The practical answer

- Short answer

- A 12-month TSA meets a 14.2-month migration, and the gap costs 3-5% of deal value. The pricing clauses, exit ramps, and extension math PE buyers miss.

- Best fit

- Industry: Private Equity & Technology M&A. Function: M&A Integration

- Operating path

- Migration & Integration → Turnaround & Restructuring → Transaction Advisory Services

- Key metric

- 68% of IT-related TSAs require extensions beyond their initial term due to unexpected data entanglement.

The number you should fear is 2.2, not 12

Here is the trap in one line of arithmetic. The seller hands you a 12-month IT Transition Services Agreement and calls it generous runway. Your standalone ERP cutover will actually take 14.2 months. That 2.2-month gap is not a scheduling footnote — it is the exact window where the meter switches from "base rate" to whatever the extension schedule allows, and the extension schedule is where the whole deal economics quietly get rewritten in the seller's favor.

I watched this play out on a roughly $400M industrial-technology spin-off. The seller proposed a clean-looking 12-month IT support TSA, fully bundled, single monthly fee. Most operating partners would have flagged it as a diligence checkbox and moved on. When we pulled the underlying service schedules apart, line by line, the base fee was reasonable and the month-seven tier carried a step increase north of 200%. The agreement was not priced to support the carve-out. It was priced to make staying expensive the moment we were most likely to still be there. That is the design, not the exception. According to PwC's 2025 Carve-Out Benchmarking Report, 68% of IT-related TSAs require extensions beyond their initial term because of data entanglement nobody scoped during diligence — meaning two out of three buyers walk straight into the penalty tier they never modeled.

The financial bleed is not theoretical. McKinsey's Global M&A Carve-Out Analysis puts base-period TSA cost at 1.5% to 3% of the target's annual revenue, rising toward 5% once you are negotiating extensions from a position of no leverage. On a $400M deal, the difference between a disciplined exit and a default one is millions of dollars of first-year EBITDA — the same EBITDA your investment thesis was underwritten against. The fix starts before signing: model the TSA as a direct reduction to enterprise value in the LOI, the way you'd treat assumed debt, not as an operating line you'll sort out after close. If you want the broader picture of where carve-outs run hotter than standard deals, the carve-out integration complexity benchmarks are the baseline read.

A TSA isn't a bridge you cross together. It's a vendor contract with a counterparty who profits from your delay — price it that way at the LOI, not at month seven.

The Six-Month Wall: two ways to lose, one narrow path through

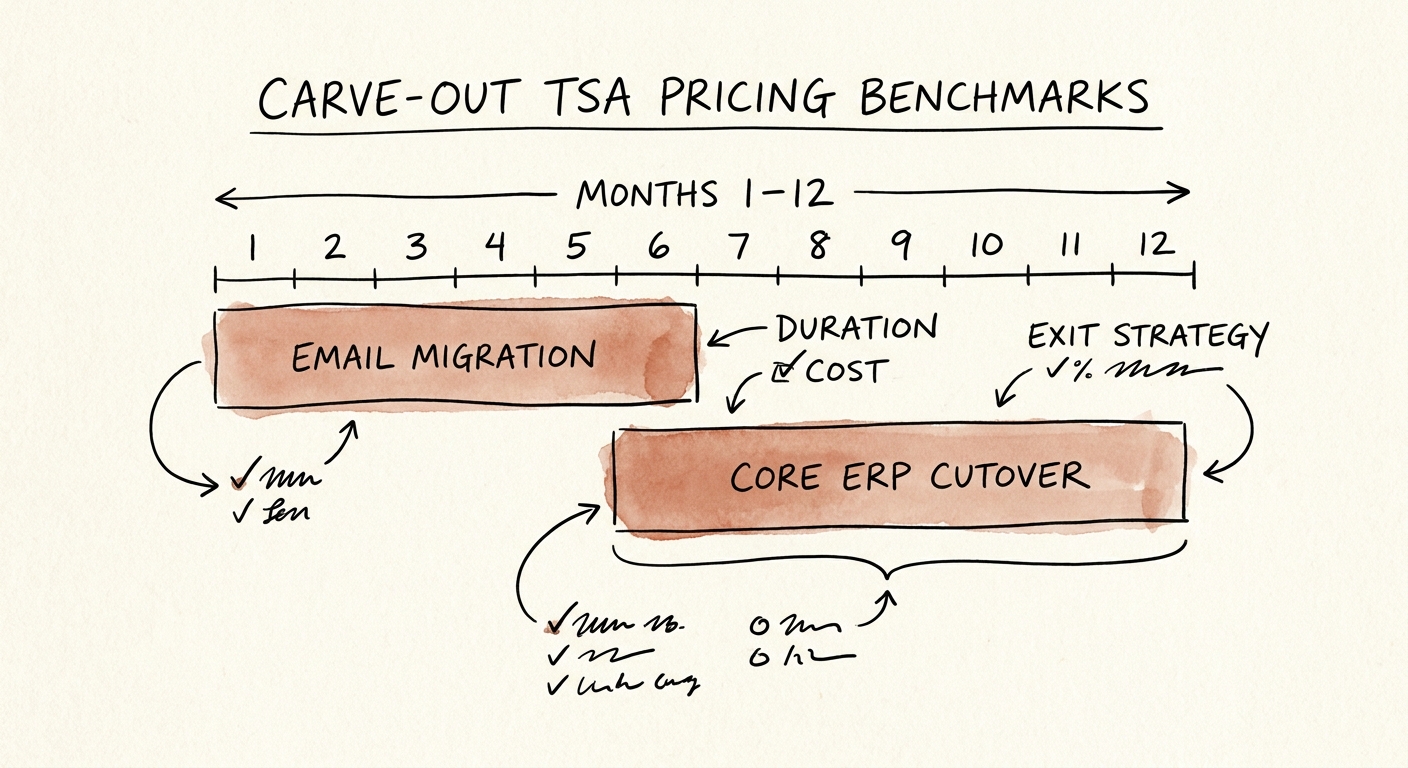

There are two failure modes in a TSA, and they pull in opposite directions, which is why most teams hit one while dodging the other. Stay too long and the extension pricing eats your margin. Sprint out too early and you break production. The honest planning challenge is that you cannot solve both with a single exit date — you have to stagger the exits by system, and the timeline that drives everything is the ERP.

Standalone ERP migrations are the long pole, and they are longer than the legal agreement assumes. Bain & Company's 2026 Technology Integration Study pegs standalone ERP and core-infrastructure migration at an average of 14.2 months — driven by the custom middleware, legacy on-prem dependencies, and tangled master data that never show up in a data room. That is the source of the 2.2-month gap, and it is why "12 months is plenty" is the most expensive assumption in the carve-out playbook. But the inverse is just as punishing: Deloitte's Divestiture Survey found buyers who force their way off the TSA before month nine suffer a 22% higher rate of critical system failure post-cutover — corrupted financial history, dropped billings, customers who churn the first time an invoice goes wrong.

So the path through is not a single cutover date; it is a triage schedule that isolates the seller's leverage to as few systems as possible. We run it in three bands. Email, Active Directory, and endpoint security exit inside 90 days — they're low-risk and they're where seller goodwill is cheapest. Sales operations and CRM exit by month six, before the extension cliffs bite. Payroll, supply chain, and the financial ERP modules ride the full twelve, because those are the systems where a Deloitte-style failure actually destroys value. By month six — the wall — every system that can be off the TSA should be off it, so the only thing exposed to a month-seven price hike is the handful of modules that genuinely needed the runway. That band-by-band sequencing is the spine of any credible M&A integration timeline; the carve-out version just enforces it harder because the counterparty is billing you for every week of indecision.

Three clauses that decide whether you win the TSA

Pricing is where sellers recover what they couldn't get in the headline number, and the mechanism is the "cost-plus" model. A parent company about to divest is sitting on stranded overhead — people and licenses it can't shed on Day 1 — and the TSA is a convenient place to park it. KPMG's 2026 Carve-Out Financial Playbook found 74% of corporate sellers embed a 10% to 15% markup into IT and HR TSA fees on top of allocated overhead. Read that plainly: you are funding the seller's restructuring while they bill you a margin for the privilege. Three contract terms reverse it.

First, kill cost-plus and price on consumption. Refuse allocated-overhead math. Demand a flat, linear fee tied to actual usage — ticket volume, instance count, seats — so you stop subsidizing the parent's stranded org chart. If they won't drop cost-plus entirely, that's your opening for the next clause. Second, attach SLA penalties with teeth. Without them, your carve-out becomes the lowest-priority queue in an IT team that's actively being wound down — and you'll feel it in uptime and ticket resolution exactly when you're mid-migration. Write in an automatic fee reduction (we use 15% the following month) every time uptime or helpdesk resolution misses the defined threshold. Make poor service cost the seller money, not you. Third, buy granular early-termination rights, not a monolith. If your team executes a tight 120-day technology integration roadmap and lands the CRM in four months, you should stop paying CRM fees in month five — not carry them through a bundled, all-or-nothing term. Per-service termination turns every early migration into immediate savings instead of trapped spend.

The mindset shift behind all three: a TSA is not a cooperative bridge you and the seller cross together. It is a vendor contract with a counterparty whose incentives run opposite to yours — they profit from your delay, your dependency, and your hesitation. Price it that way at the LOI, sequence the exits to collapse their leverage by month six, and penalize failure in writing. Do that, and the 2.2-month gap stays a footnote instead of becoming the line item that breaks your first-year thesis.