The practical answer

- Short answer

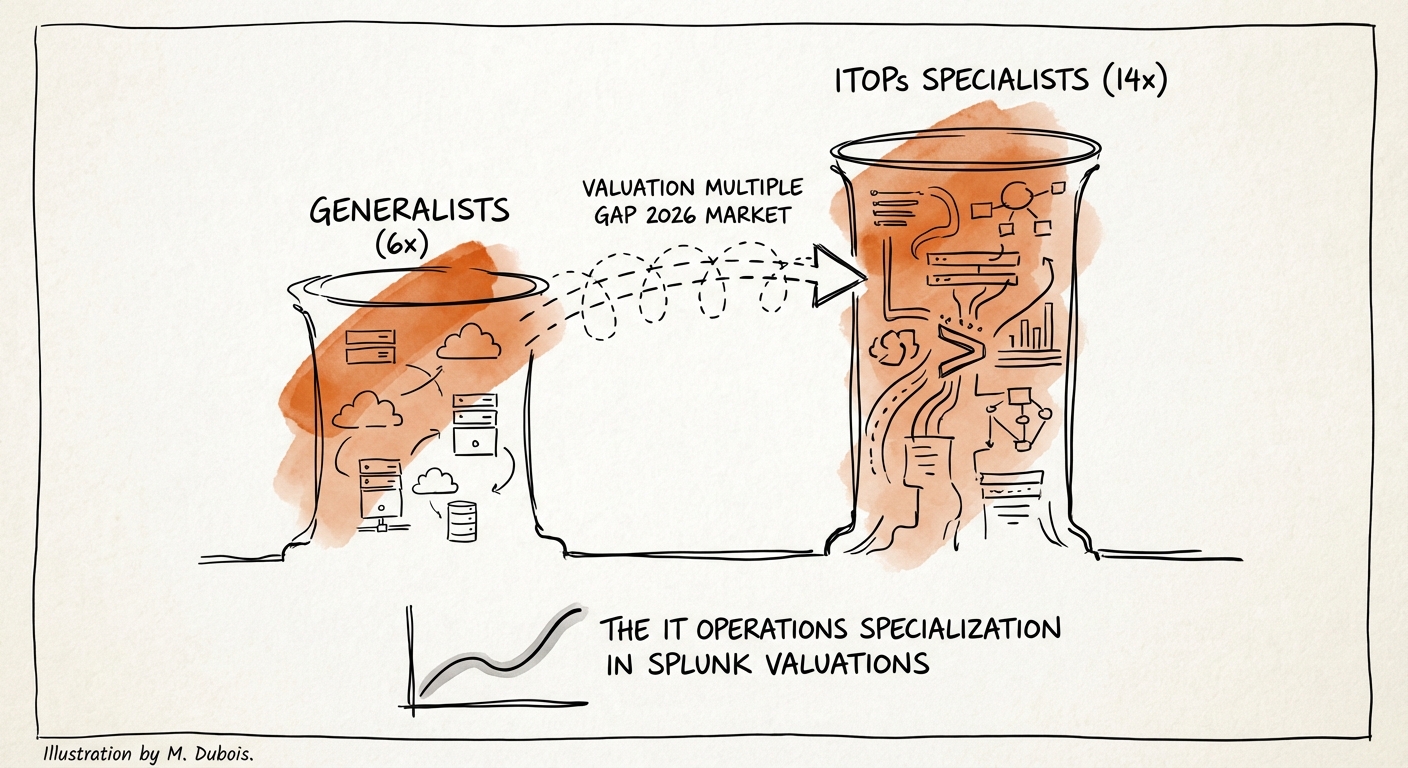

- Why Splunk partners with ITSI and Observability specializations trade at 14x multiples while generalist log collectors stall at 6x. A diagnostic for PE investors.

- Best fit

- Industry: Private Equity. Function: Exit Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14x EBITDA multiple for Splunk partners with 'Predictive Observability' and ITSI capabilities.

The "Log Collector" Discount vs. The Observability Premium

In the wake of Cisco’s $28 billion acquisition of Splunk, the partner ecosystem has bifurcated into two distinct valuation classes: the legacy “Log Collectors” and the modern “Predictive Strategists.” For private equity investors evaluating Splunk consultancies, the distinction is worth approximately 8 turns of EBITDA.

For a decade, the Splunk economy was driven by ingestion. Partners were rewarded for helping customers pump terabytes of log data into the platform, primarily for security information and event management (SIEM). These firms built business models on resale margin and time-and-materials implementation. In 2026, this model is a valuation trap. With the commoditization of log storage and the shift to “Workload Pricing,” the strategic value of pure ingestion has collapsed. These generalist firms now trade at 6x-8x EBITDA, viewed largely as staffing augmentation businesses with low recurring revenue quality.

The premium multiple—12x to 14x EBITDA—has shifted to partners specializing in IT Operations (ITOps) and Observability. These firms leverage Splunk IT Service Intelligence (ITSI), AIOps, and the Splunk Observability Cloud to transform reactive data into predictive business insights. They don’t just index logs; they map business services, predict outages before they impact revenue, and automate remediation. To a strategic acquirer, these partners are not selling hours; they are selling operational resilience. They command higher retention rates because they own the “Service Health” dashboard used by the CIO, not just the search bar used by the security analyst.

The market has stopped paying for 'data plumbers' who just move logs from A to B. The 14x multiple belongs to the 'data architects' who can predict a revenue outage 30 minutes before it happens.

The Cisco Factor: Why "Full-Stack" Drives the Multiple

The integration of Splunk into the Cisco 360 Partner Program (launching February 2026) has accelerated this valuation gap. Cisco’s strategy hinges on “Full-Stack Observability” (FSO)—the convergence of network visibility (ThousandEyes), application performance (AppDynamics), and data analytics (Splunk). Partners who remain siloed in “Splunk Classic” (on-premise Enterprise Security) are effectively locking themselves out of the ecosystem’s primary growth engine.

The valuation premium is now attached to partners who bridge the gap between AppDynamics and Splunk ITSI. Investors should look for the “FSO Metric,” which measures the percentage of a partner’s customer base utilizing both Application Performance Monitoring (APM) and Infrastructure Monitoring. A partner capable of correlating a Cisco network spike with a Splunk application log to predict a checkout failure is an asset that commands a strategic premium.

The "Predictive Revenue" Diagnostic

To determine if a target asset is a “Log Collector” or a “Predictive Strategist,” examine their revenue composition through the lens of the ITSI Maturity Curve:

- Level 1 (Commodity): Revenue is derived from installing forwarders and writing basic search queries. Valuation: 6x.

- Level 2 (Reactive): Revenue includes building dashboards and alerts, but they are static and threshold-based. Valuation: 8x.

- Level 3 (Predictive): Revenue is tied to Service Decomposition and AIOps configuration. The partner has defined “Glass Tables” that map IT metrics to business KPIs (e.g., “Checkout Latency” vs. “Revenue Risk”). Valuation: 12x+.

Firms operating at Level 3 generate sticky, high-margin managed services revenue because they effectively insure the client’s revenue stream against downtime.

Strategic Action Plan: Pivoting to the 14x Profile

For PE operating partners holding a Splunk consultancy, the path to a premium exit involves a rapid pivot from “Ingest” to “Insight.” This requires three specific operational shifts over a 12-month horizon.

First, audit the talent bench for ITSI certification. The market is flooded with “Splunk Certified Power Users” (generalists), but “Splunk ITSI Administrators” are scarce. A firm with a high density of ITSI-certified consultants possesses a defensive moat. If your ratio of Generalists to ITSI Specialists is greater than 5:1, you are a commodity shop. Aim for a 3:1 ratio to signal specialization.

Second, package IP around "Business Service Monitoring." Stop selling “Splunk Implementation” SOWs. Start selling “Retail Operations Resilience” or “Healthcare Patient Flow Monitoring” packages. These should be fixed-price, outcome-based engagements that deploy pre-built ITSI Service Trees and KPI templates. This shifts the revenue quality from T&M to IP-enabled Services, directly impacting the EBITDA multiple.

Finally, align with the Cisco FSO play. Actively pursue the Cisco Observability specializations. A Splunk partner that can articulate a joint value proposition with Cisco AppDynamics becomes an attractive M&A target not just for other SIs, but for the broader ecosystem of Global Systems Integrators (GSIs) looking to fill their FSO practice gaps.