The practical answer

- Short answer

- The bespoke playbook that worked on your platform deal silently destroys margin on bolt-ons 2-10. Here's the 30-day ingestion model that protects the thesis.

- Best fit

- Industry: Private Equity / IT Services. Function: M&A Integration

- Operating path

- Migration & Integration → Turnaround & Restructuring → Transaction Advisory Services

- Key metric

- 20% Decrease in integration costs for programmatic acquirers who use a standardized ingestion engine.

The platform deal was the trap, not the template

Picture the month-end close at a roll-up that's done eight deals: a controller exports trial balances from seven different ERPs into one master spreadsheet, hand-keys the mappings, and prays the consolidations tie out before the board call. That spreadsheet is the single source of truth for a company that costs nine figures. Nobody set out to build that. It's what happens when you let your first acquisition write the playbook for every one that follows.

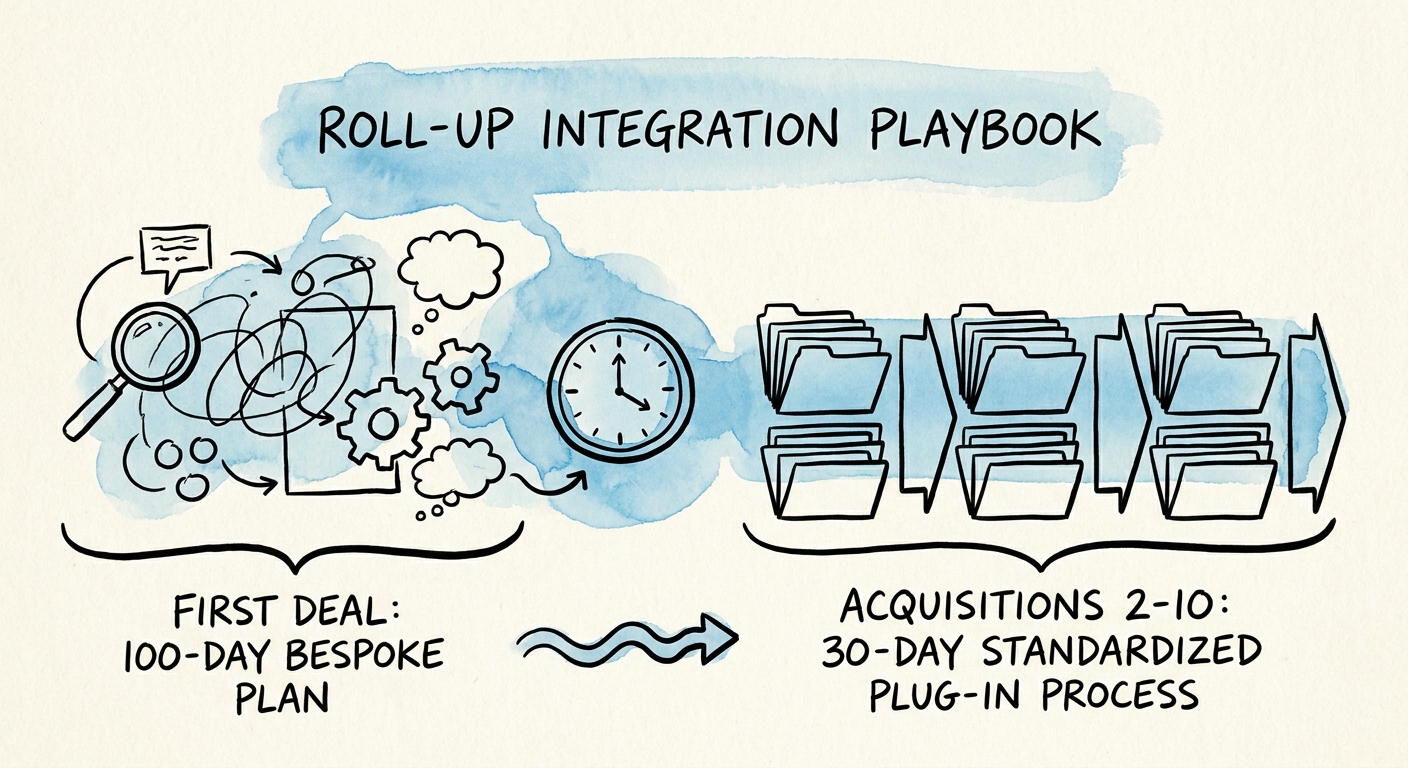

Your platform deal earned a careful, high-touch integration — 100 days of culture-building, strategy alignment, and bespoke architecture. That was correct. The mistake is treating bolt-ons two through ten the same way. A platform deal is a custom home renovation. Add-ons are a factory line. When every founder who pushes back on adopting the parent stack gets a quiet exemption "to preserve morale," you don't end up with a scalable business. You end up with eight operating companies, redundant licensing, fractured procurement, and back-office headcount stacked to babysit systems that should have died at close. On a stalled mid-market services roll-up I've seen, that pattern alone bled roughly 400 basis points of margin — not from any single bad decision, but from a dozen "reasonable" concessions compounding.

This is the well-documented failure mode of the strategy. Harvard Business Review reports that more than two-thirds of roll-ups fail to create value for investors, and integration difficulty is the usual cause. Here's the part operators miss: five small integrations don't equal one large one. They equal five separate data-mapping nightmares, five vendor-contract entanglements, five chart-of-accounts reconciliations — each one compounding on the unfinished work of the last. The fix isn't more diligence on each target. It's deciding that integration is a repeatable capability you own, not a project you reinvent every time the wire clears.

The first deal earns the right to be careful. Deals two through ten earn nothing — they're just inputs to a machine you should have already built.

The 30-day MVI: three systems, no exceptions

For deals two through ten, you don't get 100 days. You get a Minimum Viable Integration, and it has exactly three non-negotiable cutovers inside 30 days: identity and access management, financial reporting, and HR/payroll. That's it. If you can close the books together and put every employee behind a single sign-on domain by day 30, you've stopped the bleeding. Everything else — the niche ops tooling, the regional CRM customizations, the founder's beloved ticketing system — is secondary and can wait.

The hard part is never technical. It's founder attachment. The founder you just acquired sees their homegrown system as the secret sauce that earned the exit, and asking them to migrate to your Dynamics or your NetSuite feels like an insult. Operators read that resistance as a relationship to manage, so they grant autonomy. That's the fatal move — you cannot capture multiple arbitrage if you can't consolidate the data, and you can't consolidate the data if every company keeps its own systems. As Boston Consulting Group has noted on the value of data in private equity, fragmented integration prolongs underperformance, suppresses the bolt-on's own valuation, and drags down the platform that bought it.

So your playbook needs a rigid, pre-published mapping protocol decided before you ever sign an LOI. If the target runs system X, they migrate to your system Y on a fixed date. No pilots, no "let's revisit next quarter," no special cases. This is also how you avoid the slow-bleed inactive license tax, where duplicate SaaS subscriptions quietly drain EBITDA for years after a close nobody finished. And it reframes technical diligence entirely: on a bolt-on, you don't assess whether their code is good. You assess one thing — the cost and timeline to move their data onto your tracks.

Why the 100-day plan guarantees a backlog

Run the math on your own thesis. If the model calls for three or four acquisitions a year and each one takes 100 days to integrate, you have a permanent queue. Deal three closes while the team is still mapping deal two's chart of accounts. The integration function becomes the bottleneck, and the deal team responds in one of two bad ways: they slow acquisition pace and miss the thesis, or they keep buying and stop integrating — which is precisely how a buy-and-build degrades into a holding company of loosely affiliated logos.

The alternative is to move the work earlier. A 30-day plug-in only works if diligence stops being a pure risk-mitigation exercise and starts being build time. By the time the wire hits, the active-directory migration should already be scripted, the CRM data cleansing already mapped, the comms plan already loaded. The roll-ups that ingest a company a quarter without choking aren't faster integrators — they have a standing integration management office that runs the identical 30-day playbook over and over, treating each deal as the next iteration rather than a fresh problem. McKinsey's research on programmatic acquirers ties exactly this kind of repeatable engine to integration costs landing roughly 20% below initial budgets.

None of this is a tooling decision. The multiple arbitrage in your IC memo is an operational promise, not a financial one. A buyer at exit isn't paying a premium for eight mom-and-pop shops sharing a brand and a spreadsheet; they're paying for one cohesive enterprise on one platform. So before you sign the next LOI, do three things: write the system-mapping protocol now and put it in the deal terms, stand up an IMO whose only job is the 30-day plug-in, and refuse the first founder exemption — because the first one you grant is the one every subsequent founder will cite. Anything past 30 days on a basic bolt-on isn't patience. It's value you're actively destroying.