The practical answer

- Short answer

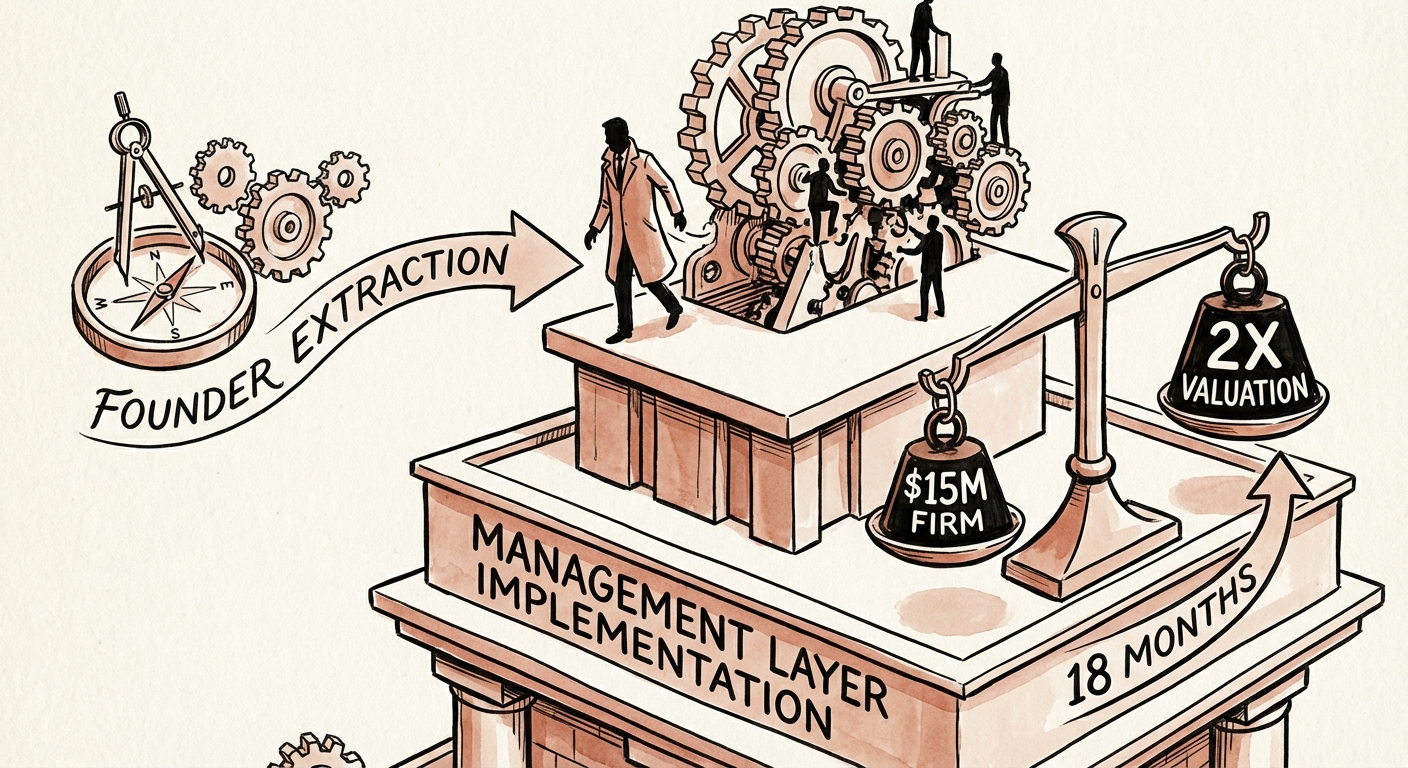

- A diagnostic case study of how a $15M tech services firm moved from a 5x to 10x EBITDA multiple by fixing revenue quality, standardization, and founder dependency.

- Best fit

- Industry: Tech Services. Function: Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 2.2x Multiple arbitrage realized by shifting from 'Project' to 'Managed Services' revenue mix.

The $15M “Unsellable” Plateau

At $15 million in revenue, most tech services firms hit a wall. You are too big to be small, but too small to be a platform. This is the “No Man’s Land” of M&A.

We recently worked with a founder—let’s call her Sarah—who ran a custom software development shop. On paper, the business looked healthy: $15M in top-line revenue, 10% EBITDA margins ($1.5M), and a prestigious client list. But when she took it to market, the feedback was brutal. Private Equity buyers offered 4x-5x EBITDA, valuing the company at roughly $6M-$7.5M. Why? Because it wasn’t a business; it was a high-revenue job for the founder.

The diagnosis revealed three valuation killers common in founder-led services firms:

- Revenue Quality: 80% of revenue was non-recurring project work. Every January 1st, they started at zero.

- Margin Erosion: Delivery was “bespoke” (read: chaotic). Margins were suppressed by constant reinventing of the wheel.

- Key Person Risk: Sarah was the Chief Sales Officer and the Chief Firefighter. If she left, the revenue left.

To exit at a premium, we didn’t need to double revenue. We needed to double the multiple. This is the playbook we used to transform a 5x asset into a 10x asset in 18 months.

You don't get paid for the work you do. You get paid for the system you built that does the work without you.

The Turnaround: Engineering the Multiple

Valuation is a function of two variables: EBITDA × Multiple. Most founders obsess over the first and ignore the second. We attacked both simultaneously.

Phase 1: The Revenue Quality Shift

Buyers pay for predictability. In 2025, pure project-based consultancy multiples are averaging 4.3x to 6.4x EBITDA for sub-$5M EBITDA firms. However, Managed Services Providers (MSPs) with recurring revenue command 8.2x to 10.8x. That is a massive arbitrage opportunity.

We didn’t pivot the entire business. Instead, we repackaged “maintenance” into “Managed DevSecOps.” We moved clients from T&M (Time & Materials) to annual retainers with defined SLAs. Within 12 months, recurring revenue shifted from 20% to 55%. This single move re-categorized the firm in the eyes of buyers, moving them from the “Consulting” bucket to the “MSP” bucket.

Phase 2: The Margin Expansion (Standardization)

You cannot scale art; you can only scale manufacturing. The firm’s delivery was art. Senior engineers were burning out fixing the same issues differently for every client. We implemented a Turnkey Documentation framework to standardize the bottom 80% of tasks.

By documenting SOPs for onboarding, code reviews, and deployment, we shifted delivery load to junior engineers (reducing cost basis) and increased velocity. The result? Gross margins expanded from 38% to 52%. EBITDA margins jumped from 10% to 22% on flat revenue.

Phase 3: Founder Extraction

The final hurdle was Sarah. A buyer will not pay cash at close if they fear the business collapses without you. They will trap you in a 3-year earnout. To maximize cash-at-close, you must fire yourself.

We installed a VP of Sales and a Delivery Head, creating a “management layer” that insulated the business from the founder. We proved it worked by forcing Sarah to take a 3-week vacation during Q4 close. The team hit the number without her. That vacation added millions to her exit value.

The Exit Math: 6x to 12x

After 18 months, the top-line revenue had only grown modestly to $16.5M. But the business underneath was unrecognizable. Here is the math of the transformation:

- EBITDA Growth: Increased from $1.5M (10% margin) to $3.6M (22% margin) via operational efficiency.

- Multiple Expansion: Increased from 5x (Project Shop) to 9x (Tech-Enabled MSP) due to recurring revenue and process maturity.

- Total Valuation: $3.6M EBITDA × 9x Multiple = $32.4M.

The result: A 4.3x increase in enterprise value, driven largely by operational engineering rather than sales growth. In the 2025 market, where the “flight to quality” is real, buyers are paying premiums for clean data, documented processes, and dispensable founders. If you are stuck at the $15M plateau, stop trying to sell more projects. Start building a productized engine.

Actionable Next Steps

- Audit Your Revenue: Calculate what % of your revenue is contractually recurring (not just “repeat”). If it’s under 30%, you have a valuation ceiling.

- Calculate Your “Process Coverage”: What % of your delivery tasks have written SOPs? If it’s under 50%, your margins are leaking.

- The Vacation Test: Can you leave for 3 weeks without checking Slack? If not, you are the constraint.