The practical answer

- Short answer

- Analysis of Splunk partner growth stages from $5M to $50M. Why 'Log Collectors' trade at 6x while Security Intelligence firms command 14x in the Cisco era.

- Best fit

- Industry: Cybersecurity & Observability. Function: Strategic Growth & M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14x EBITDA multiple for Splunk partners with >40% Managed Security revenue vs. 6x for pure resale/implementation shops.

The Cisco Era: Why 'Partnerverse' Status No Longer Guarantees Value

For the last decade, the path to a premium valuation as a Splunk partner was relatively straightforward: achieve Elite status, amass certifications, and drive ingest volume. That playbook expired in March 2024 with Cisco's $28 billion acquisition.

As we approach the full integration of Splunk Partnerverse into the Cisco 360 Partner Program in February 2026, the valuation criteria have shifted violently. Private equity buyers are no longer paying premiums for partners who simply resell compute and storage ('Log Collectors'). In the Cisco era, ingest is a commodity; intelligence is the asset.

The market has bifurcated. On one side are traditional infrastructure resellers trading at 4x-6x EBITDA, viewed as 'low-margin fulfillers' in the massive Cisco ecosystem. On the other are specialized Security Operations and Observability consultancies trading at 12x-14x EBITDA. These firms have pivoted from selling 'data volume' to selling 'outcomes'—specifically utilizing the Cisco Data Fabric and AI Canvas to deliver predictive security postures rather than reactive log management.

In the Cisco era, ingest is a commodity. If your business model depends on how much data a customer stores, you are in a race to the bottom. If it depends on how much risk you remove, you are a strategic asset.

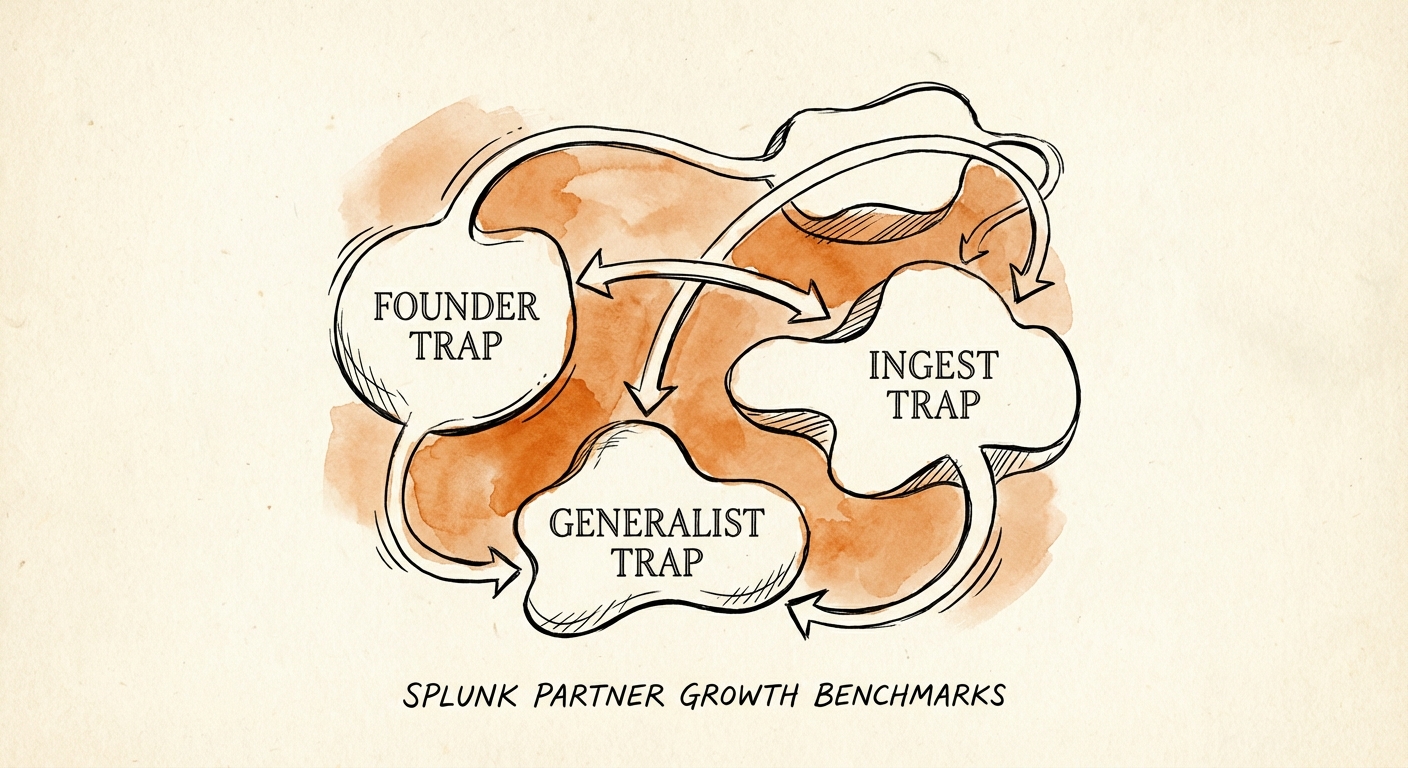

The Three Growth Stalls: Where Splunk Partners Get Stuck

Scaling a Splunk practice requires navigating three distinct 'valleys of death' where revenue grows but enterprise value (valuation) flatlines.

Stall 1: The 'Splunk Ninja' Trap ($3M - $8M Revenue)

At this stage, the firm is built around a technical founder or a 'hero architect' who knows SPL (Search Processing Language) better than anyone. Margins are high (30%+ EBITDA), but transferability is zero.

- The Symptom: Every complex deployment requires the founder's personal involvement.

- The Valuation Killer: Buyers see 'Key Person Risk' and apply a 30-50% discount.

- The Fix: Productize the 'Ninja' knowledge into documented playbooks and automated detection rules that junior engineers can deploy.

Stall 2: The 'Ingest' Trap ($10M - $20M Revenue)

The firm has scaled by reselling large licensing deals and attaching basic implementation services. You have 'Elite' status, but your gross margins on services are eroding as customers push back on billable hours for standard integrations.

- The Symptom: Revenue is growing, but Service Gross Margins are stuck below 40%.

- The Valuation Killer: You look like a low-margin VAR (Value Added Reseller) disguised as a consultancy.

- The Fix: Pivot to Managed Detection and Response (MDR) or 'Observability-as-a-Service' models to build recurring revenue that isn't tied to license resale.

Stall 3: The 'Cisco Generalist' Trap ($25M+ Revenue)

As you integrate into the broader Cisco ecosystem, the temptation is to dilute your Splunk focus to chase general networking or XDR opportunities. This creates a 'jack of all trades, master of none' profile.

- The Symptom: utilization drops as the team struggles to cross-skill between Splunk Core, Enterprise Security (ES), and the broader Cisco security stack.

- The Valuation Killer: Strategic acquirers want deep specialization. A 'diluted' $30M partner is worth less than a focused $15M specialist.

- The Fix: Double down on high-value niches like Industrial OT Security or Financial Services Fraud Detection using Splunk's advanced AI capabilities.

The 14x Blueprint: Metrics of a 'Security Intelligence' Asset

To command a premium multiple in 2026, a Splunk partner must look less like a reseller and more like a Data Product company. The firms trading at 14x EBITDA share these specific characteristics:

1. Proprietary IP Mix > 15%

Top-tier partners don't just implement Splunk; they install their own IP on top of it. This could be a library of industry-specific detection rules (e.g., 'Healthcare Ransomware Pack') or a custom connector for the Cisco Data Fabric. This IP creates vendor lock-in and high-margin recurring revenue.

2. Managed Services Revenue > 45%

Project-based revenue is lumpy and discounted by PE firms. The 'Gold Standard' is 50% recurring revenue, specifically from high-value managed services (not just support contracts). This proves you are owning the outcome, not just the installation.

3. Cisco Partner Value Index Strategy

With the shift to the Cisco 360 program, 'badges' matter less than the Partner Value Index. Winners are optimizing for the 'Performance' and 'Engagement' metrics—demonstrating active customer lifecycle management and expansion, rather than just initial transaction volume.