The practical answer

- Short answer

- Is your Palo Alto Networks practice valued as a reseller or a strategic partner? We diagnose the valuation gap between product-heavy and services-led firms.

- Best fit

- Industry: Cybersecurity. Function: Revenue Operations

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 12% Average gross margin for hardware resale, creating a 'valuation drag' on high-revenue partners.

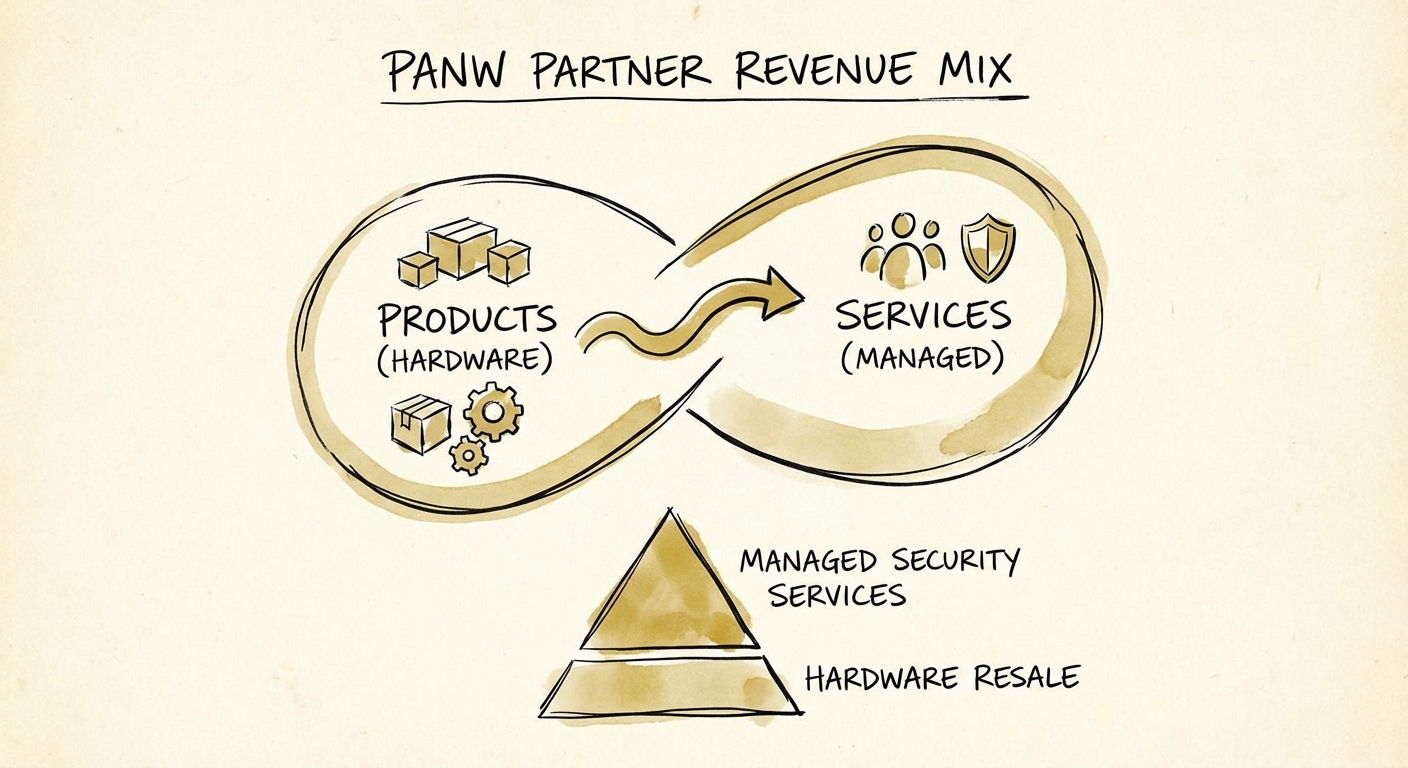

The 'Empty Calorie' Revenue Problem

If you are a Palo Alto Networks partner hitting $50M in annual revenue, you likely feel successful. You have Diamond status, a wall of certifications, and a steady stream of firewall refresh orders. But if 80% of that revenue comes from hardware and software resale, you are walking into a valuation trap.

In the private equity markets of 2026, not all revenue is created equal. We call resale revenue “empty calories.” It fills up the top line, bloats your revenue recognition, and gets you invited to the partner summit, but it provides almost no nutritional value to your EBITDA multiple.

The Tale of Two Partners

Let’s look at two hypothetical PANW partners, both generating $20M in revenue. This diagnostic reveals why one trades at a 12x EBITDA multiple while the other struggles to find a buyer at 5x.

- Partner A (The Box Mover): $16M in resale (80%), $4M in professional services (20%). Their blended gross margin is ~18%. To a buyer, they are a logistics company with a few engineers.

- Partner B (The Platform Player): $8M in resale (40%), $12M in managed services (60%). Their blended gross margin is ~45%. To a buyer, they are a strategic asset with recurring intellectual property.

The market has bifurcated. Traditional Value-Added Resellers (VARs) are trading at distressed multiples because the "margin drag" of resale dilution kills their unit economics. Meanwhile, partners who have pivoted to Next-Gen Security (NGS) services—building managed offerings around Cortex XDR, Prisma SASE, and Unit 42 collaboration—are seeing valuations that rival pure-play SaaS companies.

We see $50M resellers trading at 4x EBITDA because they own the transaction, not the customer. We see $15M managed security partners trading at 12x because they own the outcome.

Benchmarks: The Margin Reality Check

The Palo Alto Networks NextWave program has explicitly pivoted toward "platformization." If your business model is still built on the 2015 era of selling firewalls and one-time implementation fees, you are fighting both the market and your primary vendor.

The Gross Margin Hierarchy

We tracked the unit economics of 45 cybersecurity partners to establish the following margin benchmarks for 2025-2026:

| Revenue Stream | Median Gross Margin | Valuation Impact |

|---|---|---|

| Hardware Resale | 8% - 12% | Neutral / Negative Drag |

| Software/SaaS Resale | 10% - 15% | Neutral |

| Professional Services (Time & Materials) | 35% - 45% | Positive (1x - 1.5x Revenue) |

| Managed Security Services (MSSP) | 50% - 65% | Premium (2.5x - 4x Revenue) |

The data is brutal for generalists. If you are reselling a Strata firewall with a standard discount, you are fighting for scraps. However, if you are wrapping that firewall in a Managed SASE contract or providing 24/7 threat hunting via Cortex XSIAM, your margins leap from 12% to 60%.

The “Stickiness” Factor

Buyers pay for stickiness. Resale revenue resets every year (or every 3 years). Managed services revenue compounds. A partner with $5M in Managed Cortex revenue has a defensible moat; a partner with $20M in resale revenue has a Rolodex that can be poached by a distributor with a lower markup.

As noted in our analysis of MSP valuation factors, the quality of revenue determines the exit multiple. For PANW partners, the "quality" metric is defined by your attach rate of Lifecycle Services vs. simple fulfillment.

The Pivot: From Transaction to Transformation

How do you fix a broken revenue mix? You cannot simply "stop selling hardware"—that volume often anchors your partner tier. Instead, you must change how you sell it.

1. The "Trojan Horse" Strategy

Use resale as the entry point, not the destination. Every hardware refresh conversation must immediately pivot to a Security Posture Assessment. Do not quote a firewall without quoting the “day 2” management of that firewall. If the customer refuses the management, consider if they are a customer worth keeping. High-volume, low-margin customers distract your engineering talent from high-value work.

2. Specialization is the New Scale

Palo Alto Networks’ ecosystem is too vast to be a generalist. The partners commanding 12x multiples are specialists in Cloud Security (Prisma) or Security Operations (Cortex).

- Generalist: "We sell the full PANW catalog." (Result: 10% margin, competing with CDW).

- Specialist: "We are the premier Cortex XDR specialized partner for the healthcare mid-market." (Result: 45% margin, no competition).

3. Productize Your IP

Service revenue shouldn't just be hourly billing. It should be outcome-based. innovative partners are building proprietary “connectors” or “dashboards” on top of PANW APIs. This turns service revenue into something that looks, smells, and is valued like software revenue. Refer to our guide on building IP-based services for a similar playbook.

Diagnostic Checklist

Before you speak to an acquirer, run this simple test:

- Is your Resale/Services mix better than 60/40?

- Is your Managed Services Gross Margin above 50%?

- Do you have at least one NextWave Specialization (e.g., XMDR)?

If you answered "No" to more than one of these, your focus for the next 18 months is clear: Fix your mix before you fix your pitch deck.