The practical answer

- Short answer

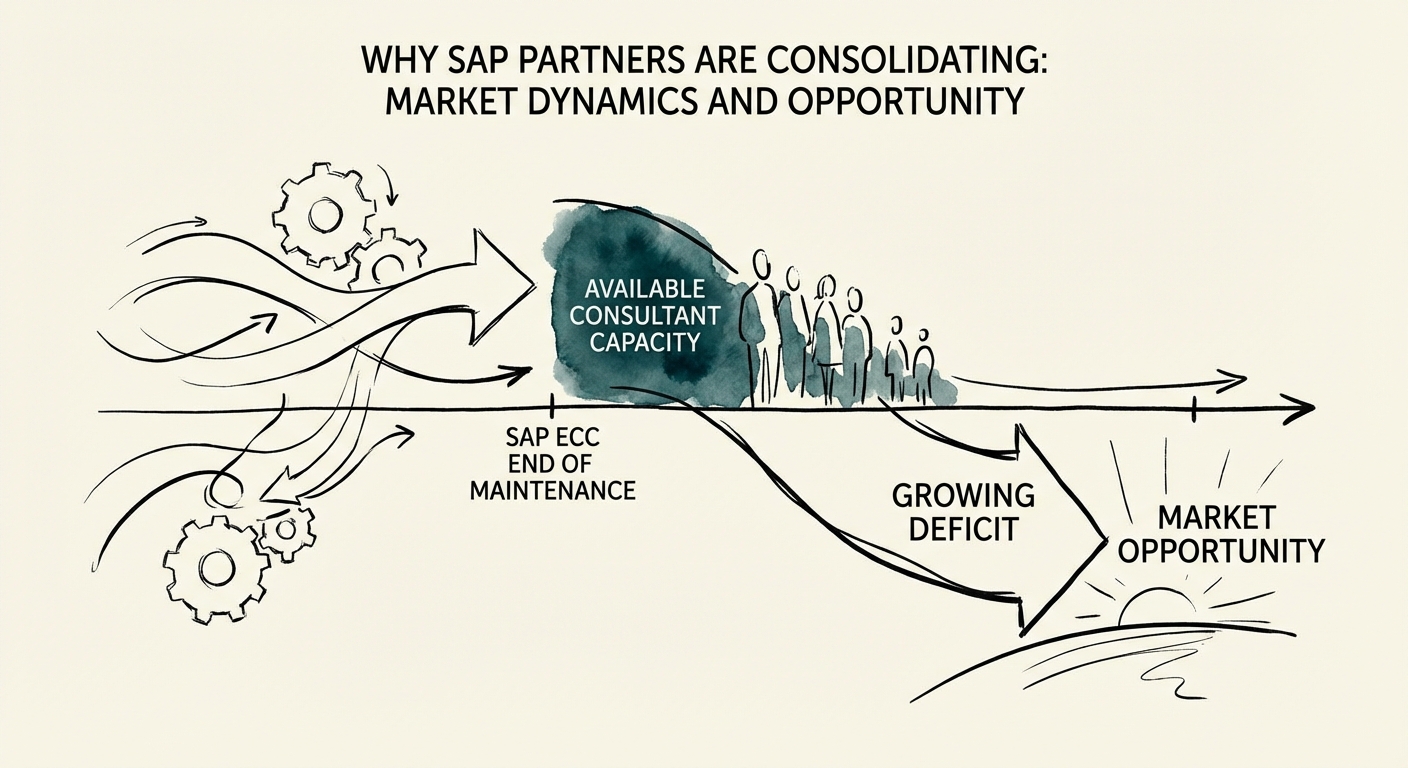

- The 2027 S/4HANA deadline is driving a massive wave of SAP partner consolidation. Here's the Private Equity playbook for capitalizing on the 40,000-person talent deficit.

- Best fit

- Industry: Private Equity / IT Services. Function: M&A / Corporate Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 60% of SAP customers have yet to migrate to S/4HANA, creating a $100B+ service TAM through 2030.

The 2027 Forcing Function: A Perfect Storm for Consolidation

The deadline is no longer theoretical. With SAP discontinuing mainstream maintenance for ECC (Enterprise Core Component) in 2027, the market is facing a supply-demand imbalance of historic proportions. Approximately 60% of SAP’s 35,000+ ERP customers have not yet migrated to S/4HANA. This isn't just a software upgrade; it is a fundamental re-architecture of the enterprise core, requiring specialized skills that the current market cannot supply.

For the sub-$20M revenue SAP partner, this deadline is an existential threat. These boutique firms cannot afford to maintain the bench of S/4HANA architects, Business Technology Platform (BTP) developers, and functional consultants required to deliver complex, multi-year transformations. The cost of a Senior S/4HANA Architect has risen by 35% in the last 18 months, crushing margins for firms that rely on a "just-in-time" staffing model.

This is where Private Equity sees the arbitrage. By rolling up regional boutiques into a "Super-Boutique" or Platform Company, sponsors can create the scale necessary to hold a specialized bench, amortize the cost of recruiting, and compete for mid-market migrations that are too small for the Big 4 but too complex for a generic MSP. The math is simple: a $15M SAP consultancy trades at 6x-8x EBITDA. A $100M integrated platform with deep S/4HANA expertise trades at 12x-15x. The delta is pure multiple expansion, fueled by the Platform Company Playbook.

You can't bill 40% margins on a 'bench' that exists only on LinkedIn. In the SAP ecosystem, the asset isn't the laptop—it's the architect who knows how to map legacy ECC data to S/4HANA without breaking the General Ledger.

The Valuation Hierarchy: From Generalist to "Industry Cloud"

Not all SAP revenue is created equal. In 2026, we are seeing a distinct bifurcation in valuation multiples based on where in the stack a partner plays. The days of high multiples for general staff augmentation are over. The premium accrues to partners who own "Industry Cloud" IP or specialized micro-vertical expertise.

The Multiple Ladder

- Commodity Staffing (6x-8x): Providing generic ABAP developers or functional analysts. Zero IP, low retention, 100% project-based revenue.

- Migration Factory (8x-10x): Proven methodology for "Brownfield" or "Bluefield" migrations. Standardized tooling, predictable delivery, but still heavily services-dependent.

- Managed Services / AMS (10x-12x): Long-term Application Management Services contracts. High recurring revenue, sticky customer relationships, but often plagued by "race to the bottom" pricing.

- Industry Cloud / BTP Innovation (12x-15x+): Partners building proprietary extensions on the SAP Business Technology Platform (BTP) for specific verticals (e.g., Life Sciences, Aerospace, Retail). This is the "Holy Grail" for PE buyers—service margins with SaaS-like stickiness.

For Operating Partners, the due diligence focus must shift from pure EBITDA to "Revenue Quality." A partner with 40% of revenue derived from BTP extensions and high-margin advisory is worth significantly more than a firm with higher EBITDA margins but 90% revenue from low-end staffing. This is where IT Services M&A Valuation trends are punishing those who haven't evolved.

The Integration Trap: Why Rollups Fail

The financial logic of an SAP rollup is impeccable, but the operational reality is often a disaster. The primary failure mode is the "Culture Clash" between lifestyle founders and institutional scale. Many boutique SAP partners are run by former practitioners who prioritize technical excellence over margin discipline. They run their businesses on spreadsheets, handshake deals, and tribal knowledge.

When you acquire three of these firms and attempt to integrate them, you often find:

- The "Cobbler’s Children" Problem: The SAP partner’s own internal systems are archaic. They sell digital transformation but run on QuickBooks and Excel. Integrating their financials takes 12 months, not the projected 90 days.

- Delivery Methodology Conflicts: Firm A uses SAP Activate; Firm B uses a custom Agile hybrid; Firm C "just gets it done." Merging these into a single, scalable delivery model triggers a revolt among senior architects, leading to the "Talent Drain"—the one thing you cannot afford in a talent-short market.

- Phantom Backlog: The "signed" pipeline in the CIM (Confidential Information Memorandum) often evaporates upon closer inspection. Revenue Quality Audits frequently reveal that "committed" projects are actually soft verbal agreements dependent on the founder's personal relationship.

To succeed, PE sponsors must deploy a "First 100 Days" plan that focuses on retention of key technical talent above all else. In this market, losing your S/4HANA Practice Lead is more expensive than missing your EBITDA target by 10%.