The practical answer

- Short answer

- A buyer's diligence team will tear your channel P&L into four revenue streams and price each one separately. Here's how to see your reseller business the way they will.

- Best fit

- Industry: Software & IT Services. Function: M&A Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 0.8x Average Revenue Multiple for Pure Resell (vs. 12x for IP)

One P&L walks in. Four companies walk out.

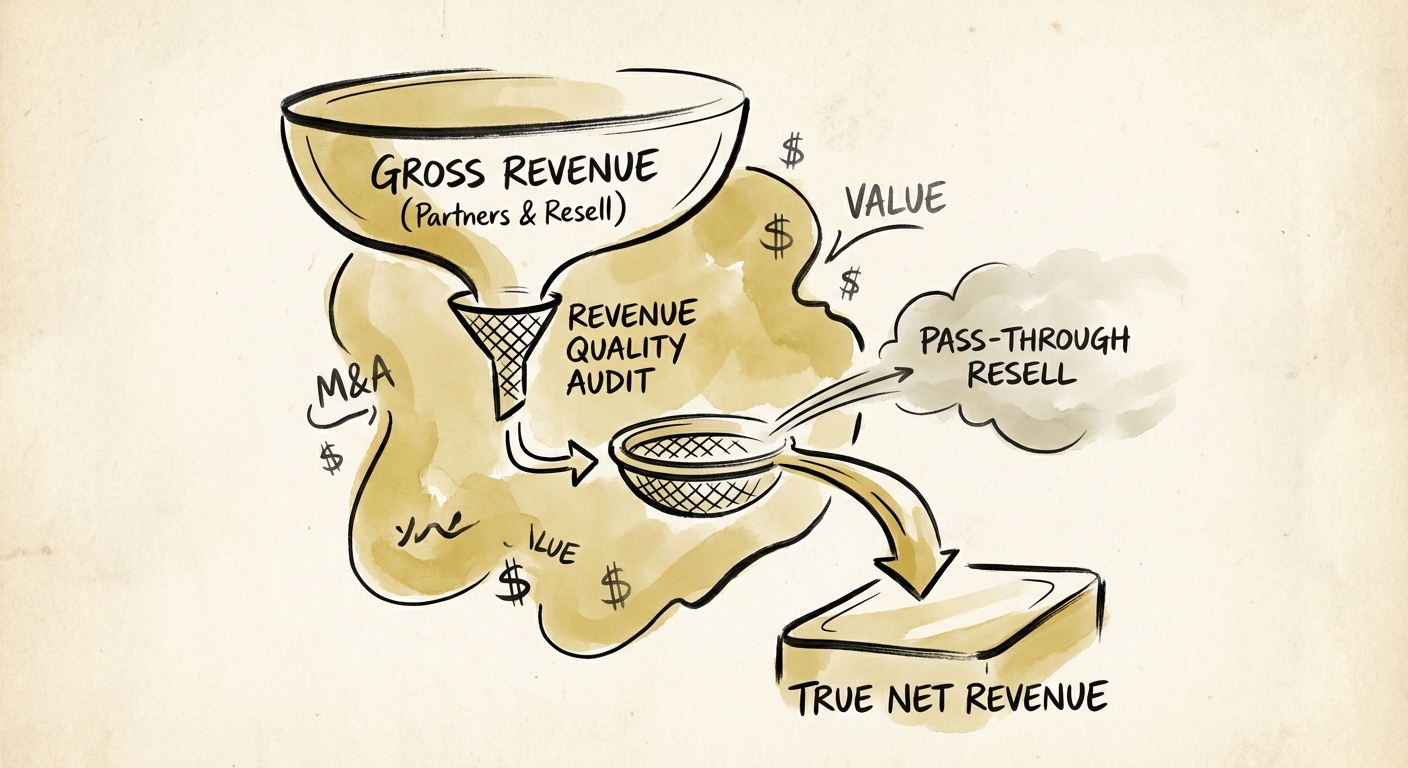

Picture the management presentation. A founder clicks to slide three: "$50M in revenue, 28% CAGR, Microsoft Solutions Partner with five designations." The room nods. Then the buy-side analyst — the one who hasn't said a word — opens the trial balance and starts highlighting cells. By the end of the week that $50M has been quietly carved into a $32M license-resell line, an $11M implementation-services line, a $5M managed-services book, and a $2M sliver of repeatable IP. Four businesses, four risk profiles, four multiples. The headline number never gets quoted again.

This is the part founders in the Microsoft, AWS, and Salesforce ecosystems consistently misjudge. In a channel business, "revenue" is not one thing — it's a stack of fundamentally different assets that happen to share an invoice template. The buyer is not buying your top line. They are buying the worst-priced stream you have too much of, and the best-priced stream you have too little of.

What the resell line actually is

When you book $32M in license resale, the buyer doesn't see $32M of enterprise. They see procurement. You are a billing intermediary between the vendor and the end customer, earning 8–15 points of margin for the privilege, on terms the vendor can change unilaterally. Microsoft's New Commerce Experience reset partner economics across an entire ecosystem in a single program change. AWS adjusts discount tiers and marketplace mechanics on its own cadence. None of that requires your sign-off. A revenue stream that can be compressed by an email from a vendor you don't control is, in valuation terms, a liability dressed as growth.

So the analyst nets it out. They report Gross Revenue minus the cost of the resold licenses, and the $50M company suddenly has a $20M-ish "net revenue" reality. That reframing is the whole ballgame — and it's why the right starting question in a channel deal is never "how big is your top line," but "how much of this revenue would survive a vendor changing its mind?"

The fastest way to lose a turn of EBITDA in diligence is to call pass-through license resale "revenue." A buyer's QofE team will find it in an afternoon, strip it out, and reprice you to a VAR multiple before you've finished your coffee.

The four streams, and what each one is worth

Channel partners get valued on a sum-of-the-parts basis because they are, functionally, a sum of parts. Drawing on the SaaS and services deal data in Software Equity Group's 2026 M&A reporting and the broader private-equity backdrop in Bain's Global Private Equity Report, here is how a buyer prices each layer — and the trap inside each one.

Stream 1 — License resale: the anchor that drags

High volume, 8–15% margin, usually non-exclusive. Priced on EBITDA at a commodity-logistics multiple, because that's what it is. The danger isn't the low multiple itself — it's the gravitational pull. When resell crosses roughly 60% of revenue, buyers stop valuing the rest separately and reprice the whole firm as a VAR. Your services and IP get quietly absorbed into the reseller discount. Mix matters more than size precisely here.

Stream 2 — Professional services: good money, headcount-shaped

Implementation, migration, custom development at 40–50% gross margin. Genuinely valuable, and it trades at a healthy EBITDA multiple — but it scales linearly with bodies. Every dollar of new revenue needs a new hire, so a buyer caps what they'll pay for it. This is the stream most founders overweight in their own heads; it feels like "real" technical work, but to a buyer it's a labor business with a ceiling. (We unpack the margin mechanics in managed services vs. professional services valuation.)

Stream 3 — Managed services: where predictability gets paid

Multi-year recurring contracts — infrastructure management, a SOC, ongoing support — at 50–65% gross margin. Now you're priced on recurring revenue rather than EBITDA, because the dollars renew without a new sale. This is the first stream where a buyer leans forward. The premium isn't for the margin; it's for the fact that the revenue shows up next quarter whether or not your sales team does anything.

Stream 4 — Proprietary IP: the SaaS multiple hiding in your services

Repeatable code, accelerators, a productized solution layer sold through the channel, at 80%+ margin. Valued on growth rate and net revenue retention — the same lens Kellblog applies to SaaS multiples and the Rule of 40. This is the $2M sliver that, if it's growing and retaining, can be worth more than the $32M resell line beneath it. The whole game of a channel exit is shifting weight from stream one toward stream four — and proving the shift is real, not a slide.

The 18-month playbook to reprice the firm before you sell it

You don't fix revenue mix in the data room — you fix it in the year and a half before. A $50M partner that moves even 10% of revenue from resell into managed services or IP can lift enterprise value by 30–40%, because those dollars cross from a commodity multiple into a recurring or growth multiple. Three moves, in order:

- Net out the pass-through in your own board pack first. Don't wait for a buyer's QofE team to do it to you. Report Net Revenue — gross minus the cost of resold licenses — as your headline number starting now. Two things happen: your real growth rate stops being flattered by vendor volume, and you arrive at the deal already speaking the buyer's language instead of getting repriced live in front of them.

- Turn your best service into a product. Find the implementation pattern your team has run twenty times — the migration script, the security-baseline package, the industry-specific configuration — and sell it as a fixed-price accelerator with a name and a SKU. The point isn't the price tag; it's the signal. Fixed-price repeatable delivery tells a buyer your revenue is starting to decouple from headcount, which is the single trait that moves you up the multiple ladder.

- Instrument attach rate and report it monthly. Track the share of resell deals that ship with an attached managed-services or IP contract. This one metric is the proof that your high-value streams are riding on your low-value volume rather than living in a separate, fragile silo. Top-quartile channel partners are landing attach rates above 40%; a buyer who sees that number trending up will underwrite your future mix, not just your trailing one.

The instinct in the channel is to chase the next big license deal because it's the fastest way to make the top line bigger. In an exit, it's often the fastest way to make the company worth less. For how this plays out in a specific ecosystem, see our breakdown of AWS partner revenue mix, and for the deal-structure side, the 2025 IT services M&A trends. The question to put on your own board agenda this month isn't how much you're selling — it's how much of what you sell you actually own.