The practical answer

- Short answer

- Is your Google Cloud practice valued at 1x Revenue or 12x EBITDA? The difference lies in your revenue mix. A diagnostic guide for founders to pivot from resell to high-margin services.

- Best fit

- Industry: Cloud Consulting / MSP. Function: Revenue Operations

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- $7.74 Revenue partners generate per $1 of GCP sold (IDC Forecast)

The Resell Mirage: Empty Calories on Your P&L

If you are a Google Cloud partner doing $20M in top-line revenue, but $12M of that is pass-through resell (billing on behalf of Google), you don't have a $20M company. You have an $8M services firm with a dangerous addiction to low-margin volume.

For years, partners chased "Premier" status by piling up resell bookings. It felt like growth. But in 2025, the economics of simple resale have collapsed. In May 2025, Google Cloud shifted to a variable revenue share model for Marketplace transactions, dropping fees to as low as 1.5% for large deals. This signals a definitive end to the "margin arbitrage" era. Google is effectively telling its ecosystem: Stop moving paper and start moving the needle.

The trap for founders is valuing their company based on that inflated top-line number. Private Equity buyers see resell revenue as "low quality"—it carries high working capital risk (you pay Google before the client pays you) and near-zero defensibility. If your primary value prop is a 3% discount on billing, you are a commodity. In due diligence, we strip that resell revenue out entirely to find your "True EBITDA." Often, what's left isn't enough to justify a Series B valuation, let alone an exit.

Resell revenue is vanity. Service margin is sanity. IP is the exit. If you are transacting $50M of cloud but only billing $5M of services, you are a bank, not a technology company.

The $7.74 Benchmark: Are You a Partner or a Vendor?

The separation between "Elite" partners and "Fulfillment" shops is measured by a single metric: The Service Attach Multiplier. According to IDC forecasts formalized in 2025, top-tier partners generate $7.74 in their own services, software, and IP revenue for every $1 of Google Cloud consumption they influence.

The Hierarchy of GCP Revenue Quality

We classify partner revenue into three tiers of valuation impact:

- Tier 3 (The Anchor): Resell & Fulfillment. (Valuation: 0.5x - 1x Revenue). This is simply transacting the cloud spend. It is necessary for the relationship but high-risk for your margins if it exceeds 30% of your mix.

- Tier 2 (The Labor): Professional Services. (Valuation: 6x - 10x EBITDA). Migrations, implementations, and data engineering. This is healthy, but it scales linearly with headcount.

- Tier 1 (The Multiplier): IP & Managed Services. (Valuation: 12x+ EBITDA). Proprietary solutions sold through the Marketplace that burn down customer commits. This is where the $7.74 figure is reached.

If your ratio is closer to $1:$1 (one dollar of services for every dollar of cloud sold), you are leaving massive value on the table. You are effectively acting as Google's unpaid sales force, bearing the cost of acquisition without capturing the lifetime value of the customer.

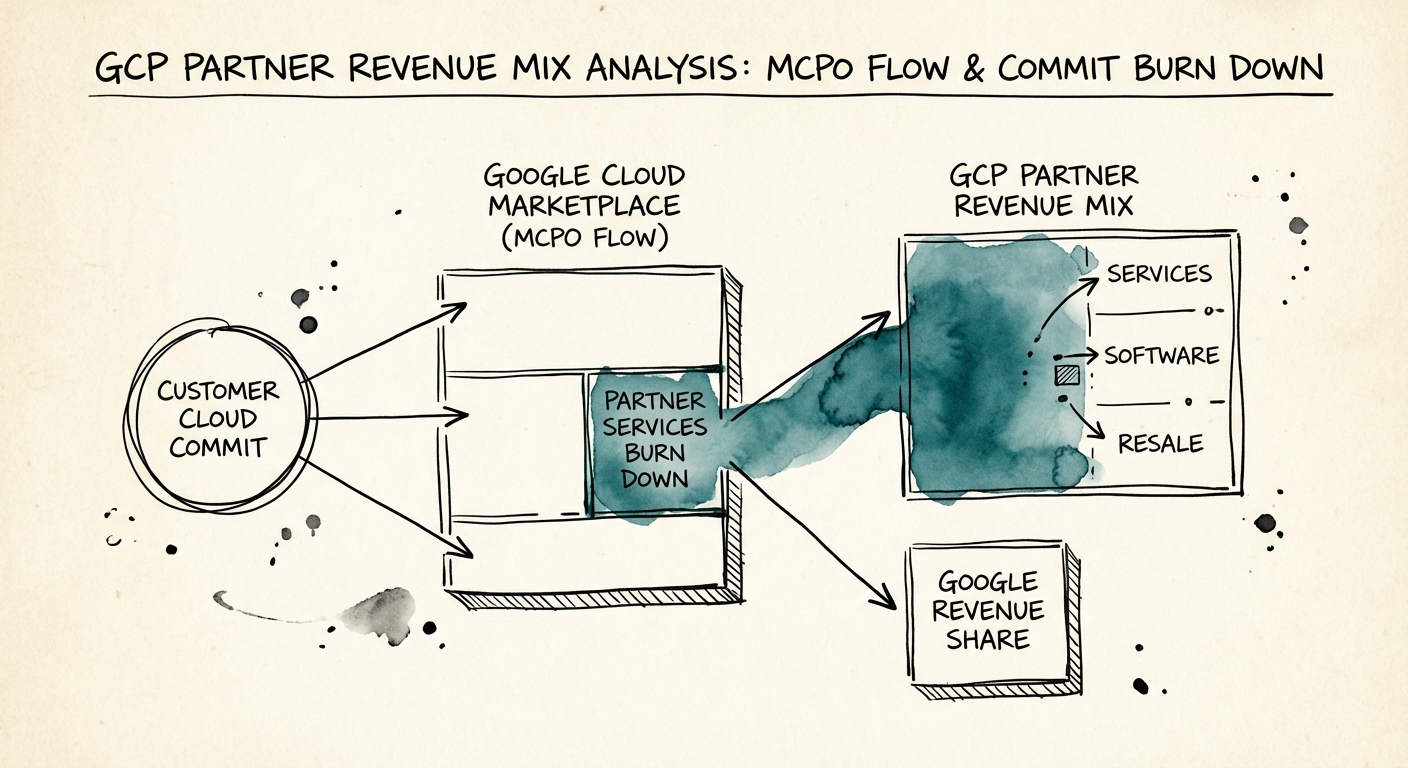

The Marketplace Pivot: From 'Billing' to 'Burning'

The most effective way to fix your revenue mix isn't to stop reselling—it's to change how you resell. The 2025 updates to the Google Cloud Partner Advantage program introduced a game-changing lever: 100% Commit Drawdown for Channel Private Offers (MCPO).

This means your managed services and IP, when sold through the GCP Marketplace, count dollar-for-dollar against your customer's committed cloud spend (up to a cap). This changes the sales conversation from "Please buy my services" to "Let me help you utilize the budget you've already committed to Google."

The Playbook for founders:

- Audit Your Mix: Calculate your Service Attach Multiplier. If it's below $4.00, your sales team is incentivized on the wrong metric (Bookings vs. Gross Margin).

- Productize Your IP: Package your "Tribal Knowledge" into a Marketplace listing. Whether it's a specific "Data Lake in a Box" or a "Security Landing Zone," make it a SKU.

- Shift to MCPO: Stop sending invoices for services. Start transacting your services through the Marketplace. This increases your stickiness (you are now part of their cloud bill) and improves your valuation multiple by reclassifying service revenue as "Cloud Marketplace ARR."