gross margins, or excessive service delivery costs. This scoring process occurs long before the Quality of Earnings (QofE) report; it starts during the initial data room review. If your revenue mix is weighted toward "low-quality" ARR, you aren't just facing a lower multiple; you are facing a potential re-trade or deal collapse.

The "Masking" Effect of High NRR

One of the most dangerous signals in 2026 due diligence is the "Masking" effect. This occurs when a company boasts strong Net Revenue Retention (NRR)—often above 110%—while suffering from poor Gross Revenue Retention (GRR). This signals that the company is churning customers at an alarming rate but hiding the leakage by aggressively upselling the survivors. While this works for venture growth stories, it is a red flag for PE buyers looking for platform stability. In the eyes of an acquirer, 110% NRR with 80% GRR is significantly less valuable than 105% NRR with 95% GRR.

In 2026, a dollar of revenue is no longer just a dollar. PE buyers are paying 12x for 'sovereign' recurring revenue and 4x for 'leaky' subscription revenue. The gap isn't in the product; it's in the contract quality and retention mechanics.

The 5-Point Revenue Quality Diagnostic

To maximize exit value, Operating Partners and Founders must audit their revenue streams against the same scorecard buyers will use. A "Premium Quality" revenue stream scores high on all five dimensions, while deficits in any area serve as drag coefficients on your valuation multiple.

1. Retention Quality (The GRR/NRR Split)

Benchmark: Premium multiples (10x+) require GRR > 90% and NRR > 110%.

Revenue from cohorts with GRR below 85% is often treated as "melting ice cubes" and discounted by 20-30%. If your expansion relies solely on price increases rather than seat/usage expansion, the quality score drops further, as this indicates pricing power risk rather than product value.

2. Margin Quality (The Service Trap)

Benchmark: 80%+ Gross Margin on Subscription Revenue.

In 2026, buyers are aggressively stripping out "hidden services" from COGS. If your Customer Success team spends 40% of their time on manual onboarding or support ticket resolution, that cost is reallocated to COGS, depressing your gross margins. ARR with 60% gross margins trades like a services business (1.5x revenue), not a software business.

3. Contract Quality (The Commitment Index)

Benchmark: Multi-year, paid upfront, with auto-renewal.

Monthly contracts are no longer viewed as "frictionless"; they are viewed as "unsecured." Revenue secured by 3-year contracts with aggressive price escalators commands a premium because it guarantees cash flow visibility during the debt-service period of a leverage buyout.

4. Concentration Risk

Benchmark: No single customer > 10% of ARR.

High concentration doesn't just lower the multiple; it increases the holdback and escrow requirements, reducing cash at close. In 2026, buyers are also scrutinizing "vertical concentration"—exposure to a single distressed industry.

5. Usage Predictability

Benchmark: <15% volatility quarter-over-quarter.

With the rise of usage-based pricing models, "estimated" overages are often excluded from ARR calculations until they are historically proven. Revenue based on "projected usage" is frequently haircut by 50% in the final valuation.

The "Fake ARR" Trap: Preparing for the QofE Defense

The fastest way to lose credibility (and value) in a deal is the discovery of "Fake ARR" during diligence. This occurs when non-recurring revenue is classified as subscription revenue to inflate the top line. Common culprits in 2026 include:

- Setup Fees Amortized as ARR: Including implementation fees in the recurring bucket.

- "Pilot" Revenue: Counting 3-month paid pilots as annual contracts.

- Conditional Revenue: ARR tied to performance milestones or future feature delivery.

- Service-Disguised-as-SaaS: "Managed Services" contracts that require human labor but are billed as subscriptions.

Actionable Advice: Conduct a "Sell-Side Revenue Audit" 12 months before exit. Segment your ARR into "Tier 1" (High Quality) and "Tier 2" (At Risk). Proactively separate lower-quality revenue streams in your CIM (Confidential Information Memorandum). Presenting $8M of "Platinum" ARR and $2M of "Other Recurring Revenue" yields a higher blended multiple than claiming $10M of ARR that gets shredded in diligence.

By proactively scoring your revenue quality, you move the negotiation from "defending the number" to "validating the quality," positioning your firm as a premium asset in a skepticism-first market.