The practical answer

- Short answer

- A roll-up bidding against its own three brands in the same RFP is burning EBITDA. Here is the 180-day decision window and the 90-day sunset that keeps the revenue.

- Best fit

- Industry: B2B Technology & Services. Function: Go-To-Market Operations

- Operating path

- Migration & Integration → Turnaround & Restructuring → Transaction Advisory Services

- Key metric

- 30% Customer-profile overlap threshold that mandates immediate brand retirement.

Two of your own logos showed up on the same RFP shortlist

The fastest way to see the cost of a dual-brand portfolio is to watch a procurement team build a vendor shortlist. On a recent $50M technology roll-up I worked through, the sponsor insisted on keeping three regional brands alive to "preserve local equity." Eight months later, an enterprise buyer's shortlist for a single contract listed two of our own brands as competing vendors. We had a sales rep discounting against another sales rep on the same payroll. We won the deal and lost the margin, because the only way to break the tie was price.

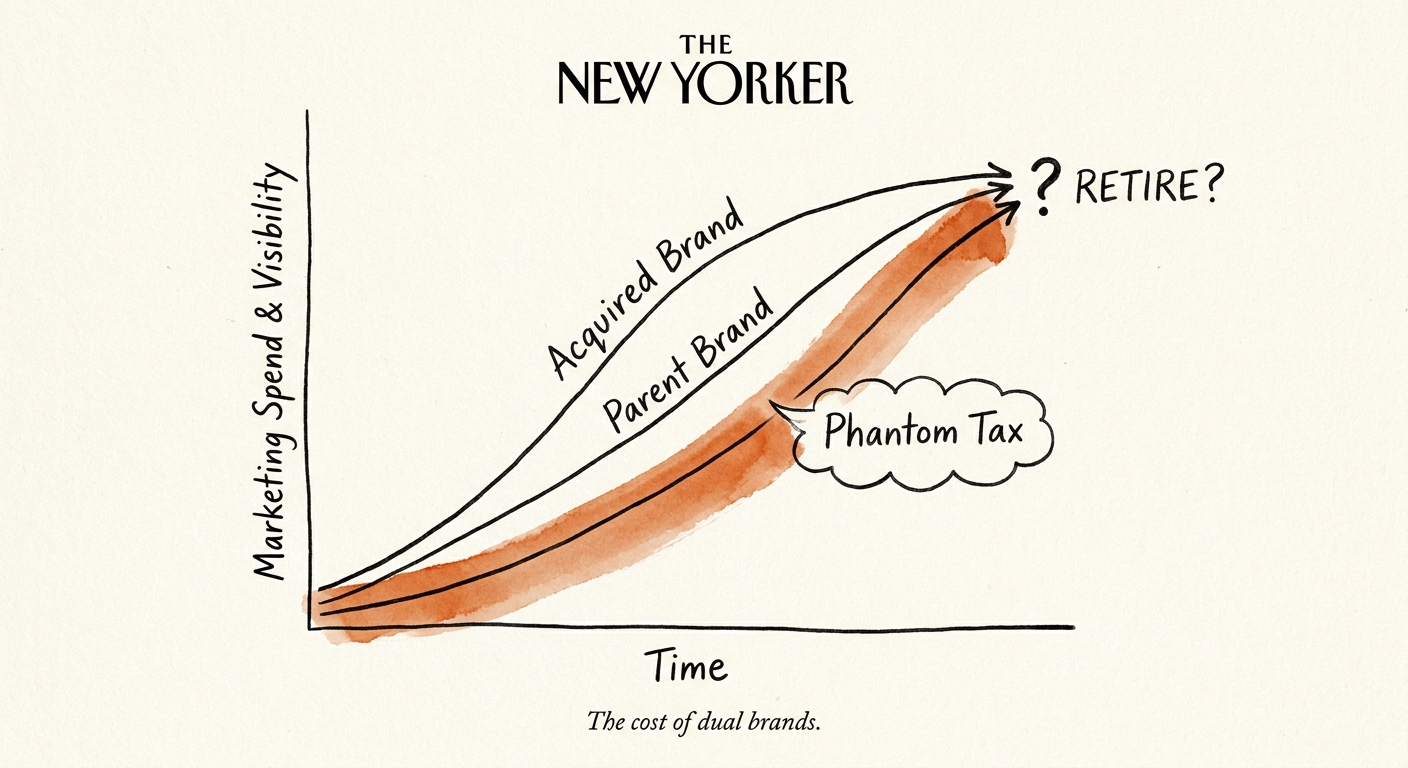

That is what dual-brand architecture actually buys you after month six: not loyalty, but a tax. You pay it in duplicated paid-search bids on identical keywords, in two marketing teams producing two versions of the same case study, in analysts who cannot decide whether you are one platform or three boutiques. Acquirers treat the legacy name like a sacred artifact and call leaving it alone "do no harm." The harm is just invisible on the P&L until you go looking for it in the SG&A line.

And the customer you think you are protecting is the one you are confusing. Harvard Business Review's work on the integration playbook notes that satisfaction tends to dip in the years after an acquisition, often because the service experience fragments across the seams of the combined company. If your investment thesis promises a 25% cross-sell synergy in year one, ask yourself the literal question the buyer asks: which of these three brands do I sign the master agreement with? When the answer is unclear, the cross-sell does not happen. The brand you kept to protect revenue is the thing preventing the revenue you underwrote.

A brand you keep "just to be safe" is a salesperson on payroll whose only job is to lose to your other salesperson. You are funding both sides of the deal.

The retirement decision is arithmetic, not sentiment

The executive team will want to debate this brand by brand, founder by founder, with a lot of feeling about "what the name means in that market." Take the emotion out and replace it with three readings off the integration model. The reason to move fast is that delay compounds: EY-Parthenon puts median integration cost in the tech, media, and telecom sector at roughly 5.6% of target revenue, and a brand left on life support converts that one-time transition spend into permanent overhead that never ends. Every month the legacy logo survives, that 5.6% keeps ticking.

Trigger one is pipeline overlap. Pull both brands' active pipelines and tag by buyer persona. If more than 30% of the acquired brand's open opportunities chase the exact same persona your platform already sells to, the brand is not serving a distinct market — it is splitting your demand-gen budget and bidding against your own domain. That brand retires. There is no version of "preserving optionality" that justifies paying twice to compete with yourself for one buyer.

Trigger two is the system seam. You cannot run unified pipeline reporting while reps are still emailing from two domains and pitching from two decks — the operational fiction breaks the moment a deal touches both teams. As we covered in consolidating CRM data across acquired sales teams, attempting to merge pipeline data on top of two live brand identities is how CRM consolidations fail at high rates. The brand and the system have to retire together; sequence them apart and you get neither.

Trigger three is the clock, and it is the one operators underestimate. You have roughly 180 days post-close before "temporary" becomes "the way things are." Past that window, employees and customers have rebuilt their mental model around the dual-brand state, and changing it now reads as erasure rather than integration. That is when you trigger the kind of resistance documented in the post-merger culture clash — legacy staff defending an identity they have re-anchored to, with a 15% to 20% attrition spike among exactly the people who hold the customer relationships you bought.

A 90-day sunset that moves equity instead of burning it

Once the decision is made, the execution risk inverts. The mistake now is not waiting too long — it is going too fast. Flip the legacy domain dark over a weekend and redirect everything to the parent, and you will watch the acquired customer base churn out of pure reflex. The goal of the next 90 days is to move brand equity across the bridge before you burn the bridge, in three deliberate moves.

Days 1 to 30, the endorsement phase: the acquired brand stays primary but every surface gains "A [Platform] Company" — site header, email signatures, deck footers, sales collateral. You are not changing the relationship yet, you are announcing it. Route inbound traffic through dual-branded landing pages so the market starts associating the two names while the familiar one still leads. Nobody should feel anything change except a new line of small type.

Days 31 to 60, the migration phase, is where revenue actually leaks. The platform brand takes the visual lead and the legacy name steps down to a product or service-tier label. This is the moment a careless email costs you accounts — as we found in sunsetting acquired products, botched communication in this specific window can vaporize a large share of acquired revenue. Hand your customer success and account managers a tight, pre-written script that frames the change as a capability upgrade the client is gaining, not a cost cut the sponsor is running. The frame is the whole job here; left to improvise, half your reps will apologize for the change and confirm the customer's worst read of it.

By Day 90 the legacy brand is gone from every external surface: domains permanently redirect, LinkedIn pages merge, decks are unified, and the field stops carrying two identities into the same room. The payoff is the inverse of the problem you started with — one logo on the RFP shortlist, one bid, full margin, and the cross-sell synergy you promised the investment committee finally able to land because the buyer knows who they are signing with. A retired brand is not a loss on the integration ledger. It is the line item where the multiple you underwrote stops leaking.