The practical answer

- Short answer

- A diagnostic framework for Private Equity firms evaluating SAP implementation partners. How to spot 'body shops,' value IP, and avoid the S/4HANA valuation trap.

- Best fit

- Industry: Private Equity / IT Services. Function: M&A Due Diligence

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 12.8x Median EV/EBITDA multiple for PE-led tech services deals in 2025, signaling a premium for high-quality assets.

The S/4HANA "Supercycle" Is a Double-Edged Sword

The narrative in every CIM you read this year is identical: "The 2027 SAP S/4HANA migration deadline is a guaranteed revenue annuity for the next decade." Investment bankers are pitching this as the ultimate tailwind, citing the 40,000+ legacy ECC customers who must migrate or face maintenance premiums and security risks.

They aren't wrong about the demand. They are wrong about the profitability of that demand.

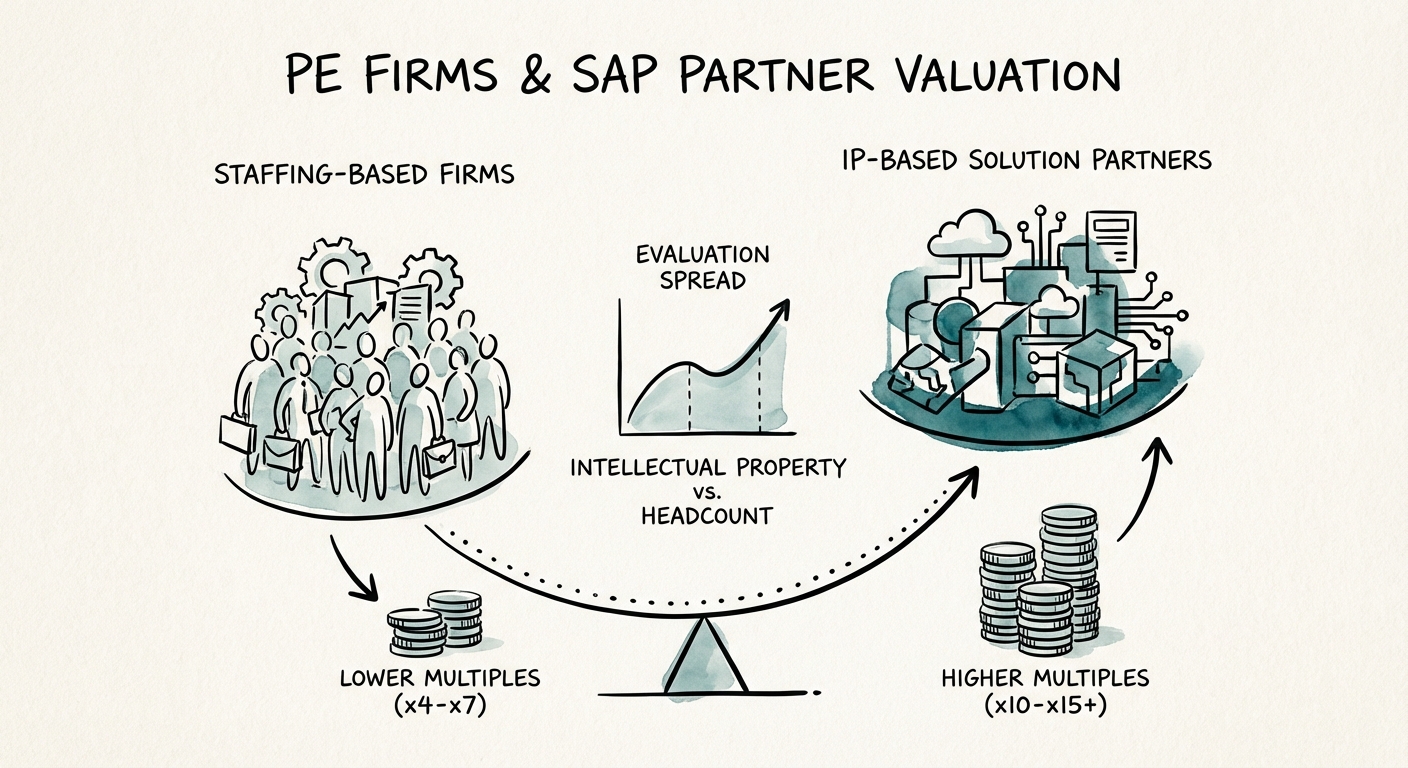

We are seeing a bifurcation in the market that is punishing "body shop" consultancies while rewarding IP-led firms with multiples that rival SaaS companies. In 2025, Private Equity sponsors paid a median EV/EBITDA multiple of 12.8x for premium tech services assets, while generic staff augmentation firms struggled to break 6x. The difference wasn't revenue growth—it was revenue quality.

For a PE Operating Partner, the risk isn't that the market disappears. The risk is acquiring a firm that looks like a consultancy but operates like a low-margin staffing agency, unable to scale without linearly adding headcount in a talent-constrained market. You cannot arbitrate labor costs when senior SAP architects are commanding $250/hour.

We are seeing a bifurcation in the market that is punishing 'body shop' consultancies while rewarding IP-led firms with multiples that rival SaaS companies.

The 4-Point "Operator's Audit" for SAP Targets

When we conduct Operational Due Diligence (ODD) on SAP partners, we ignore the revenue CAGR slide and go straight to the delivery model. Here is the diagnostic framework to determine if you are buying a platform or just a payroll liability.

1. The "Paper Tiger" Certification Audit

Do not trust the "Gold Partner" slide. We frequently find firms boasting "500+ Certified Consultants" where 80% of those certifications are held by juniors with zero full-lifecycle implementation experience. This is a latent risk for project failure.

- The Metric: Calculate the ratio of Lead Architects (10+ years exp) to Juniors. If it's worse than 1:8, the firm is billing for training, not delivery.

- The Risk: Red flags in delivery quality usually surface in month 6 of an engagement, leading to clawbacks and reputation damage.

2. Revenue Quality: Project vs. Managed Services

The "Migration Bubble" is finite. What happens in 2028? The highest-value targets use the migration project as a loss leader (or low margin entry) to secure multi-year Application Management Services (AMS) contracts.

- The Benchmark: Best-in-class SAP partners have 40%+ of revenue attached to recurring AMS or IP subscriptions. If the target is 90% "eat what you kill" project revenue, discount the multiple by 3 turns.

3. IP & Accelerators: The Margin Expander

Does the firm start every project with a blank sheet of paper? Or do they have proprietary industry templates, code libraries, and data migration tools? This is the difference between 25% and 45% gross margins.

- The Check: Ask for the "IP Attribution" analysis. How many billable hours were saved by internal tools in the last 10 projects? If the answer is "we don't track that," they don't have IP. They have PowerPoint decks.

4. Concentration Risk: The "Whale" Trap

SAP projects are massive. It is common to see a $20M revenue firm with one client generating $12M. This isn't a business; it's a project team for hire.

- The Rule: If the top client is >20% of revenue, you are buying a customer concentration risk that requires a structured earnout, not cash at close.

The Valuation Adjustment Matrix

You cannot pay 12x for 6x operations. Use this matrix to adjust your LOI based on operational reality.

The "Body Shop" Discount (Target Multiple: 4x-6x)

These firms trade on labor arbitrage. They have high attrition (25%+), low utilization (or artificially high utilization burning out staff), and no proprietary assets. Their revenue growth is capped by their recruiting speed. In the 2026 talent market, this is a losing bet.

The "IP-Led" Premium (Target Multiple: 10x-14x)

These firms have "productized" their service delivery. They sell outcomes, not hours. They have:

- Proprietary IP: Pre-built SAP BTP (Business Technology Platform) extensions that they license to clients.

- Vertical Focus: They don't do "SAP for everyone." They do "SAP S/4HANA for Mid-Market Manufacturing in the Midwest."

- High Retention: Utilization rates are optimized at 75-80% without burnout because tools do the heavy lifting.

The Verdict: The S/4HANA deadline creates urgency, but it also creates noise. The winners in this vintage will not be the firms with the most consultants, but the firms with the most leverage. Buy the code, not the headcount.