The practical answer

- Short answer

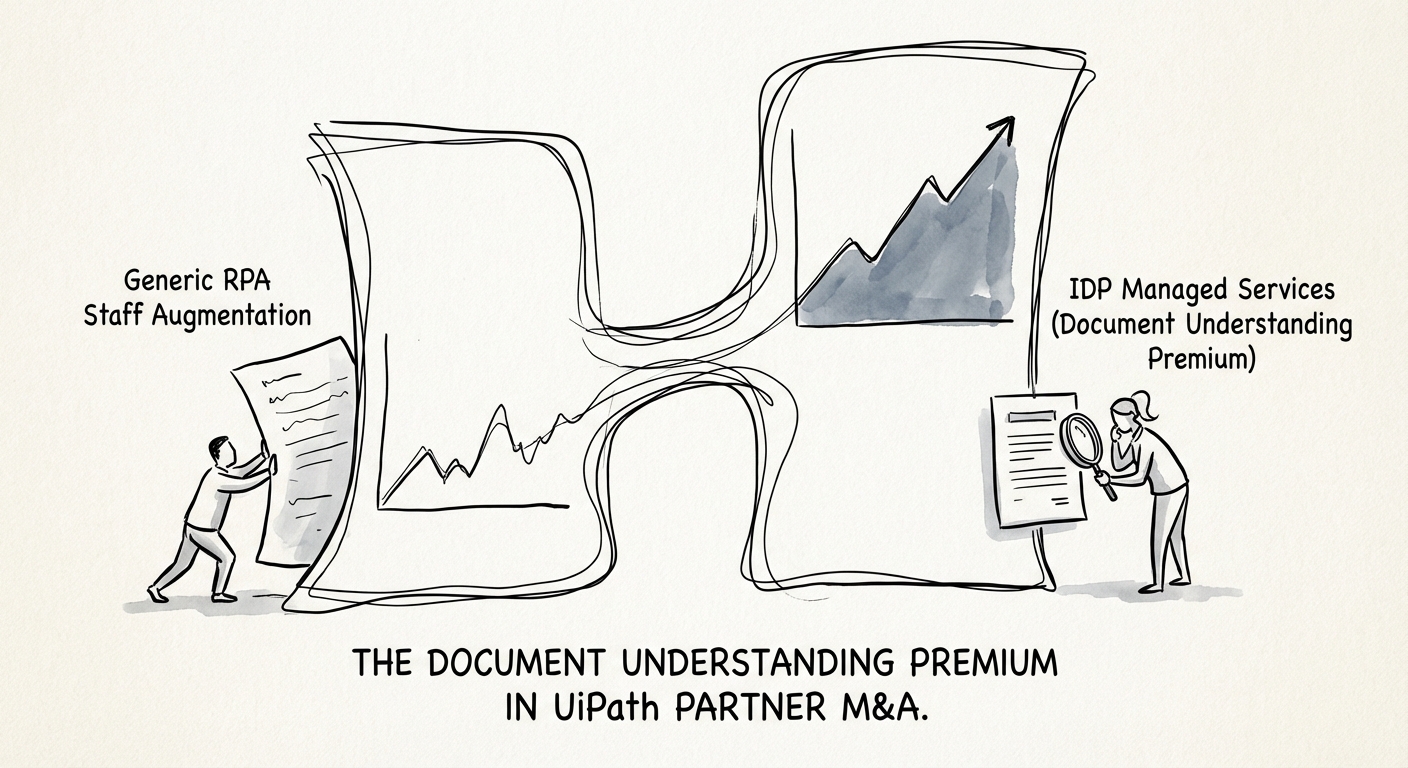

- A 40-person UiPath shop billing T&M trades at 6.5x. The same firm with a custom DU model and 85% STP trades at 13.5x. Here's the diligence that separates them.

- Best fit

- Industry: Intelligent Automation. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 13.5x Average EBITDA multiple for UiPath partners with >40% revenue from IDP/AI projects, versus 6.5x for generic RPA services.

Two firms walk into the data room

Picture two UiPath partners, both around 40 people, both doing roughly $9M in services revenue. On paper, you would swear they were the same company. One walks out of diligence with a term sheet at 6.5x EBITDA. The other clears 13.5x. The gap isn't sales motion, geography, or a charismatic founder. It's what happens after a document hits the queue.

The first firm builds bots. Developers at $150/hour script "move this field from the invoice PDF into SAP, then click submit." It works, it bills, and it is also exactly the capability Microsoft now ships inside Power Automate and Salesforce bundles into Flow — plus whatever a client's own analyst can now assemble with a Copilot prompt. When the thing you sell becomes a checkbox in software the buyer already licenses, you don't have a moat. You have a notice period.

The second firm sells something a platform can't commoditize on its own: the ability to read the documents nobody else can. UiPath's own positioning leans on this — that the bulk of enterprise data lives in unstructured formats that traditional automation simply can't touch (see UiPath's FY2025 financial results, where the AI and document-led products carry the growth narrative). When I run technical diligence on a partner, the first question I'm really answering is which of these two firms I'm looking at. The frontmatter on the deal — "UiPath Gold Partner, RPA expertise" — tells me nothing. The Validation Station tells me everything.

When I open a UiPath partner's books, I don't read the revenue line first. I read the Validation Station logs. They tell me whether you sold a model or rented out a keyboard — and the multiple follows the answer.

Why a "per document" line item is worth more than a "per hour" one

The premium isn't sentiment about AI. It shows up in the financials in three concrete places, and a buyer's analyst will find every one of them.

First, the pricing model flips the margin structure. Generic RPA is a Time & Materials business — you sell hours, the hours have a ceiling, and a client who learns the tool stops buying them. Intelligent Document Processing lets you price per document processed, which means once a model is trained and running, your marginal cost collapses while the invoice keeps going out. That's the difference between the ~38% gross margins typical of T&M delivery and the 55-65% an asset-based managed service throws off. The Everest Group IDP State of the Market work tracks this shift toward outcome and consumption pricing across the category — and in the data room, the margin line is the first thing that makes a partner look like software instead of staffing.

Second, the revenue gets stickier in a way that compounds. When you've trained the model that reads a client's claims or contracts, you're not a vendor they renew — you're plumbing they'd have to rip out. We consistently see IDP-led managed contracts carry meaningfully higher net revenue retention than project-based RPA, because churning means re-solving the unstructured-data problem from scratch. That's the revenue-quality story buyers pay up for: not just how much, but how hard it is to take away.

Third, IDP unlocks a different budget line. Nobody can point a language model at supply-chain or claims data while it's trapped in a scanned PDF, so the partner who owns the extraction layer becomes the prerequisite for everything downstream. That reframes the firm from "automation vendor" competing for shrinking IT-ops dollars to data-infrastructure partner pulling from the AI budget — the one part of the enterprise spend that's actually expanding. Same engineers, same office; entirely different P&L the buyer underwrites.

The three things I check before I believe the premium

Every partner now "does IDP." The word is on the website, it's in the deck, it's in the founder's opening five minutes. So I throw the claim out and audit three artifacts that can't be faked in a pitch.

One: do they train models, or just call them? There's a canyon between a firm that runs the out-of-the-box "Invoices" or "Receipts" extractor and one with the data-science bench to train a custom model for, say, complex commercial insurance claims or multi-jurisdiction loan files. The first is consuming a UiPath feature anyone can license. The second has built IP — a proprietary, hard-to-replicate asset that survives the acquisition. I ask to see the training data pipeline and the model versioning. If the answer is "we use the standard models," the 13.5x conversation is over.

Two: what's the Straight-Through Processing rate on the hard documents? This is the metric that separates an engineering shop from a BPO with a tech veneer. STP is the share of documents that clear without a human touching the Validation Station. A partner running 85% STP on genuinely messy inputs has optimized the model, the confidence thresholds, and the exception logic — that's leverage. A partner at 40% is paying people to clean up after the machine, which means their "automation" margin is a labor cost in disguise. The Gartner RPA category work (Magic Quadrant for Robotic Process Automation) frames the platform; STP tells you who actually operationalized it. I pull the logs across the client base, not the one flagship account they want me to see.

Three: do they own a vertical, or do they "process anything"? The richest multiples go to partners who fused Document Understanding with one domain — healthcare claims adjudication, bills of lading in logistics, KYC packets in banking, mortgage origination. "We automate any document" reads as no document in particular, and it discounts. A firm that can say "we are the partner for mortgage origination intake" has pricing power and a referenceable wedge — the same vertical-specialization premium showing up across the data ecosystem. If you're a founder eyeing an exit in the next 18 months, this is the most actionable of the three: you can't manufacture a custom-model portfolio by Q3, but you can stop chasing every RFP and concentrate your next four wins in one vertical. That's the move that re-rates the firm.